Your Claims Operation Has a $308 Billion Blind Spot

I want to start with something that does not make it into board presentations.

Every year, I talk to operations leaders at U.S. insurance carriers. People who are sharp, experienced, and genuinely committed to running clean organizations. When the conversation turns to fraud, the response I hear most often is not denial. It is exhaustion.

"We know it's happening. We just don't have the bandwidth to catch it."

That sentence stays with me. Because it tells the whole story. Not of negligence, but of a structural mismatch that the industry has not yet resolved. The fraud is sophisticated. The operational capacity assigned to detect it is not keeping pace. And the gap between those two realities is costing U.S. insurers more than most are willing to say out loud.

The Number Nobody Wants to Own

Let me put a figure on the table.

According to the Coalition Against Insurance Fraud, insurance fraud costs the United States $308.6 billion annually. Not $308 million. Not across a decade. Every single year.

To put that in context: that figure exceeds the annual GDP of more than 140 countries. It is not a rounding error. It is a structural drain on an industry that serves tens of millions of Americans at the most vulnerable moments of their lives.

What makes this number even more significant is how it got there. The last major estimate, $80 billion published in 1995, was already staggering for its time. Adjusted purely for inflation, that figure would reach roughly $155 billion today. The actual number is more than double that. The difference is not explained by inflation. It is explained by the internet, by organized criminal networks that have gone fully digital, by state-sponsored fraud rings, and by a litigation environment that has changed fundamentally in the past decade.

Fraud has professionalized. The operational response to it, in most carriers, has not.

What Is Actually Driving It, and Why It Is Getting Harder to Catch

There is a common misconception that insurance fraud is primarily an individual problem. A policyholder inflating a claim. A contractor padding an invoice. Those cases exist and they matter. But the growth in fraud volume over the past fifteen years has been driven by something more organized and more difficult to detect.

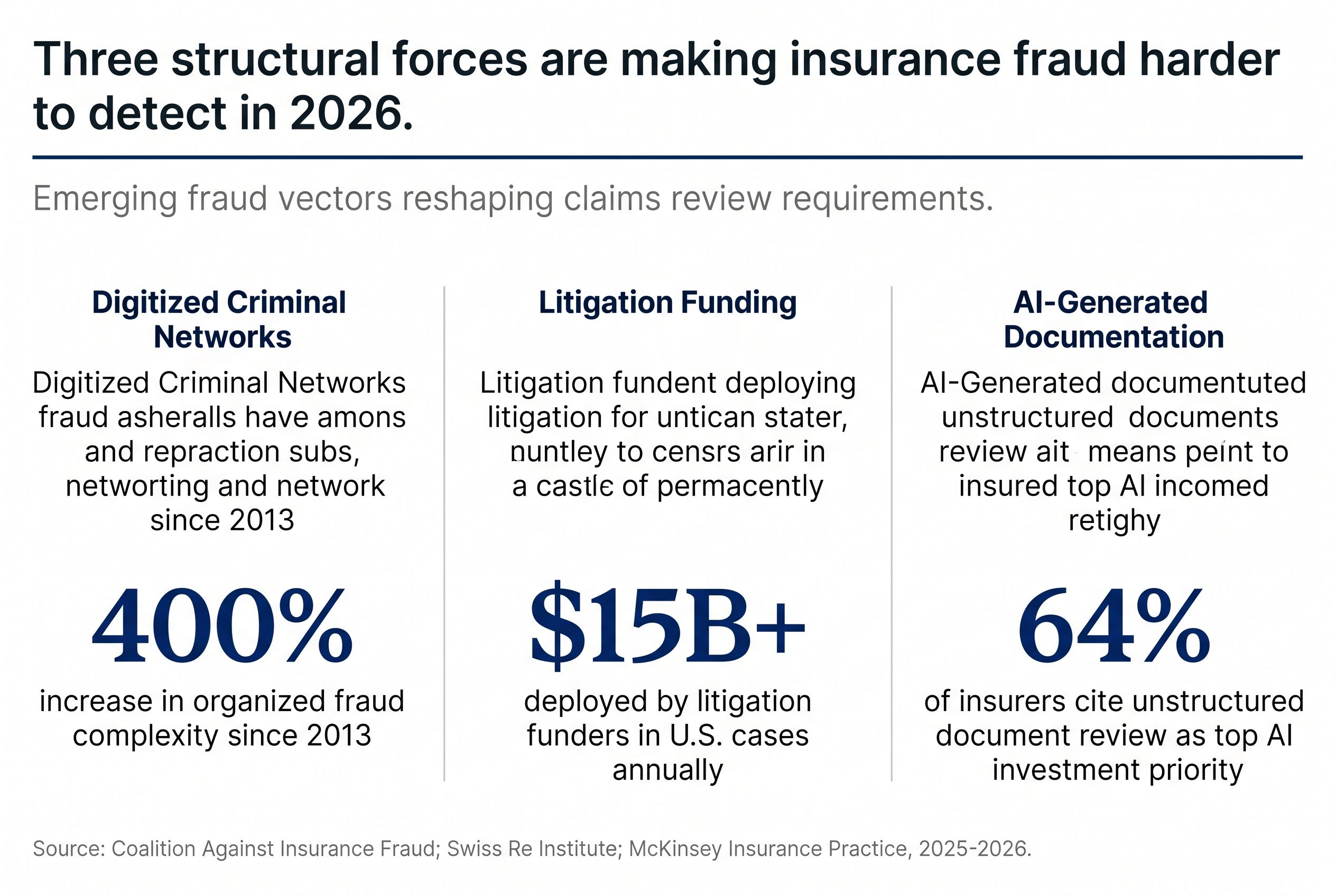

Organized crime has moved online. Criminal syndicates that once operated through physical pressure have reinvented themselves as digital fraud operations. Some are sponsored by state actors. Others operate as sophisticated networks that identify potential claimants, pair them with unscrupulous legal representation, and manufacture claims with documentation that is increasingly difficult to distinguish from legitimate filings.

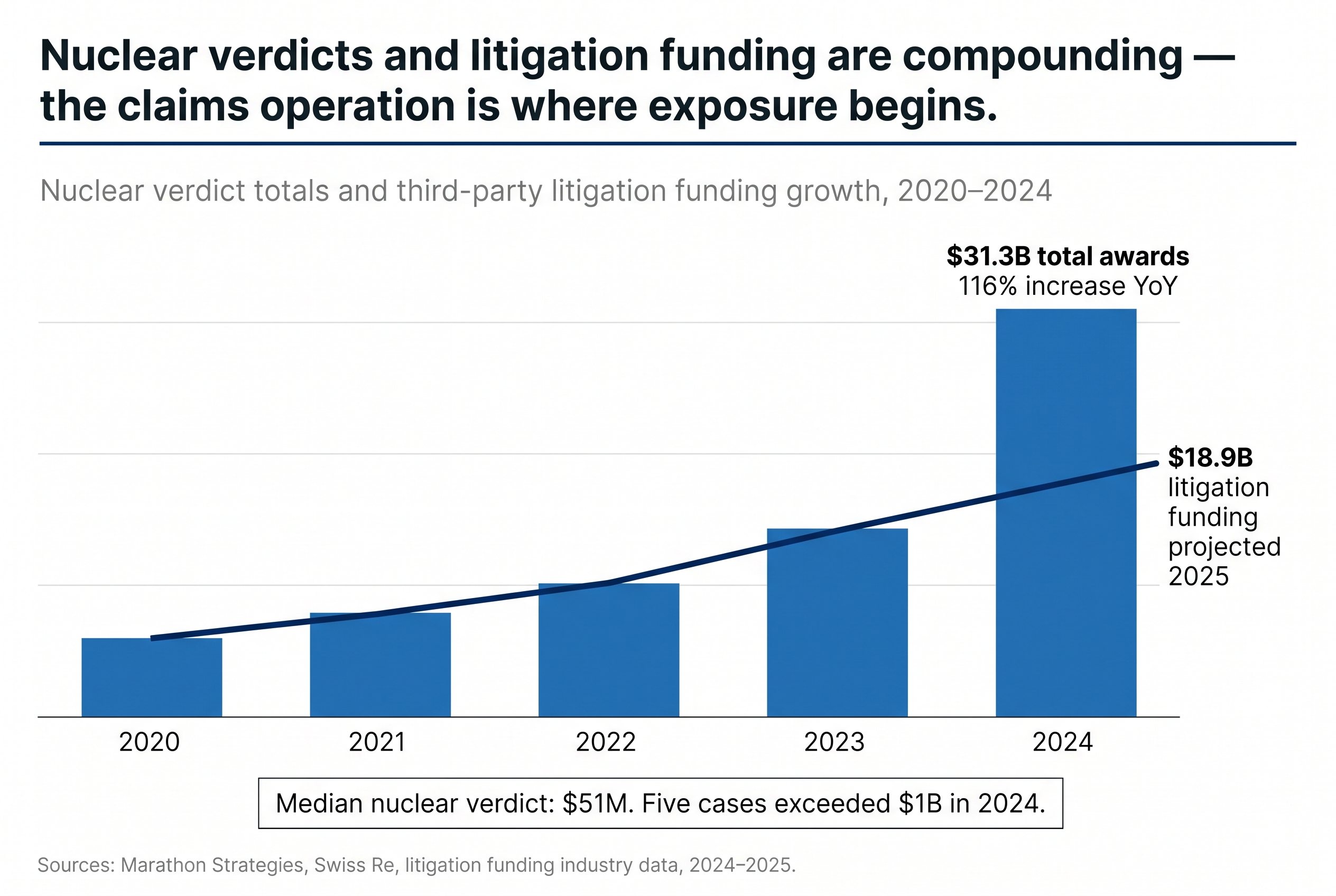

Litigation funding has changed the economics of fraud. Third-party litigation funders, investors who pay legal costs in exchange for a percentage of settlement proceeds, have made it financially viable to pursue fraudulent claims that would have previously been abandoned. The plaintiff only repays the funder if they win. The result is a professionally financed adversarial environment that many carriers are structurally unprepared to match.

AI-generated documentation is an emerging frontier. The same capabilities that are transforming legitimate insurance operations are being used to fabricate supporting documentation, synthesize medical records, and manufacture the paper trail that a claim requires. Detection requires pattern recognition at scale, which is exactly the kind of work that exhausted in-house teams, buried under legitimate claim volume, are least positioned to perform consistently.

The carriers catching the most fraud are not necessarily the ones with the best investigators. They are the ones with the operational capacity to actually look.

The Real Cost Is Not Only Financial

When fraud goes undetected, it does not just drain reserves. It raises premiums for every honest policyholder on the book. It increases the cost of claims for the carriers who serve them. It lengthens processing times for legitimate claimants, real people often in crisis, who are waiting for a resolution while their file sits in a queue behind fraudulent ones consuming disproportionate adjuster bandwidth.

This connection matters. As explored in Social Inflation Is Not a Legal Problem. It Is a Claims Operations Problem, nuclear verdicts are not made in courtrooms. They are shaped months earlier by operational decisions most carriers are not tracking closely enough. Fraud sits inside that same operational blind spot. It is not a legal or actuarial problem waiting at the finish line. It is an operations problem embedded in the daily work of the claims queue.

The carriers that resolve claims quickly, accurately, and empathetically are the ones who keep policyholders. The ones who cannot, because their teams are overwhelmed and fraud is consuming resources that should serve legitimate claimants, pay for it in lapse rates and trust long before they see it in the loss ratio.

Why the Talent Crisis Makes This Worse

This problem does not exist in isolation from the broader workforce pressure the U.S. insurance industry is absorbing right now.

The U.S. Bureau of Labor Statistics projects the industry will lose approximately 400,000 workers through attrition. The median age of insurance industry employees is 45. One in four workers is already 55 or older. The pipeline is not replacing them at anything close to the required rate.

That constraint hits hardest precisely where fraud detection lives: in experienced adjusters, SIU professionals, and claims reviewers who carry years of pattern recognition that no software fully replicates. As examined in The 400,000 Professionals Leaving Insurance Are Not Taking Jobs With Them. They Are Taking Judgment, the headcount can eventually be replaced. The judgment those professionals carry cannot be easily transferred, documented, or automated.

When those people retire, or when they are overwhelmed by volume, the blind spot in fraud detection grows. Not because carriers stopped caring. Because the operational capacity to scrutinize what is in the queue quietly contracts.

The Cost Problem Underneath the Fraud Problem

There is another layer here that deserves attention.

Most carriers facing fraud exposure are simultaneously facing pressure on operational cost. The instinct under cost pressure is to consolidate, reduce headcount, and rely on existing teams to absorb more. That instinct is understandable. It is also precisely the wrong response when the problem is insufficient scrutiny capacity.

As discussed in The Carriers Winning on Cost Are Not Cutting Headcount. They Are Rethinking Where Work Belongs, the carriers performing best on cost efficiency are not the ones that have simply reduced their workforce. They are the ones asking a harder and more precise question: does this work belong here, with these people, at this cost structure? That reframe changes what operational decisions are available.

Applied to fraud detection, the question is not whether to invest in scrutiny capacity. The data is unambiguous that the cost of under-investing is far greater than the cost of the investment itself. The question is what the right structure for that capacity looks like given the talent constraints, cost pressures, and volume variability every carrier is currently managing.

What Effective Fraud Detection Operations Actually Look Like

The most effective fraud detection operations are not characterized by more sophisticated technology alone. Technology matters, including pattern recognition, document AI, and anomaly flagging, but technology without trained human review at scale produces false positives that consume as much time as they save. The operations that perform best combine both.

What separates high-performing fraud detection from average is not a single tool or a single team. It is consistent operational discipline applied at volume. The ability to maintain dedicated review bandwidth regardless of claim volume spikes. The ability to apply consistent flagging criteria across every file, not just the ones that happen to land on the desk of the right reviewer on the right day. The ability to sustain that coverage without depending entirely on institutional knowledge that is walking toward retirement.

This is also why the compliance dimension of fraud detection cannot be separated from the operational one. The regulatory environment governing how insurers investigate, document, and report suspected fraud is itself becoming more demanding. As covered in The Compliance Maintenance Burden Is Growing Faster Than Compliance Teams Can Scale, regulations no longer arrive as discrete events to implement. They arrive continuously. The carriers managing the gap with exposure are taking on risk they may not have fully priced.

The Strategic Reframe Executives Need

Insurance fraud is consistently discussed as a compliance problem or a financial problem. It is both. But it is also, fundamentally, an operations problem. And operations problems have operations solutions.

The $308.6 billion figure will not be resolved by any single carrier acting alone. But each carrier has meaningful influence over how much of that figure comes from their own book, and how much of their legitimate claimant base absorbs the cost of fraud that was never caught.

The carriers performing best on fraud containment are not the ones with the largest SIU departments. They are the ones who have built sufficient operational capacity to actually examine what is in the queue. To apply consistent scrutiny. To maintain that scrutiny even when volume spikes, even when key personnel turn over, even when the caseload of legitimate claims would otherwise consume every available hour.

That is not a technology story. That is an operational discipline story. And it is one that every carrier serving the U.S. market needs to be writing for themselves now, before the blind spot gets any larger.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.