The Carriers Winning on Cost Are Not Cutting Headcount. They Are Rethinking Where Work Belongs.

When combined ratios come under pressure, the instinct in most carrier organizations follows a predictable sequence. Underwriting tightens. Rate increases are filed. And somewhere in the executive conversation, headcount reduction surfaces as a lever. In the first quarter of 2026 alone, over 11,000 employees were laid off across insurance companies, with additional reductions announced through February and March. The cost pressure driving those decisions is real. The method is, in most cases, the wrong response to the right problem.

The carriers that are actually moving their expense ratios in a durable direction are not primarily doing it through workforce reduction. They are doing it through a fundamentally different question: not how many people do we need, but where does each category of work actually belong in our operating model?

That question produces a different answer than headcount analysis, and it produces better results. The distinction matters because the two approaches have opposite effects on what the carrier actually needs most in a difficult market: operational quality, compliance precision, and the judgment-intensive work that drives underwriting performance and claims outcomes.

The Expense Ratio Gap Is Structural, Not Cyclical

The performance spread between top-performing and lagging carriers on expense ratio is not primarily a function of market conditions. It is a function of operating model design.

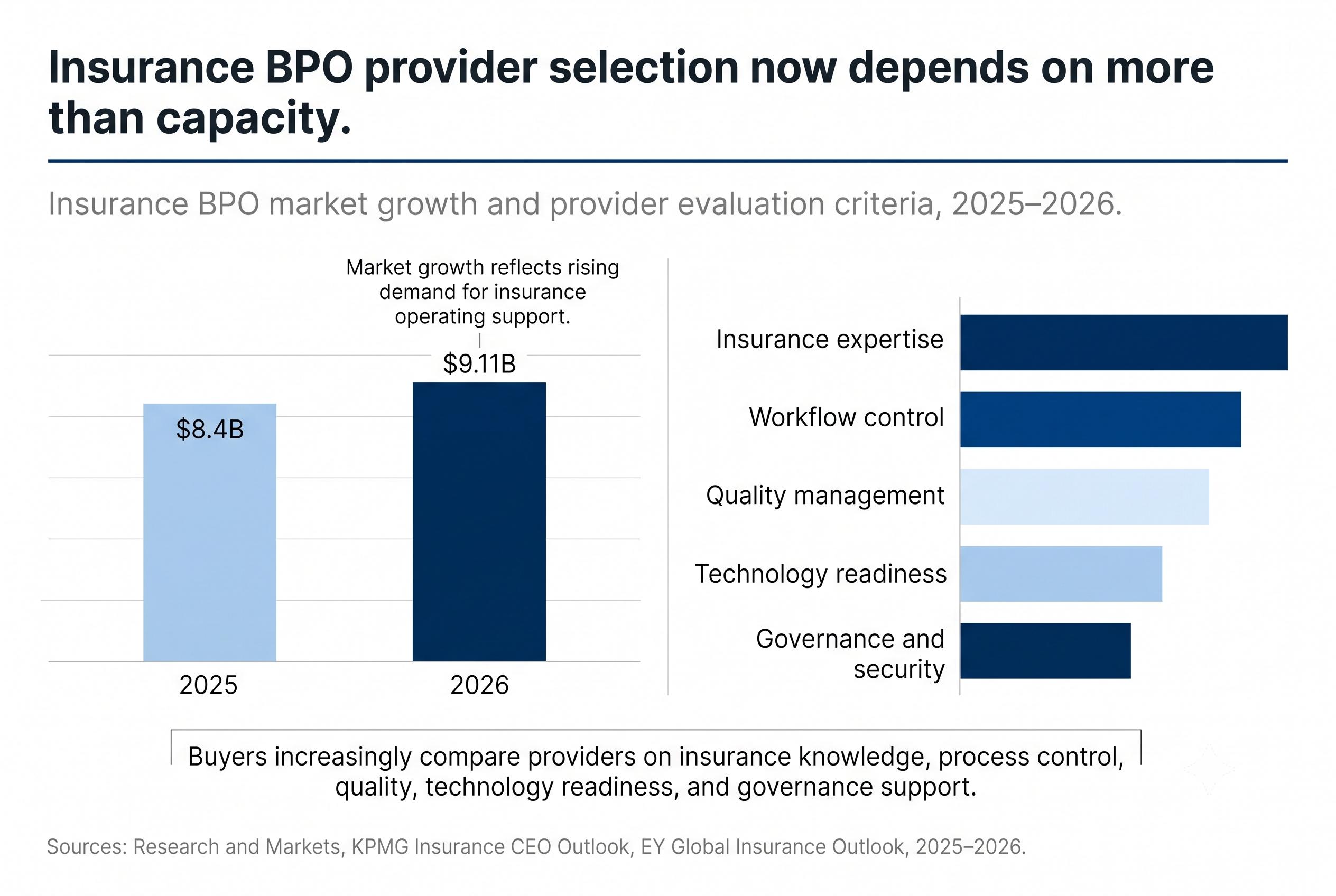

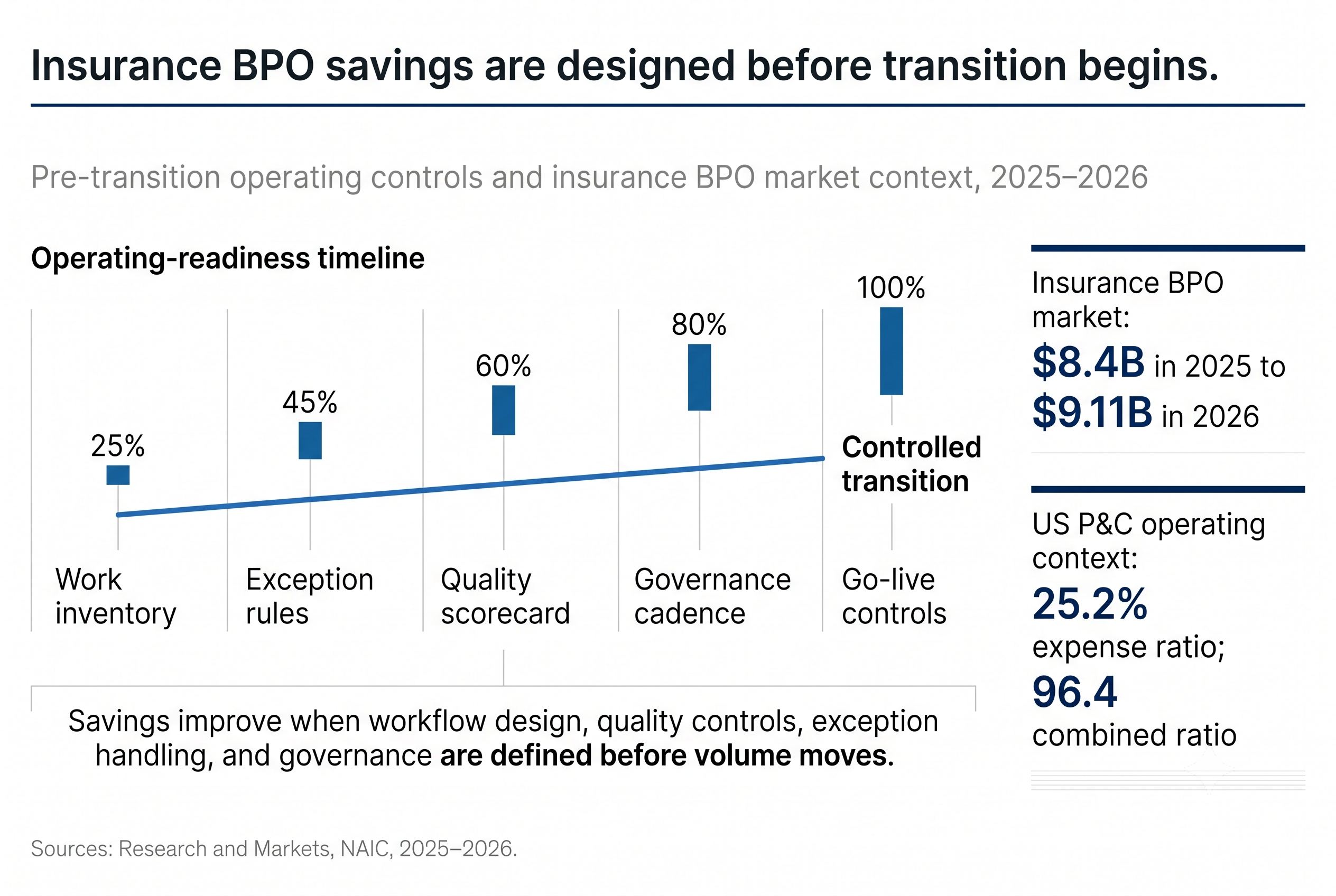

PwC analysis has documented that top-performing insurers carry average expense ratios of approximately 24 percent, while middle-tier carriers average 27 percent and laggards reach 32 percent. That eight-point gap between leaders and laggards represents a structural cost disadvantage that compounds across every premium dollar the lagging carrier writes. McKinsey analysis has found that operating expenses at the industry's top-performing carriers are typically around 60 percent lower than at the lowest-performing companies.

Those gaps do not close through periodic workforce reductions. They close through fundamental differences in how work is organized, assigned, and executed. The carriers at 24 percent are not staffed at a dramatically lower headcount than those at 32 percent. They are structured differently, in ways that eliminate cost at the process and workflow level rather than through the blunt instrument of reducing bodies against a workload that remains unchanged.

Deloitte's 2026 insurance outlook projects the U.S. P&C combined ratio deteriorating from 97.2 percent in 2024 to approximately 99 percent in 2026, driven by persistent cost pressures from trade policy uncertainty, labor shortages, and supply chain disruption. In that environment, carriers whose expense ratios are structurally elevated face compounding pressure from both sides of the combined ratio simultaneously. The window for making structural operating model changes before the pressure becomes a crisis is narrowing.

What Disaggregation Actually Means in Practice

Swiss Re's 2025 P&C market analysis identified a structural shift already underway in carrier operating models: functions formerly performed by vertically integrated carriers are disaggregating, with tasks being allocated to differentiated players offering specialization and technology. That observation captures the direction correctly. What it understates is how deliberate and precise that disaggregation needs to be to produce the expense ratio improvements carriers are seeking.

The logic of disaggregation is not the same as the logic of outsourcing everything that is not underwriting. It is more specific than that, and the carriers that have implemented it well understand the distinction precisely.

Work in an insurance operation exists on a spectrum defined by two variables: the degree to which it requires insurance-specific domain knowledge, and the degree to which it requires carrier-specific judgment. The intersection of those two variables determines where work should sit.

Work that requires deep insurance domain knowledge and carrier-specific judgment, the kind that lives in experienced underwriters interpreting complex commercial submissions, senior claims handlers managing high-stakes litigation exposure, or compliance professionals navigating regulatory relationships built over years of direct engagement, belongs inside the carrier's core operation. It is the work that determines competitive performance. It cannot be commoditized without direct consequence to underwriting quality, claims outcomes, and regulatory standing.

Work that requires genuine insurance domain knowledge but can be executed with consistency by a specialized partner who carries that domain expertise as a core competency, policy servicing, FNOL handling, billing and payment processing, underwriting submission intake, routine compliance documentation, belongs in a different structural position. Not because it is unimportant, but because it can be executed with equivalent or superior quality at lower cost by a partner whose entire operating model is built around doing it well. The carrier that staffs these functions with permanent full-time employees carries the fixed cost of that capacity in every quarter, regardless of volume fluctuations, surge events, or the judgment intensity of the work.

Work that is genuinely standardized and not insurance-specific belongs in automated or shared service environments that require neither domain expertise nor carrier-specific judgment to execute.

The carriers at 24 percent expense ratios have, in most cases, made these distinctions explicitly and structured their operations accordingly. The carriers at 32 percent are often still staffing the full spectrum with permanent headcount calibrated to peak demand, carrying the cost of that capacity in every period regardless of whether the work warrants it.

Why Headcount Reduction Produces Inferior Results

The appeal of headcount reduction as a cost lever is its immediacy. The savings are calculable, the timeline is defined, and the impact on the expense ratio is visible in the next reporting period.

The cost of headcount reduction as a primary expense ratio strategy is less visible and accumulates more slowly, which is precisely why it is systematically underestimated.

The first cost is operational quality degradation. When carriers reduce permanent headcount without simultaneously restructuring where work is done, the workload that the reduced team must absorb does not decrease proportionally. Cycle times lengthen. Quality review steps are compressed. Escalation protocols are followed less consistently because the adjuster or servicing associate managing a higher caseload applies judgment to prioritization in ways that expose the organization to risk. The expense ratio may improve in the short term. The loss ratio consequences of operational quality degradation typically appear six to eighteen months later, outside the planning horizon of the decision that caused them.

The second cost is the talent problem. In an environment where finance and insurance hiring sits 27 percent below its 2022 peak and 400,000 experienced professionals are retiring simultaneously, the carrier that reduces headcount through layoffs is operating in the same market it will need to hire from when volume recovers. The institutional knowledge that leaves with the laid-off employees does not return when hiring resumes. The carrier rebuilds with less experienced talent into a market that is already competitively constrained for insurance-domain expertise. The operational quality that the reduction temporarily impaired does not automatically recover when headcount is restored.

The third cost is the opportunity cost of the wrong structural problem being solved. The carrier that reduces headcount in claims processing to hit an expense ratio target has not addressed why its claims processing costs were elevated relative to peers. If the elevated cost was a function of staffing work that could be executed at lower cost by a specialized partner, the reduction provides short-term relief without correcting the structural issue. The next cycle of cost pressure will produce the same conversation about the same functions, because the operating model question was never answered.

The Structural Question Most Carrier Planning Processes Do Not Ask

The operating model question that expense ratio leaders have answered and that laggards have not is deceptively simple: for each major function in our operation, is this work best done by permanent carrier employees, by a specialized partner with insurance domain expertise, or by automated systems, and are we currently structured that way?

Most carrier planning processes evaluate cost reduction against existing structure rather than against the structure the function warrants. The question asked is typically: how do we reduce the cost of doing this the way we currently do it? The more productive question is: is this the right way to be doing this, and does the current structure reflect the best available answer to that question?

In our experience working with carriers across multiple lines and operational functions, the gap between those two questions is where the durable expense ratio improvements live. The carrier that asks the second question and answers it honestly discovers, in most cases, that a significant portion of its operations is staffed at a cost structure that does not reflect the actual requirements of the work. Policy servicing functions that require genuine insurance knowledge but not carrier-specific judgment are staffed with permanent employees carrying fully-loaded employment costs. Claims intake functions that benefit enormously from insurance domain expertise but could be executed with equivalent quality by a specialized partner are instead staffed with a fixed headcount that cannot flex with volume. Compliance documentation workflows that require precision and insurance knowledge but are repetitive in structure are managed by professionals whose time could be more productively applied to the judgment-intensive regulatory work that actually requires their specific expertise.

Restructuring those functions, not reducing them, is where the sustainable expense ratio improvement comes from. The work does not disappear. The structure changes to reflect what each category of work actually requires and where it can be executed with the highest combination of quality and cost efficiency.

The Competitive Consequence of Getting This Wrong

The combined ratio headwind Deloitte projects for 2026 and beyond is not a temporary condition from which the market will recover to more comfortable operating norms. The cost pressures driving it, labor inflation, social inflation, climate-driven claims severity, reinsurance cost increases, are structural features of the market environment, not cyclical disruptions.

In that environment, the carriers whose expense ratios are structurally aligned to the actual cost requirements of their work, rather than to the legacy structure of how the work has historically been organized, will compound their cost advantage in every successive period. The carriers that respond to each cycle of pressure with headcount reductions, while leaving the underlying operating model unchanged, will repeat the same conversation at the next inflection point.

The expense ratio gap between industry leaders and laggards has been stable at approximately eight percentage points for years. It is stable not because the laggards are not trying to close it, but because the method they are using does not address its cause. The question for carrier leadership is whether the current operating model reflects a deliberate answer to where each function belongs, or whether it reflects the accumulated decisions of how work happened to be organized at some earlier point in the carrier's history.

That distinction, not headcount, is where the expense ratio is actually determined.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.