Insurance BPO Savings Start Before the Contract Is Signed

Introduction

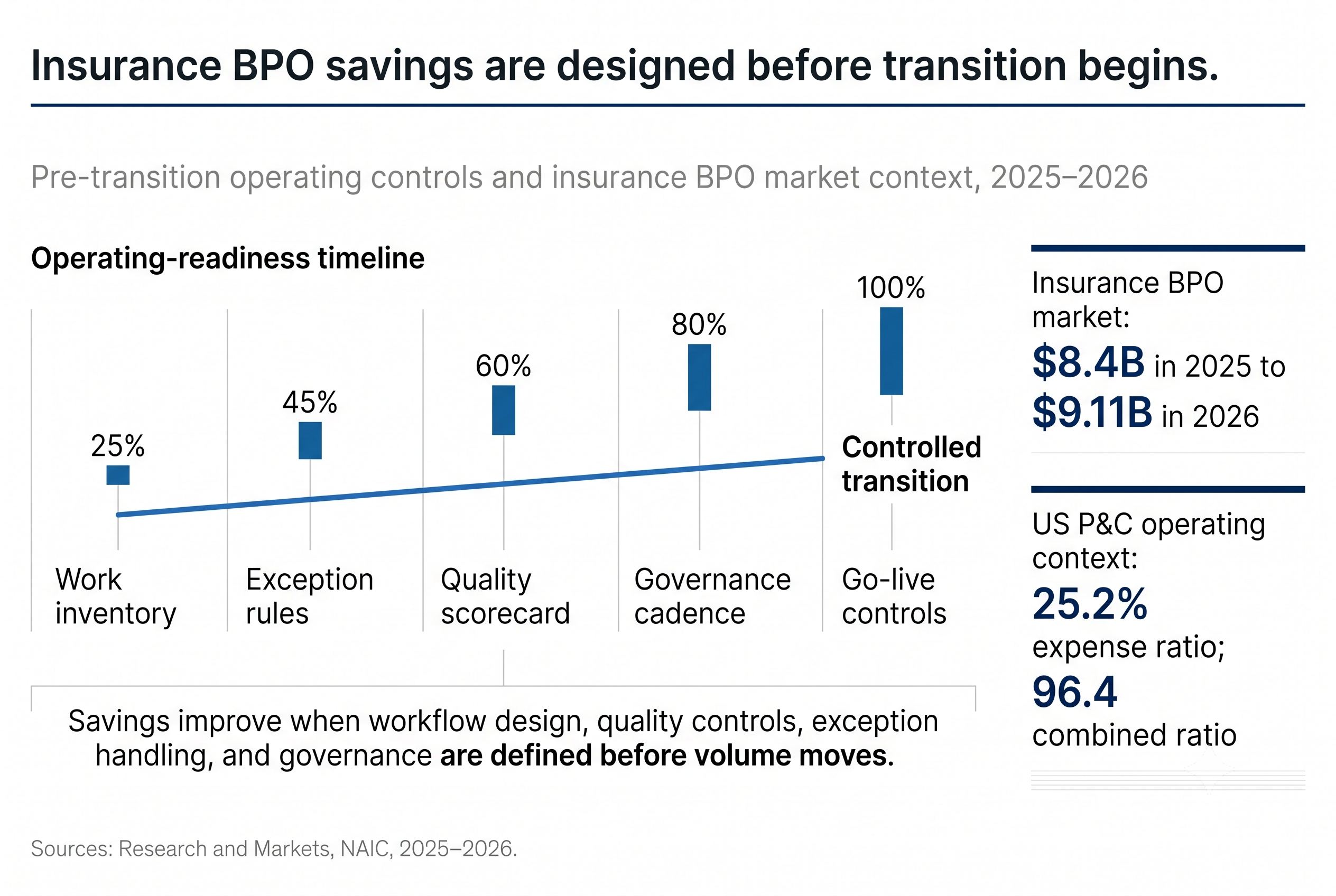

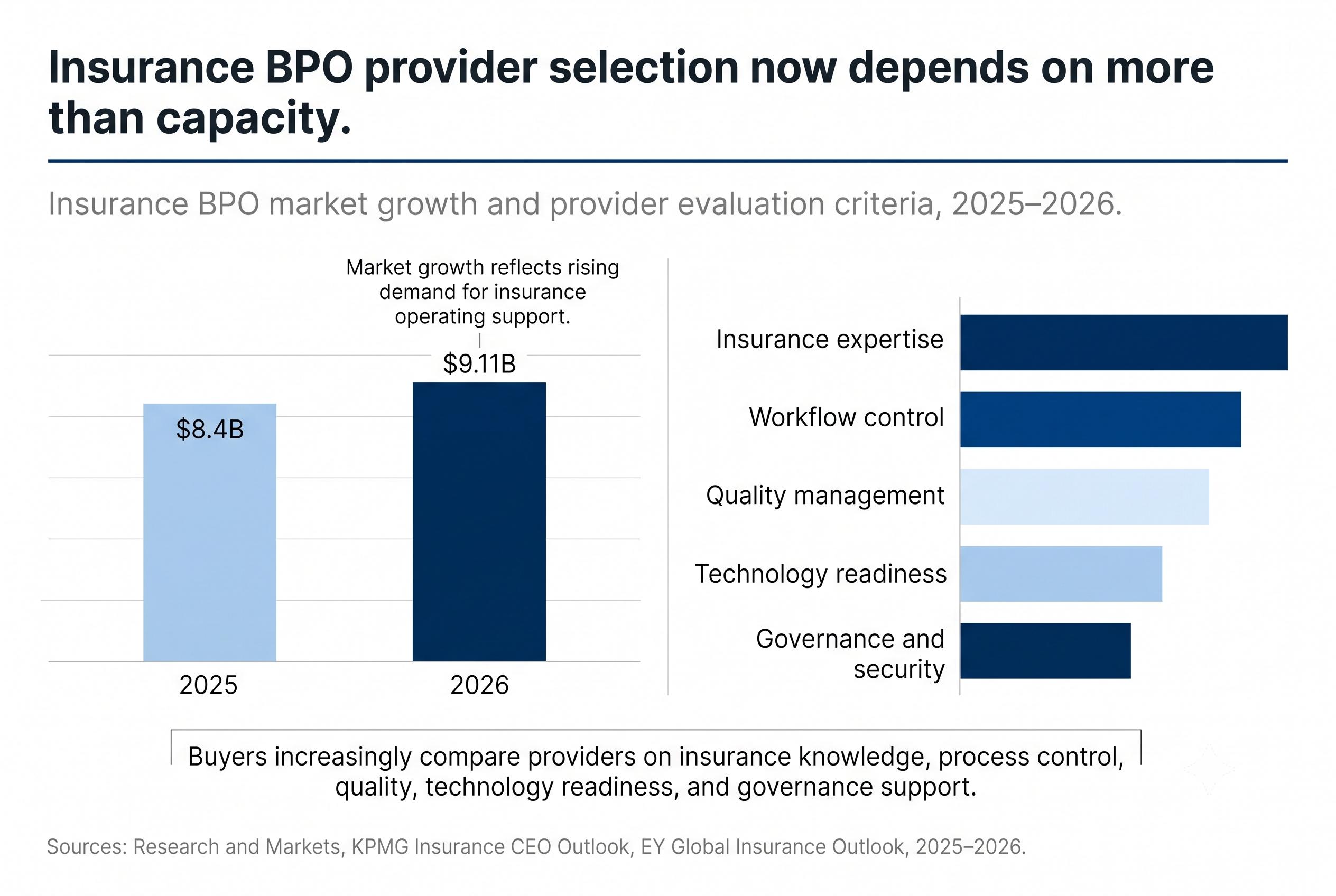

Insurance BPO delivers the most value when the operating model is designed before the work moves. The category is growing because carriers are under pressure to control expense, add capacity, improve service consistency, and support increasingly complex insurance workflows. The global insurance business process outsourcing market is projected to grow from $8.4 billion in 2025 to $9.11 billion in 2026, driven by rising operating costs, process complexity, scalability needs, and demand for specialized outsourcing talent. That growth reflects a practical reality inside insurance: carriers still need external operating capacity, but the return depends on how well the work is structured before transition begins.

The Market Is Growing Because the Pressure Is Operational

The financial pressure behind insurance BPO is visible in current industry data. The NAIC’s 2025 mid-year property and casualty analysis reported a 25.2% expense ratio and a 96.4 combined ratio for the US P&C industry, with underwriting expenses continuing to rise during the first half of the year. Even when underwriting results improve, carriers still have to manage the operating cost embedded in claims intake, policy servicing, billing, customer support, documentation, compliance, and back-office workflows.

This is where insurance BPO services can create measurable value. A carrier may need additional claims support after catastrophe activity, more consistent policy servicing during renewal cycles, or better coverage across multilingual customer service channels. Those are operating problems, not simple staffing problems. The economics improve when the outsourcing model accounts for process ownership, quality control, exception handling, training, regulatory requirements, and the way work moves between internal and external teams.

The Savings Are Designed Upstream

Most of the savings in insurance process outsourcing are created before pricing is finalized. A carrier needs to know which tasks are standardized, which tasks require licensed or experienced insurance judgment, which exceptions require escalation, and which systems create duplicate entry. Without that operating map, the BPO partner receives work that may look clean at the queue level but creates cost later through rework, billing corrections, missing documentation, customer callbacks, or compliance review.

Policy servicing is a good example. An endorsement request may touch coverage records, billing, declarations, broker communication, lienholder information, renewal data, and future claims eligibility. Treating that request as a single transaction misses the operational chain behind it. A well-designed policy servicing and retention model defines the required data, the decision rules, the handoff points, and the quality checks before the associate begins processing the request.

Rework Is Where Unit Cost Comes Back

A lower unit cost matters only when the unit is completed correctly across the full workflow. In claims, a fast intake process can still create downstream cost if the file reaches the adjuster with incomplete loss details, missing coverage information, weak triage, or inconsistent customer communication. ISSI has written about this same upstream cost problem in FNOL Is the Only Part of Claims That Drives Cost but Belongs to No One, where the intake moment determines much of the cost that later appears inside claims handling.

Current customer experience data shows how visible this fragmentation becomes. J.D. Power’s 2025 U.S. Claims Digital Experience Study found that 22% of claimants still use multiple channels to find answers to the same question, despite years of digital investment across claims. That is a customer-facing symptom of an operational issue: information, ownership, and status visibility are split across channels. The same pattern sits behind ISSI’s article on fragmentation as a cost distortion problem.

The Scorecard Has to Measure Quality, Not Activity Alone

Many insurance BPO scorecards still lean heavily on activity metrics such as average handling time, calls answered, cases completed, and transactions processed. These measures help leaders understand workload and staffing efficiency, but they do not show whether the operation is producing cleaner outcomes. A team can close more items per hour while sending more exceptions back to the carrier, increasing reopened cases, or creating additional work for billing, underwriting, claims, or compliance.

The stronger scorecard includes first-pass accuracy, reopened items, correction volume, exception aging, customer effort, quality review findings, and downstream touches per transaction. Those metrics show whether the outsourced operation is reducing total work or simply moving work across departments. The loyalty impact is measurable: J.D. Power found that 52% of auto and homeowners customers who rated their digital claims experience as “poor” or “just OK” were likely to leave or not renew, compared with 4% among customers who rated the experience “excellent” or “perfect.”

Insurance-Specific Expertise Protects the Business Case

Insurance operations carry judgment that process maps often fail to capture. A routine servicing request can involve state-specific notices, policy language, billing logic, producer communication, and documentation standards. A routine claims support task can involve coverage validation, severity indicators, fraud signals, litigation exposure, and customer sensitivity. The business case improves when the delivery team understands those details before volume increases.

This is the advantage of an insurance operations partner built around the industry’s workflows. ISSI’s insurance operations solutions cover claims operations, policy servicing, underwriting support, regulatory and compliance operations, fraud and payment integrity, sales operations, and AI workflow control. That range matters because carriers rarely experience operational cost in one isolated function. Cost usually appears between functions, where customer data, policy details, claims documentation, and compliance requirements need to remain consistent.

AI Makes the Control Layer More Valuable

AI is becoming part of the operating model carriers are asking BPO partners to support. KPMG’s 2025 Insurance CEO Outlook found that 73% of insurance CEOs are prioritizing AI investments to streamline underwriting, claims, and customer experience, while 77% identify workforce transformation and AI upskilling as a top constraint and growth opportunity. Those numbers show why insurance support services increasingly need to combine people, workflow design, and AI oversight instead of treating delivery capacity as a standalone resource.

AI follows the operating logic it is given. Clean workflows, clear escalation rules, complete documentation, and experienced human review produce better AI-supported outcomes. Weak exception logic and inconsistent data create avoidable review volume. ISSI has covered this control issue in AI in Claims Is Working Exactly as Designed. That’s the Problem, and the same principle applies across underwriting support, servicing, compliance, and claims. A carrier evaluating AI operations and workflow control should look closely at how the partner manages human review, audit trails, model supervision, exception queues, and quality feedback loops.

What Carriers Should Prepare Before Outsourcing Insurance Operations

Before expanding an insurance BPO relationship, carriers should prepare the operating model with the same discipline used for a system implementation. The work inventory should identify repeatable tasks, judgment-based tasks, exception types, system dependencies, documentation requirements, regulatory triggers, and quality control points. The transition plan should explain how institutional knowledge will be captured from experienced employees, how associates will be trained, and how performance will be reviewed after go-live.

The most useful commercial conversation is usually the operational one. Which workflows create the most rework today? Where do customers repeat information? Which servicing tasks create billing corrections? Which claim files reopen because intake was incomplete? Which compliance reviews happen too late in the process? A strong insurance BPO model gives the carrier visibility into those questions before the work is moved, then uses that visibility to improve quality, cost, and scalability over time.

Closing Perspective

Insurance BPO savings start with design, not transaction pricing. The carriers that get durable value from outsourcing define the work clearly, preserve insurance judgment, measure quality across the full workflow, and build governance around the points where cost usually leaks: handoffs, exceptions, rework, customer communication, and compliance documentation.

The case for insurance BPO is strongest when the partner helps the carrier improve how operations actually run. Lower unit cost can help the budget. A better operating model can improve the economics of claims, policy servicing, customer support, compliance, and back-office work at the same time. For carriers reviewing where their operations need more consistency, capacity, or control, ISSI’s insurance operations solutions provide a practical starting point for evaluating the full workflow before isolated cost problems become embedded across the organization.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.