What Makes an Insurance BPO Provider Different?

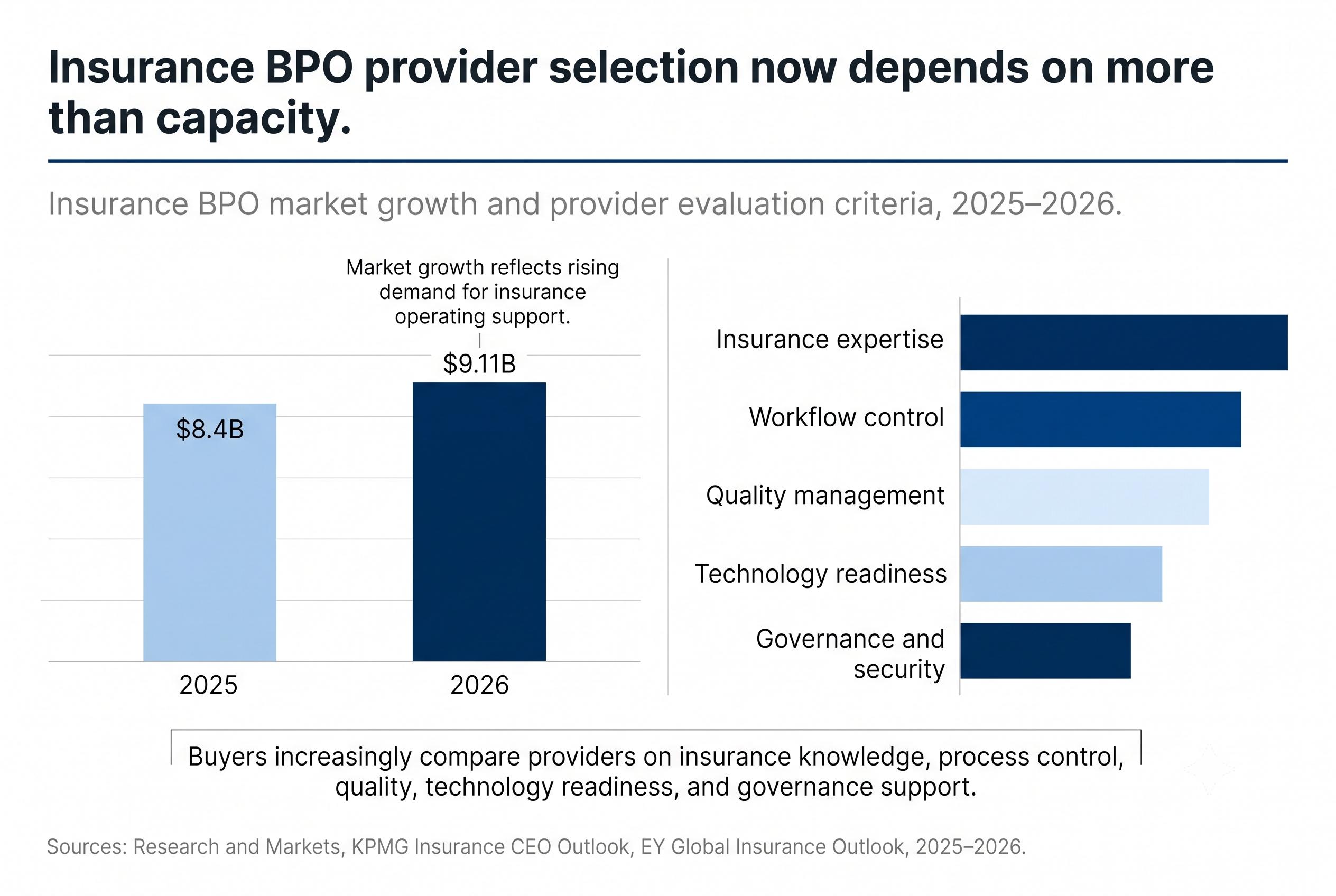

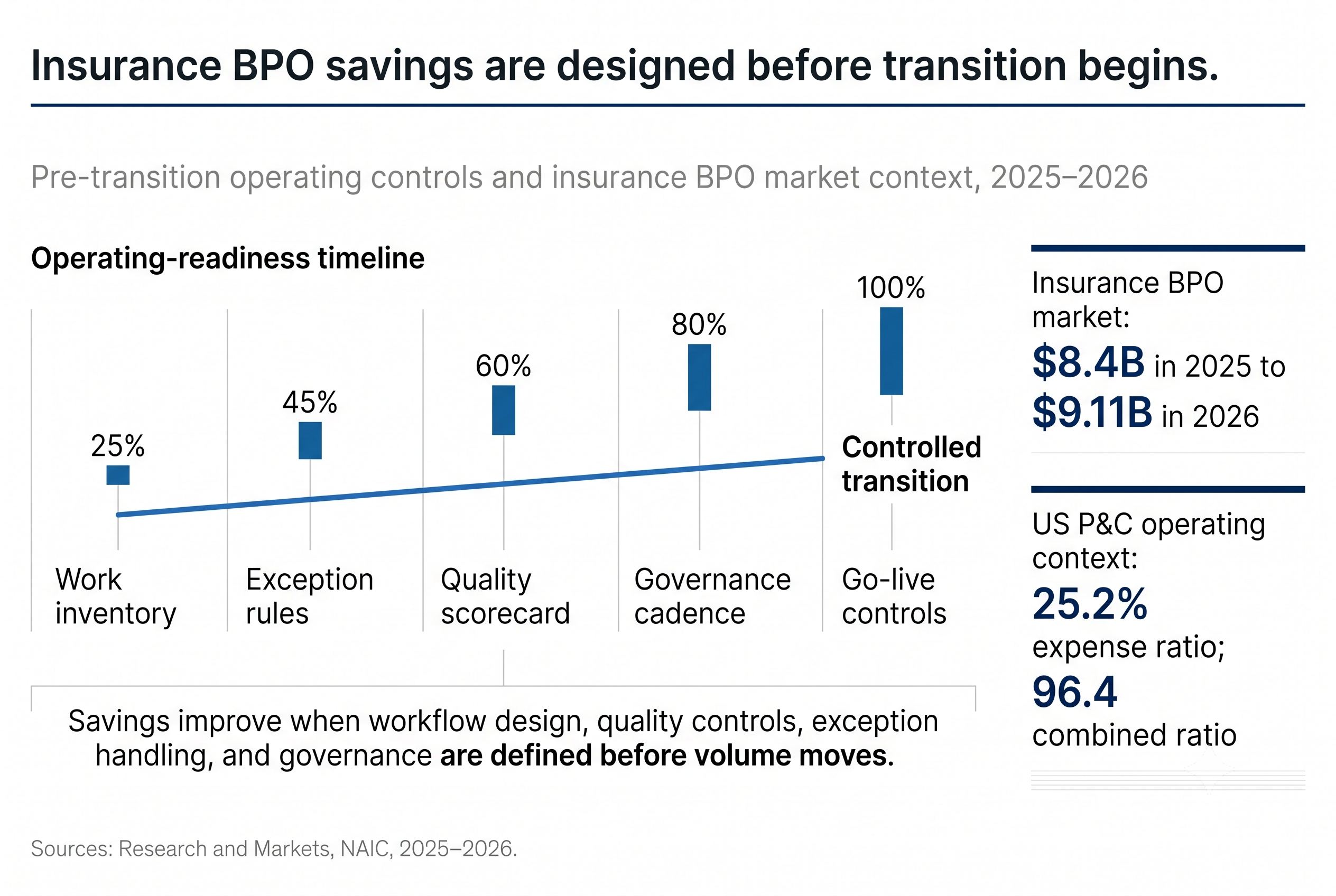

The phrase insurance BPO provider sounds broad, but buyers are usually asking a more specific question. They want to know which partner can support insurance work without creating extra friction across claims, policy servicing, customer support, compliance, and documentation. Google Search Console is already showing ISSI for that type of commercial search, and the broader market context explains why. The global insurance business process outsourcing market is projected to reach $9.11 billion in 2026, up from $8.4 billion in 2025, with growth tied to rising process complexity, outsourcing demand, and expanding service scope across policy administration, claim processing, customer service, underwriting support, data entry, and document management.

The Category Has Shifted From Labor to Operating Capability

Insurance leaders are not evaluating providers in the same way they did a decade ago. KPMG’s 2025 Insurance CEO Outlook found that 82% of insurance CEOs are confident in company growth, while the same report shows they are balancing technology investment, cost efficiency, claims handling, and customer loyalty at the same time. That combination changes what carriers need from partners. A provider now has to fit into a more connected operating model, where service quality, workflow discipline, and business continuity matter as much as staffing capacity.

That shift is visible in what the market now includes. Research and Markets describes the insurance BPO category as covering policy administration, claim processing, customer service, underwriting support, data entry, and document management. This is a much broader operating footprint than the older view of BPO as a narrow back office function. A carrier choosing a provider today is often evaluating whether that partner can support the flow of work across multiple functions, not only complete isolated tasks.

Insurance Expertise Shows Up in Routine Work

Insurance work looks standardized until a routine transaction hits an exception. A policy change may affect billing, declarations, underwriting records, lienholder information, renewal timing, and future claims eligibility. A claims support request may involve missing documentation, status visibility, customer communication, payment review, or fraud signals. What separates one insurance BPO provider from another is often the ability to recognize when the task is straightforward and when it requires escalation, added documentation, or a different review path.

That point matters more as insurance operations become more data and technology driven. EY’s 2025 Global Insurance Outlook notes that regulatory changes and rising customer expectations mean sophisticated tooling and rich data sets need to underpin every aspect of the insurance enterprise. In practice, that means the provider has to understand how the workflow works inside the carrier environment, not only how to execute a single transaction.

Quality Control Is Part of the Provider Decision

A strong provider relationship is defined by the work that does not come back. Volume metrics still matter, but completed transactions, handled calls, or processed files do not fully explain whether the operation is improving. In insurance, rework creates cost quickly because one correction can trigger a second review in billing, claims, compliance, or customer support. The better indicator is whether the provider helps reduce reopened cases, correction volume, exception aging, and repeat contacts.

This is where customer communication becomes a useful proxy for operating quality. In J.D. Power’s 2025 Insurance Customer Retention Playbook, customers who rate communications during the claims experience as very easy score 793 in overall satisfaction, compared with 514 when communications are not very easy. The gap is large because the customer experiences process clarity and service quality as one thing. A provider that improves documentation quality, status visibility, and communication handoffs is influencing retention as well as productivity.

Technology Readiness Now Matters in Provider Selection

Technology no longer sits outside the provider decision. KPMG found that more than 73% of insurance CEOs say AI is a top investment priority, and 67% expect returns from AI investments within one to three years. That means carriers increasingly need partners that can work inside AI enabled environments across claims, customer service, underwriting support, and workflow management. The practical question is no longer whether a provider can support the process. It is whether the provider can support the process while helping maintain review discipline, documentation standards, and usable outputs.

That same report found that 77% of insurance CEOs identify AI workforce readiness and upskilling as a key challenge, while 77% also say the pace of regulatory progress could become a barrier to organizational success. Those findings matter because they point to the same conclusion: providers are now being evaluated partly on whether they can operate inside environments shaped by new technology, tighter governance expectations, and evolving review requirements.

Security and Governance Are No Longer Side Questions

Provider selection also carries a larger governance burden than before. KPMG reports that 83% of insurance CEOs say the biggest barrier to organizational growth is cybercrime and cyber insecurity. EY’s 2025 Global Insurance Outlook also points to a lack of visibility into third party security infrastructure and data flows as a source of vulnerability. For carriers, this means provider quality now includes how the partner approaches data handling, process controls, auditability, and business resilience.

This does not mean carriers are looking for perfection from providers. It means they want evidence of operational discipline. Clear escalation paths, documentation standards, access controls, quality review, and transparent reporting all matter because outsourced insurance work often touches customer data, policy data, claims data, and regulated communications at the same time. A provider that can work cleanly inside those conditions is different in a way buyers can actually feel.

The Best Provider Fit Usually Looks Operational, Not Promotional

The most useful way to evaluate an insurance BPO provider is to look at how the operating model behaves under normal pressure. Can the provider absorb volume changes without losing service consistency. Can it distinguish repeatable work from judgment based work. Can it capture exceptions early enough to keep them from becoming downstream cost. Can it support digital workflows, human review, and quality feedback at the same time. These are practical questions, and they reveal more than broad positioning statements.

That is also why the best provider relationships tend to look collaborative instead of transactional. The carrier brings product knowledge, operating priorities, and business goals. The provider brings scale, workflow discipline, training structure, service management, and execution support. When those pieces fit together, outsourcing becomes part of the carrier’s operating model rather than a disconnected external function. That is where the real difference shows up.

Closing Perspective

What makes an insurance BPO provider different is rarely one headline capability. It is the provider’s ability to support insurance work with enough process discipline, quality control, technology readiness, and operating context to help the carrier scale cleanly. The market is growing because carriers need that support across more parts of the insurance lifecycle, and the provider decision is becoming more important as workflows become more connected.

For buyers, the question is practical. Which partner can help the organization move work with fewer corrections, clearer accountability, and stronger service consistency. That is usually where the difference between providers becomes visible.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.