The 400,000 Professionals Leaving Insurance Are Not Taking Jobs With Them. They Are Taking Judgment.

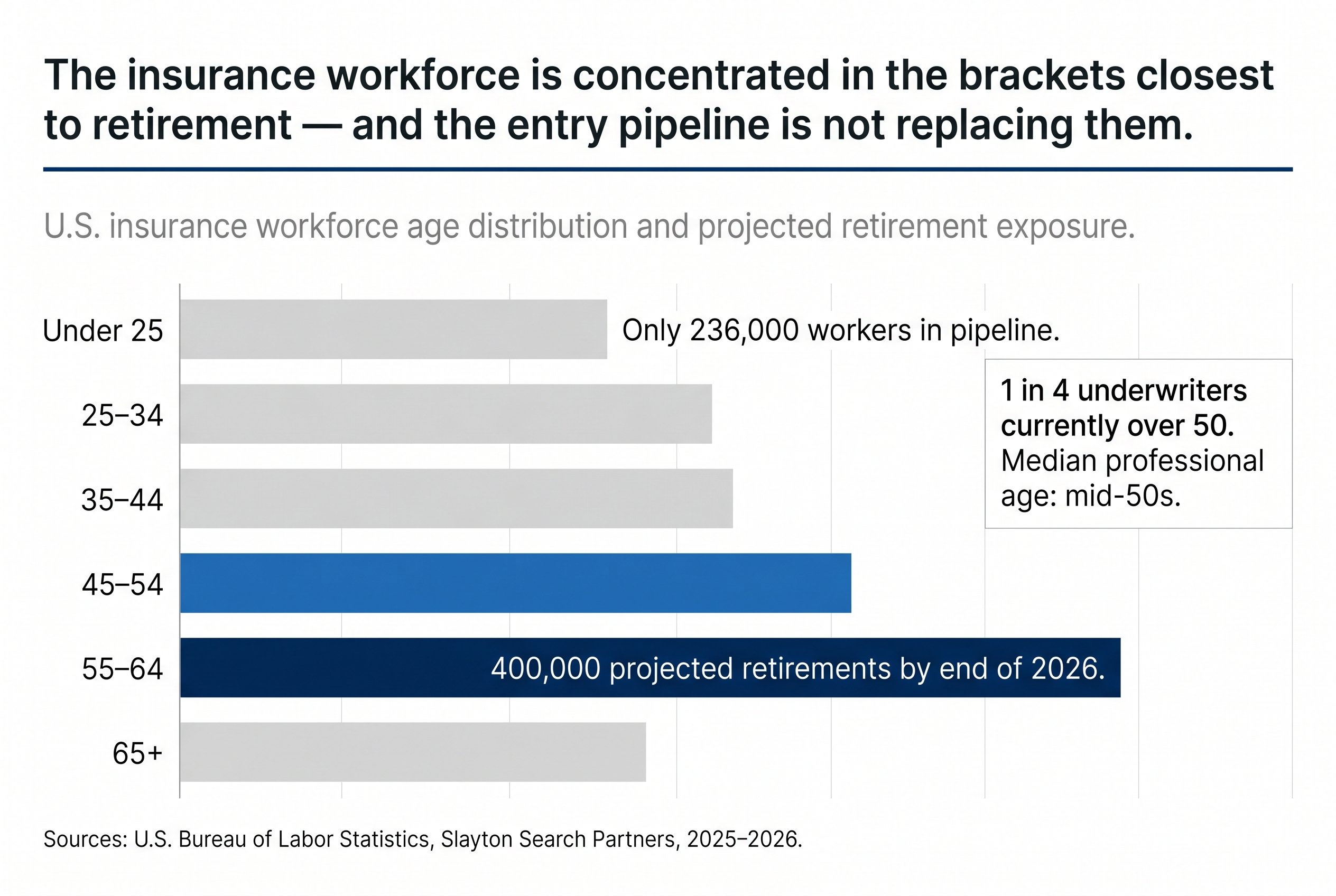

The insurance industry has discussed the retirement wave with consistent accuracy and consistent inadequacy. The number is well established. By the end of 2026, an estimated 400,000 insurance professionals will have retired in the United States since 2021, according to Bureau of Labor Statistics projections. The demographic arithmetic is not in dispute. One in four underwriters is currently over 50. The median age of the insurance professional is in the mid-50s. Roughly half of the current workforce will retire within the next fifteen years.

What the industry has discussed less honestly is the nature of what is actually leaving.

The framing has been predominantly about headcount. Carriers and agencies are losing people, and the pipeline to replace them is thin. Seventy-nine percent of Gen Z say they have never considered working in insurance. Finance and insurance hiring sat 27 percent below its 2022 peak as of 2025. These are real constraints and they deserve the attention they are receiving.

But the headcount framing understates the problem by a significant margin, because the professionals leaving the industry are not primarily taking volume with them. They are taking judgment. And judgment, in the insurance context, is not a skill that can be rebuilt on the same timeline as headcount.

What Judgment Means in an Insurance Context

The distinction between knowledge and judgment is not abstract. It has concrete operational consequences that express themselves in loss ratios, litigation exposure, and compliance performance.

Knowledge is what can be documented: policy language, coverage thresholds, regulatory requirements, claims handling protocols. Knowledge can be written down, loaded into training curricula, and transferred to new hires within a reasonable onboarding period. It is the foundation of operational competence.

Judgment is what cannot be fully documented: the underwriter who recognizes, from a combination of details in a commercial submission that no individual checklist captures, that a risk warrants a second review. The claims adjuster who identifies, from the pattern of a claimant's communications and the specific sequence of a reported incident, that the file has subrogation potential that standard workflow would miss. The compliance manager who understands, from years of direct engagement with state examiners, which regulatory ambiguities a given commissioner's office interprets conservatively and which ones carry practical tolerance.

Slayton Search's 2026 industry analysis described this precisely: the expertise leaving the workforce "lives in the veteran underwriter who instinctively knows which risks warrant a second look, or the claims adjuster who recognizes fraud patterns before losses escalate." That expertise is rarely documented because documentation cannot fully capture it. It is accumulated through market cycles, through the experience of being wrong and adjusting, through direct exposure to outcomes that training simulations do not replicate. It is, in the language that California Management Review applied to this category of expertise in March 2026, tacit knowledge: the real differentiator that no data collection program or AI training initiative can recreate from scratch.

The retirement wave is not draining headcount from the insurance industry. It is draining the tacit knowledge base on which underwriting quality, claims accuracy, and regulatory judgment depend.

Where the Gaps Are Already Visible

The downstream effects of judgment loss are not theoretical at this stage of the retirement wave. They are already measurable in specific operational domains.

In underwriting, the impact surfaces as inconsistency. Experienced underwriters make risk assessments that newer professionals cannot replicate with the same accuracy or efficiency, not because newer professionals lack training or intelligence, but because the pattern recognition that underlies accurate risk assessment requires exposure to a breadth of outcomes that takes years to accumulate. Carriers that have lost significant underwriting experience in specific lines are seeing submission review cycle times lengthen, referral rates to senior review increase, and loss ratios in those lines show variability that was not present when the experienced underwriters who set the original risk appetite were still active.

In claims, the impact surfaces as leakage and cycle time degradation. The adjuster who carries ten years of experience with a specific class of commercial liability claims can identify, within the first week of a file, the combination of factors that indicate elevated litigation risk and warrant early intervention. A newer adjuster working from documented protocols will process the same file correctly within established guidelines but without the pattern recognition that triggers the proactive steps that experienced handlers take as routine. The protocol was written by someone with the judgment to know what it was written for. The judgment itself did not transfer with the written protocol.

In compliance, the impact surfaces most acutely in multi-state operations. Regulatory relationships in insurance are built over years of direct engagement. The compliance professional who has managed examinations in a given state across multiple cycles carries an understanding of that regulator's priorities, communication style, and interpretation patterns that no documentation adequately captures. When that professional retires, the organization's compliance posture in that state does not drop to zero. It drops to whatever the written policy and the institutional memory of those who remain can sustain, which is measurably different from what it was before.

Why the Standard Responses Are Not Solving the Problem

The industry's standard responses to the retirement wave are familiar: aggressive recruiting, compensation improvements, academic pipeline development, and AI-assisted workflow automation. Each of these is genuinely valuable. None of them addresses the core problem at the pace the problem is advancing.

Recruiting addresses headcount. It does not address the judgment gap that separates a two-year associate from a fifteen-year veteran. The most effective recruiting program in the industry is producing professionals who are, by definition, years away from carrying the tacit knowledge base of the professionals they are replacing. The gap between when the experienced professional leaves and when the new hire reaches equivalent judgment depth is a structural operational exposure that no recruiting initiative closes in the near term.

Academic pipeline development is a five to ten year investment with genuine long-term value. It does not help the carrier whose senior claims team median experience drops by eight years between 2024 and 2027 as the retirement wave moves through its peak.

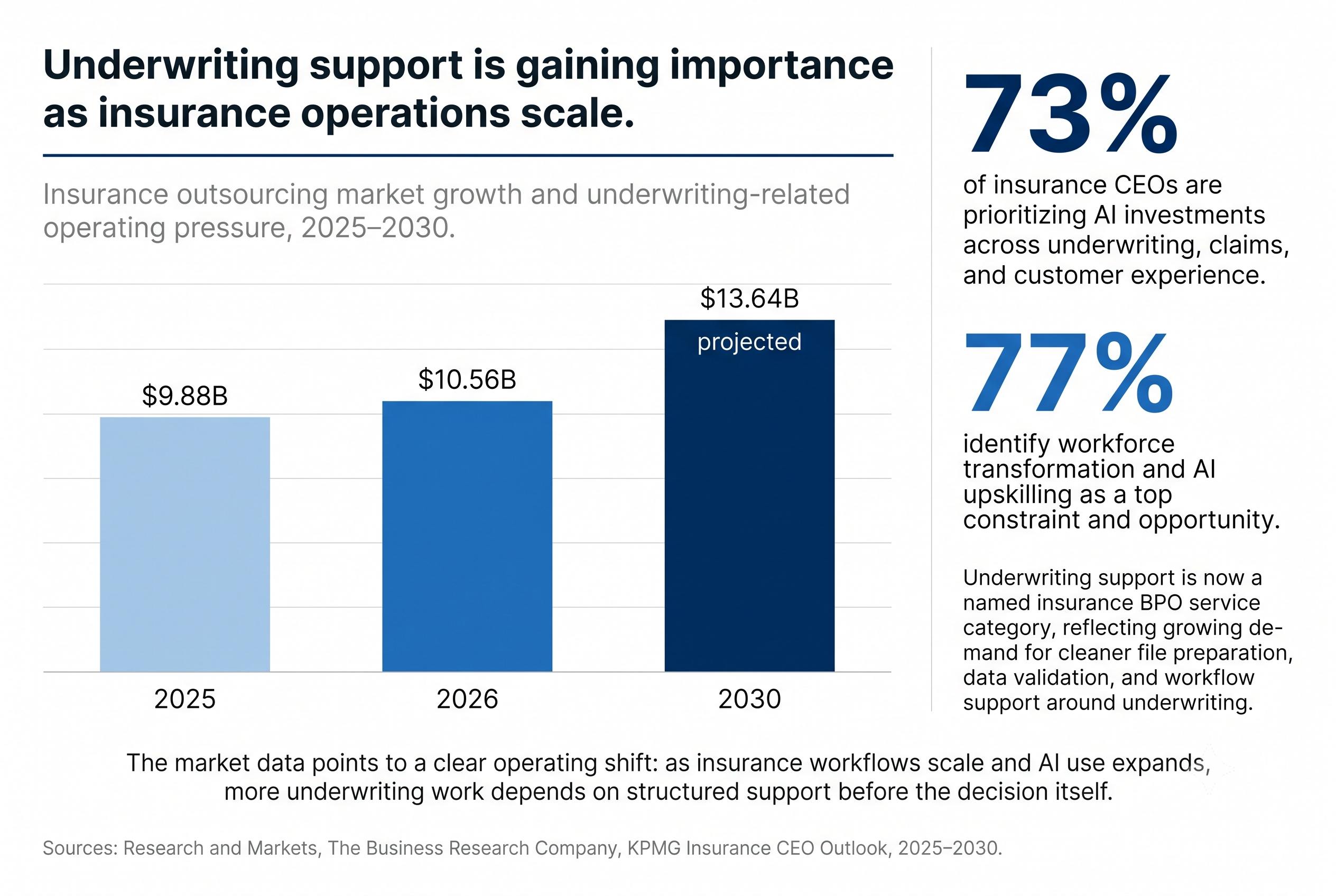

AI-assisted automation is the response that has attracted the most investment and the most inflated expectations. The honest assessment of where automation actually helps is specific: it is highly effective at reducing the administrative burden on experienced professionals, freeing them to apply their judgment to more cases rather than spending time on documentation and data entry. It is considerably less effective at replicating the judgment itself. As the California Management Review analysis noted, the tacit knowledge embedded in the decisions of experienced professionals is precisely what AI systems most need to learn from, and the window to capture it from the professionals who carry it is closing faster than most organizations have built the systems to capture it.

The carriers that are ahead of this understand something that the standard responses miss. The judgment that is leaving the industry cannot be recreated in the near term through any combination of hiring, technology, or training investment. It can, however, be retained through operational models that keep experienced professionals engaged and that structure the work so that their judgment is embedded in the workflow rather than held individually.

The Structural Response the Problem Actually Requires

The carriers managing the retirement wave most effectively share a common operational characteristic. They have moved from treating talent as a flow problem, replacing outflow with inflow, to treating it as a structural design problem: how do we organize operations so that accumulated judgment is embedded in how work is done, not held exclusively by individuals who will eventually leave?

This distinction has practical consequences for how operations are structured.

The first consequence is the design of dedicated associate teams rather than rotating pools. A model in which experienced and developing professionals work together on a defined book of business, with consistent assignment and sustained exposure to the same carrier's workflows, coverage interpretations, and risk standards, transfers judgment in a way that generalist rotation models do not. The developing professional who handles the same class of commercial accounts alongside an experienced colleague for two years absorbs contextual knowledge that no training program delivers. The judgment transfer happens through proximity and repetition, not through documentation.

The second consequence is the prioritization of retention over replacement as the primary talent strategy. The judgment base the industry is losing cannot be rebuilt at the pace it is departing. What can be slowed is the pace of departure. Carriers and operational partners that invest in work models which retain experienced professionals, through flexible arrangements, meaningful roles, and reduced administrative burden that allows judgment-intensive work to remain central, extend the window during which tacit knowledge is available for transfer. The professionals in the 55 to 64 age bracket represent, collectively, the largest concentrated knowledge asset the industry currently holds. The strategies most likely to keep them engaged longer and structure their engagement for maximum knowledge transfer are currently underinvested relative to the strategies aimed at replacing them.

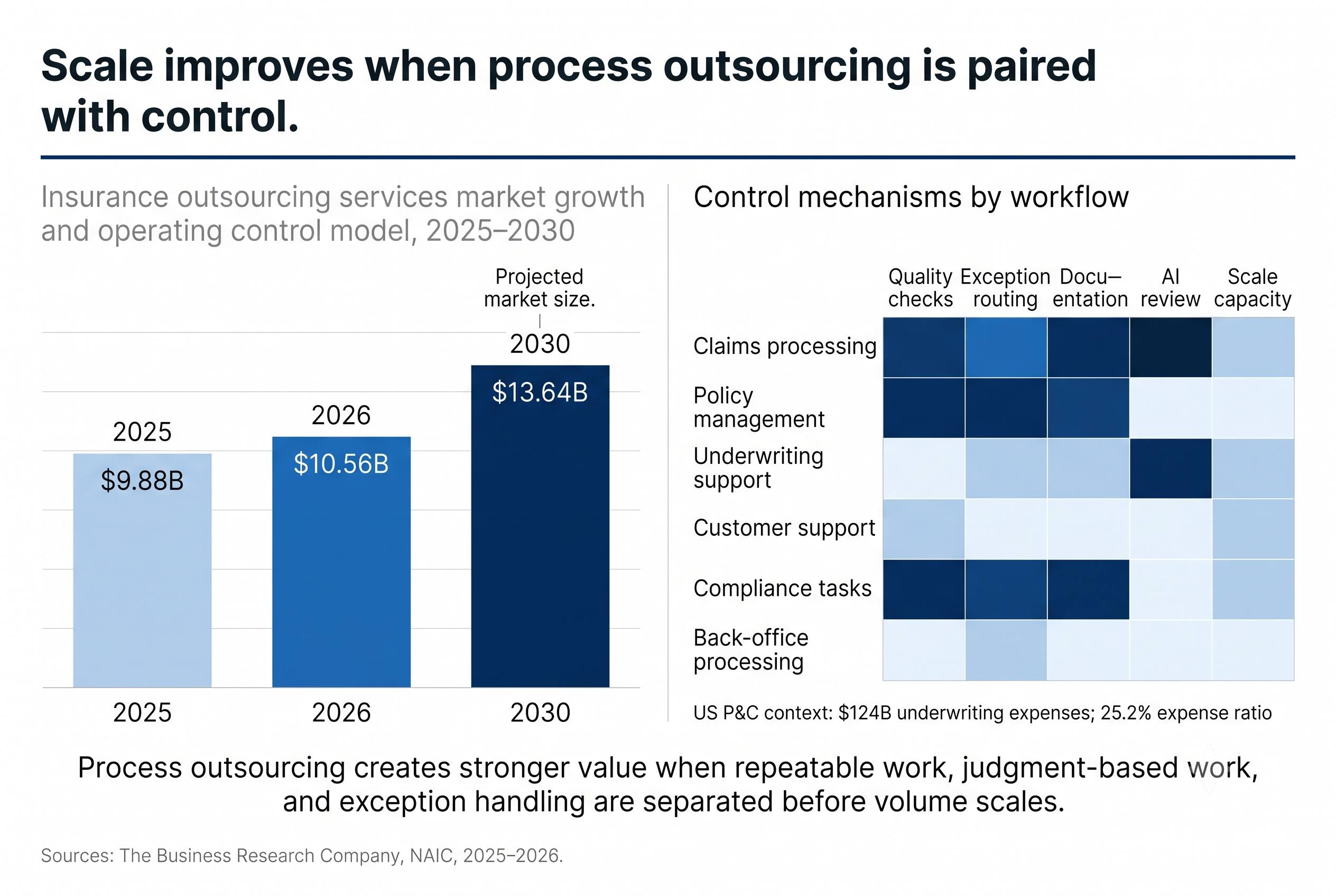

The third consequence is the willingness to partner with operational providers whose model is built around retaining insurance-domain expertise rather than scaling generic capacity. The risk in outsourced operations, which every carrier leadership team has encountered, is the partner whose associates carry shallow insurance knowledge and require sustained carrier investment to reach operational effectiveness. The alternative, a partner whose dedicated teams carry deep, sustained insurance domain experience and whose model is explicitly built around retaining and developing that expertise, produces a different outcome precisely because it addresses the judgment problem rather than treating it as someone else's concern.

The Window Is Shorter Than Planning Cycles Suggest

The Bureau of Labor Statistics projects that 1 million additional insurance professionals in the 55 to 64 age bracket will follow the current retirement wave within the next decade. Only 236,000 workers currently under the age of 25 are positioned to enter the industry in the same timeframe. The mathematics of that gap, combined with the judgment transfer timeline required to bring new entrants to genuine operational effectiveness in complex functions, suggests that the organizations with a three to five year window to act are already inside that window.

The carriers and operational partners that recognize the retirement wave as a judgment crisis rather than a headcount crisis, and that build operational models to retain, structure, and transfer accumulated expertise rather than simply hiring to fill vacancies, are making an investment that compounds in value precisely as the broader market's judgment base continues to thin.

The 400,000 professionals leaving by the end of 2026 are not the last cohort. They are the leading edge. The operational response built for this wave will determine whether the next one is manageable or destabilizing.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.