The Home Insurance Affordability Crisis Is Not a Pricing Problem. It Is an Operations Problem in Disguise

The narrative surrounding the U.S. home insurance crisis has been almost entirely framed around pricing. Premiums rose 24 percent between 2021 and 2024. Projections call for another 8 percent increase in both 2026 and 2027. Insurance now represents 9 percent of the typical homeowner's monthly mortgage payment, an all-time high. Carriers are exiting high-risk states. Insurers of last resort are absorbing policies that private markets refuse to write.

This framing is accurate. It is also incomplete in a way that matters to carrier leadership.

The pricing pressure is a consequence of climate, reinsurance costs, litigation, and construction inflation. Those forces are real and, in most cases, outside any single carrier's control. What is within a carrier's control is the operational response to the market conditions those forces have created. And that operational response, across most of the industry, has not kept pace with the scale or the speed of what is actually happening.

The carriers that understand this are not searching for relief from external conditions. They are redesigning operational models to perform in an environment where premium-driven switching, large-scale non-renewals, and surge-driven service demands are no longer exceptional. They are the new operating baseline.

The Scale of Market Disruption Carriers Are Now Operating Inside

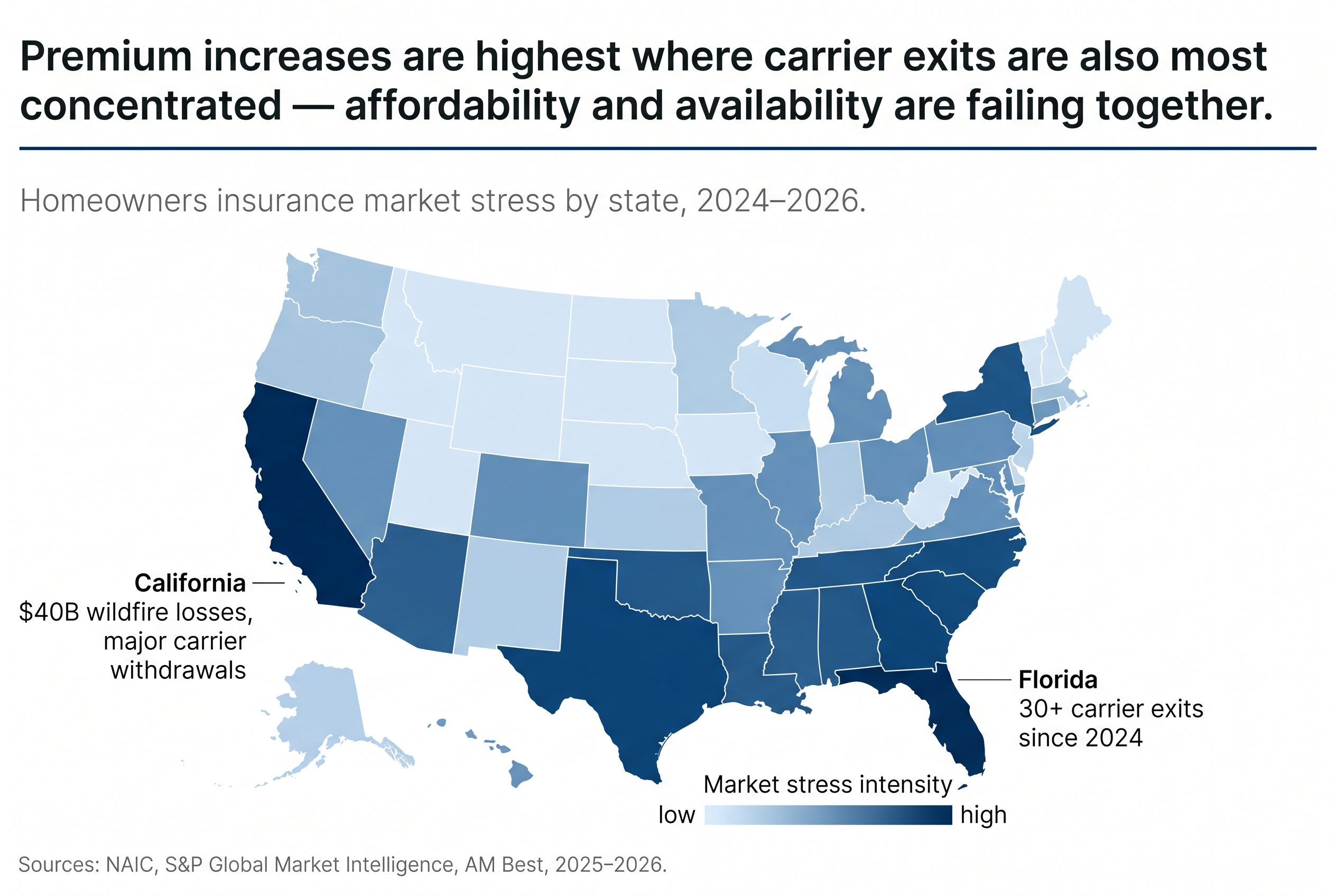

The exit of major carriers from high-risk states has not been gradual. In California, State Farm, Allstate, Farmers, Nationwide, and The Hartford have each pulled back or stopped writing new homeowners policies, citing the compounding effect of wildfire exposure, reinsurance costs, and regulatory constraints that prevented adequate rate adjustment. California wildfires in the first half of 2025 alone accounted for an estimated $40 billion in covered property losses, representing approximately 50 percent of the world's total insured natural catastrophe losses during that period.

In Florida, more than 30 home insurance companies have exited the state since May 2024. Citizens Property Insurance Corporation, the state's insurer of last resort, reached a high of 1.4 million policies in 2023 before coordinated depopulation efforts brought the count down. The carriers that have entered to absorb the market are smaller, less capitalized, and operating with different risk models than the majors they replaced.

The operational consequence of this displacement is not confined to the exiting carriers. The remaining carriers in these markets, and the carriers in adjacent markets watching the same climate and litigation dynamics begin to emerge in their own geographies, are absorbing a structurally different book of business. They are also absorbing a structurally different customer relationship. When 49 percent of policyholders report a premium increase and 43 percent of those who received an increase say they do not intend to renew, according to J.D. Power's 2025 U.S. Home Insurance Study, the volume and nature of policyholder interactions changes materially. Retention calls, billing disputes, coverage inquiries, and non-renewal processing do not scale proportionally with headcount. They surge.

The Retention Paradox That Most Carriers Are Not Managing Well

J.D. Power's intelligence data for 2026 reveals a dynamic that has significant operational implications. In 2025, 57 percent of auto insurance customers actively shopped for coverage, up from 49 percent in 2024. Unlike prior years, more of those shopping customers found lower prices and acted on them. Twenty-nine percent of insurance customers switched insurers in 2025. The market has crossed a threshold: customers who previously shopped but stayed are now shopping and leaving.

This creates a retention paradox that sits entirely within the operations function. Premium competitiveness is an underwriting and pricing decision. Whether a customer who is considering leaving actually leaves is, in most cases, an operations decision.

The data on this is consistent. TransUnion's analysis of retention drivers identifies proactive outreach about discounts, early notice of rate increases, and consistent service quality as the factors most correlated with policyholder retention decisions. None of those are underwriting outputs. All of them are operational execution outputs. A carrier whose contact center is staffed at the level required for normal volume cannot execute proactive retention outreach at the scale the current market demands while simultaneously managing the inbound volume generated by policyholders reacting to renewal notices. The two demands compete for the same capacity.

In our experience working with carriers through market disruption events, the carriers that retain the highest proportion of at-risk policyholders are not the carriers with the lowest premiums. They are the carriers whose operational infrastructure can sustain meaningful human contact at the moments when a policyholder's decision is still in motion. A policyholder who receives a 22 percent premium increase and speaks with a knowledgeable servicing associate within 24 hours of opening that notice is in a fundamentally different retention situation than one whose call goes to a queue that resolves three days later.

That gap is not a technology gap. It is a capacity and execution gap.

Non-Renewal Processing at Scale Is an Underestimated Operational Load

The industry discussion around non-renewals has focused almost entirely on the policyholder impact, which is real and significant. The operational load that mass non-renewal events create for the issuing carrier has received considerably less attention.

A non-renewal is not a simple administrative event. State-specific regulations govern the notice period, the format, and the content required. Some states mandate that carriers provide coverage continuation options or referrals to FAIR plans. Documentation requirements for non-renewal decisions vary by state and by the reason for non-renewal. In states where regulators have imposed moratoriums restricting non-renewals in declared disaster areas, the compliance requirements layered onto those decisions add further operational complexity.

When a carrier issues tens of thousands of non-renewals across multiple states in a compressed period, the resulting inbound inquiry volume, regulatory compliance burden, and documentation workload does not sit cleanly within any single operational function. It spans policy servicing, compliance, and customer contact operations simultaneously. The carriers that have pre-built operational infrastructure for non-renewal surge manage this with measurably less service degradation than those that treat it as an exceptional event to be absorbed by existing teams already operating at capacity.

The same logic applies to the carriers receiving transferred policies from exiting competitors. A book of business that moves from a departing carrier to a remaining carrier does not arrive as an orderly transfer. It arrives as a surge of new policyholders who are anxious, often inadequately informed about coverage differences, and interacting with a carrier whose systems and servicing teams may not have been calibrated for the volume or the complexity of that book. The onboarding experience in the first 90 days of that relationship is a significant determinant of whether those policyholders stay through first renewal. Most carriers understaff for it.

The CAT Season Compounding Effect

The home insurance affordability crisis does not operate in isolation from catastrophe season dynamics. It compounds with them.

Oliver Wyman reported that property claims volume surged 36 percent in 2024, driven by a 113 percent increase in catastrophe-related claims. When a major weather event strikes a market where policyholders are already anxious about coverage costs, coverage availability, and carrier stability, the contact center and claims intake volume that follows is not simply a CAT response event. It is a CAT event layered on top of a retention event, layered on top of a non-renewal processing backlog.

The carriers that handle CAT seasons well in this environment are not the carriers with the largest permanent headcount. Permanent headcount calibrated for CAT surge is permanently over-resourced for the 40 weeks per year when a major event is not active. The carriers that handle it well are those whose operational model includes pre-integrated, pre-trained surge capacity that activates at the scale the event requires and does not degrade the service levels that drive retention in the weeks immediately following.

The distinction matters because the claims experience during and after a CAT event is one of the highest-leverage retention moments in the policyholder relationship. Fewer than half of customers reported feeling that insurance is worth the price in 2024, according to P&C industry research. The claims experience is the moment that either validates or destroys that perception. A policyholder who files a claim after a wildfire or hurricane and receives fast, accurate, empathetic handling emerges from that experience with a fundamentally different disposition toward renewal than one who encounters delays, incomplete communication, and repeated contacts to resolve issues that should have been addressed on first contact.

The operational infrastructure that produces that difference is not built during the storm. It is built in the quarters before it.

The Strategic Reframe Carrier Leadership Needs

The home insurance affordability crisis is a structural market condition, not a cyclical one. The climate dynamics driving it will not reverse. The reinsurance cost pressures it generates will not reverse. The litigation environment compounding both will not reverse. The carriers that plan for a return to pre-2020 operating conditions are planning for a market that no longer exists.

The productive strategic question is not when conditions will normalize. It is how to build an operational model that performs with margin in the conditions that now define normal.

That operational model has three characteristics that distinguish it from the models most carriers built for a calmer market environment. It scales fluidly, absorbing non-renewal surges, policyholder transfer volumes, and CAT response demands without degrading core service quality. It executes proactive retention engagement at the scale and consistency the current switching environment demands, not reactively after the renewal notice has already been processed without contact. And it maintains compliance precision across the state-specific non-renewal, documentation, and coverage communication requirements that regulators are actively examining in a market they know is under stress.

None of these characteristics emerge from technology investment alone. They emerge from operational design: the deliberate construction of capacity, workflow, and execution capability that is matched to the market that actually exists, rather than the market that carriers built their models for a decade ago.

The pricing decisions will remain difficult as long as the underlying risks remain elevated. The operational decisions are within reach now. The carriers that make them are building a durable advantage in a market where the gap between operational leaders and operational laggards is widening with each renewal cycle.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.