Insurance Process Outsourcing Services Help Carriers Scale With Control

Introduction

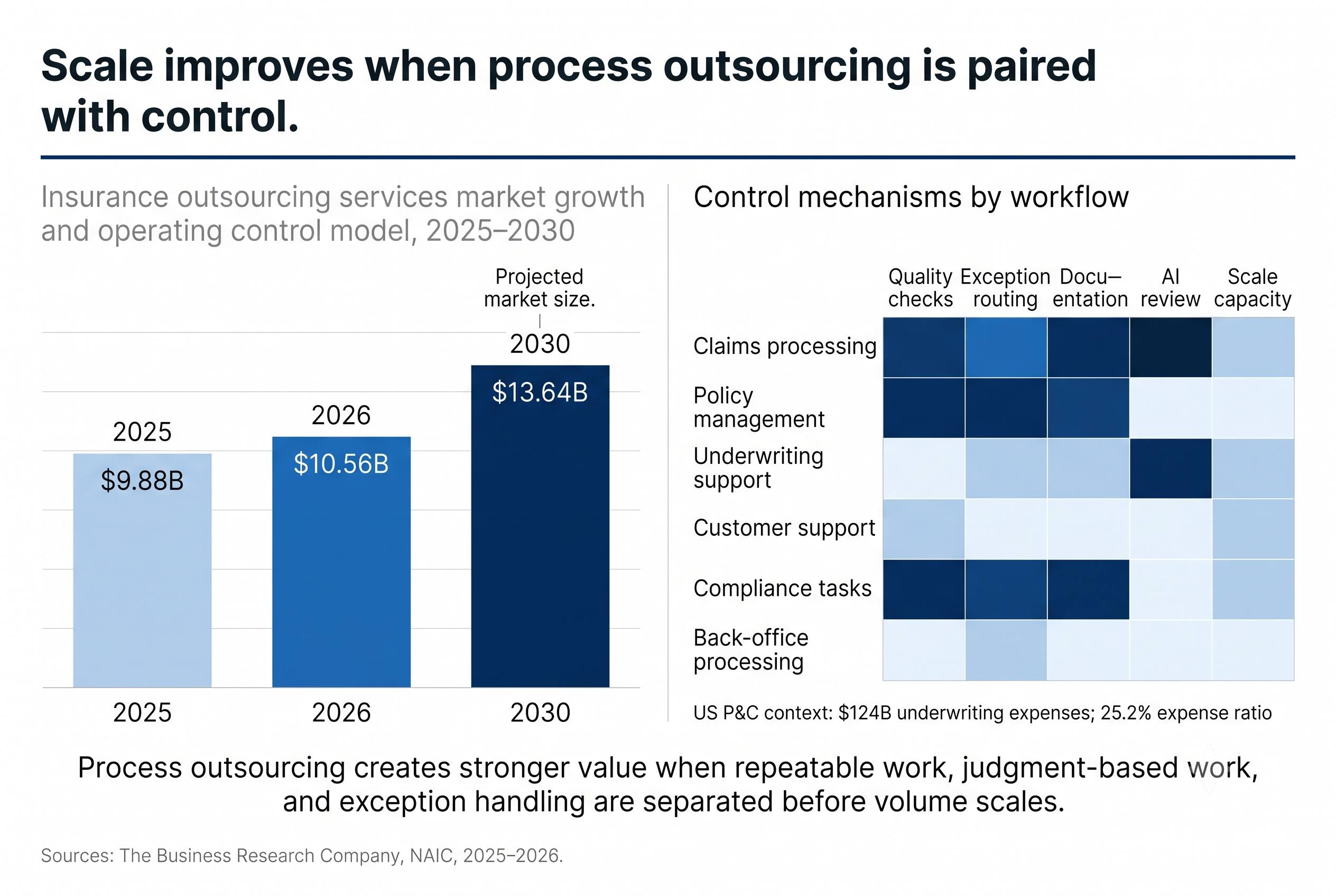

Insurance process outsourcing services are becoming a practical way for carriers to scale work without losing operating discipline. The demand is visible in the market data: the insurance outsourcing services market reached $9.88 billion in 2025 and is expected to grow to $10.56 billion in 2026, with growth tied to increasing policy volumes, operating cost pressure, digital insurance expansion, regulatory complexity, and specialized outsourcing providers. The same market is projected to reach $13.64 billion by 2030. For carriers, the value comes from more than added capacity. The strongest outsourcing models help standardize repeatable work, protect quality, and keep exceptions visible across the insurance lifecycle.

Scale Is Becoming a Process Question

Carrier scale depends on how well high-volume work is organized across claims, policy servicing, underwriting support, billing, customer support, document handling, and compliance. The NAIC’s 2025 mid-year property and casualty analysis reported $124 billion in underwriting expenses, a 25.2% expense ratio, and a 96.4 combined ratio for the US P&C industry during the first half of 2025. Those numbers show why operating structure matters even during periods of improved underwriting performance.

Insurance process outsourcing services create value when they help carriers separate repeatable work from judgment-based work. A billing update, document review, address change, claim status request, or endorsement may look routine at the task level, but each item can affect another function if the workflow is unclear. A controlled outsourcing model defines the data required, the systems involved, the quality checks, the exception path, and the escalation point before volume increases.

The Scope Now Reaches Across the Insurance Lifecycle

Insurance outsourcing has expanded across a wide range of operational functions. The Business Research Company defines insurance outsourcing services across claims processing, policy management, underwriting, finance and accounting, information technology, and other service types. Its 2026 report also lists subsegments such as claims adjudication, claims investigation, claims settlement support, policy issuance, policy renewal management, policy cancellation handling, endorsement processing, quote generation support, application screening, and underwriting decision support.

That scope fits how insurance work actually moves. A customer service inquiry may require policy data, billing records, claim status, producer notes, and compliance documentation. A claims support task may require document review, fraud signal detection, vendor coordination, payment information, and customer communication. ISSI’s insurance operations solutions are organized around that connected model, supporting claims, policy operations, customer experience, fraud, compliance, back-office work, and AI workflow control as parts of the same operating environment.

Policy Management Needs Clean Handoffs

Policy management is one of the clearest areas where process outsourcing can strengthen scale. The work includes issuance, renewals, cancellations, endorsements, proof-of-coverage requests, document updates, billing changes, and policyholder information updates. The outsourcing services market report identifies policy management as one of the core service categories, with specific subsegments that include policy issuance, renewal management, cancellation handling, endorsement processing, and policy information updates.

The operational value comes from handoff discipline. A policy change can touch billing, underwriting, declarations, producer communication, lienholder information, renewal records, and future claims eligibility. A well-run claims and policy operations model gives associates clear rules for what can be processed immediately, what requires review, and what needs documentation before the transaction moves forward. That reduces avoidable rework while giving carriers more consistent support during renewal cycles, product changes, and volume spikes.

Claims Support Depends on Documentation Quality

Claims support is another area where process outsourcing services can improve consistency across high-volume work. A strong claims support model helps manage intake, documentation, status updates, claim file organization, payment support, vendor coordination, and customer communication. The value is especially clear when carriers are managing catastrophe activity, increased repair complexity, fraud signals, or heavier communication volume.

J.D. Power’s 2025 U.S. Claims Digital Experience Study found that insurers deliver adequate proactive digital updates 22% of the time, and 22% of customers still rely on multiple channels to find answers to the same question. The same study found that 52% of auto and homeowners customers who rate their digital claims experience as poor or just OK are likely to leave or not renew, compared with 4% among customers who rate the experience excellent or perfect.

Those findings point to the importance of clean operating support. Customers want timely information, but claims teams also need accurate documentation, complete intake details, and clear status data. ISSI has covered this same operating pattern in FNOL Is the Only Part of Claims That Drives Cost but Belongs to No One, where early information quality influences the cost and clarity of later claims activity.

Compliance and Fraud Add More Need for Control

Compliance, quality, fraud review, and payment integrity are becoming more connected to everyday operations. The insurance outsourcing services market report includes regulatory compliance management, customer onboarding assistance, premium collection services, risk data analysis, billing support, multilingual customer service, legacy system modernization, and knowledge process services within the market’s revenue categories. That mix shows how outsourcing has moved into work that requires both process accuracy and control.

The fraud environment also reinforces the need for disciplined review processes. The National Insurance Crime Bureau reported that an analysis of questionable insurance claims submitted from 2022 through June 30, 2025 showed a year-over-year increase in claims involving traditional identity theft or synthetic identity, with nearly a quarter of identity-theft-related referrals involving a synthetically generated identity. For carriers, that makes document validation, referral quality, payment review, SIU support, and exception handling more important inside routine workflows.

Regulatory expectations are also becoming more operational, especially around AI. The NAIC’s implementation map for its model bulletin on the use of artificial intelligence systems by insurers lists multiple jurisdictions that have adopted the bulletin, including Delaware in 2025, Hawaii in 2025, and New Jersey in 2025, alongside earlier adopters. That matters because governance has to be executed through workflows, review notes, audit trails, escalation paths, and quality monitoring.

AI Makes Process Outsourcing More Valuable

AI is changing the kind of support carriers need from insurance process outsourcing services. KPMG’s 2025 Insurance CEO Outlook found that 73% of insurance CEOs are prioritizing AI investments to streamline underwriting, claims, and customer experience, while 77% identify workforce transformation and AI upskilling as a top constraint and opportunity. IBM’s 2025 insurance AI report found that insurers allocate 40% of AI spend to operational effectiveness and cost reduction, and 77% expect to use agentic AI in claims over the next year.

AI-supported workflows still need people who understand the insurance process around the output. Claim summaries need review. Document extraction needs validation. Customer responses need approved knowledge sources. Fraud flags need investigation paths. Policy changes need data checks and escalation rules. ISSI discussed this control issue in AI in Claims Is Working Exactly as Designed. That’s the Problem, and the same principle applies across underwriting support, policy servicing, customer care, compliance, and AI operations and workflow control.

What Carriers Should Expect From a Process Outsourcing Partner

A strong insurance process outsourcing partner should help carriers scale with visibility. The evaluation should include how the partner captures institutional knowledge, trains associates on insurance-specific workflows, documents exception rules, monitors quality, protects data, supports compliance requirements, and reports on rework. Activity volume still matters, but the better questions focus on accuracy, escalation, consistency, and total work reduction.

The scorecard should include first-pass accuracy, reopened cases, correction volume, exception aging, documentation quality, customer effort, downstream touches, and quality review findings. These measures show whether the outsourced workflow is improving the operating model or simply completing tasks. For functions such as back-office and financial operations, compliance, quality and risk, and fraud, SIU and payment integrity, the right scorecard gives carriers a clearer view of where process support is strengthening control across the business.

Closing Perspective

Insurance process outsourcing services help carriers scale when they are built around workflow discipline, insurance knowledge, and quality control. The opportunity is strongest in the work that repeats at volume but still requires accuracy: policy changes, claims documentation, customer support, billing updates, underwriting support, compliance tasks, fraud review, payment support, and back-office processing.

The direction of the market is clear. Insurance outsourcing is becoming more specialized, more connected to technology, and more integrated with the carrier operating model. For organizations reviewing where scale, consistency, and workflow control can improve, ISSI’s insurance operations solutions provide a practical way to evaluate process outsourcing across the full insurance lifecycle.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.