When Five Million Policyholders Leave, the Operational Problem Is Not What You Think

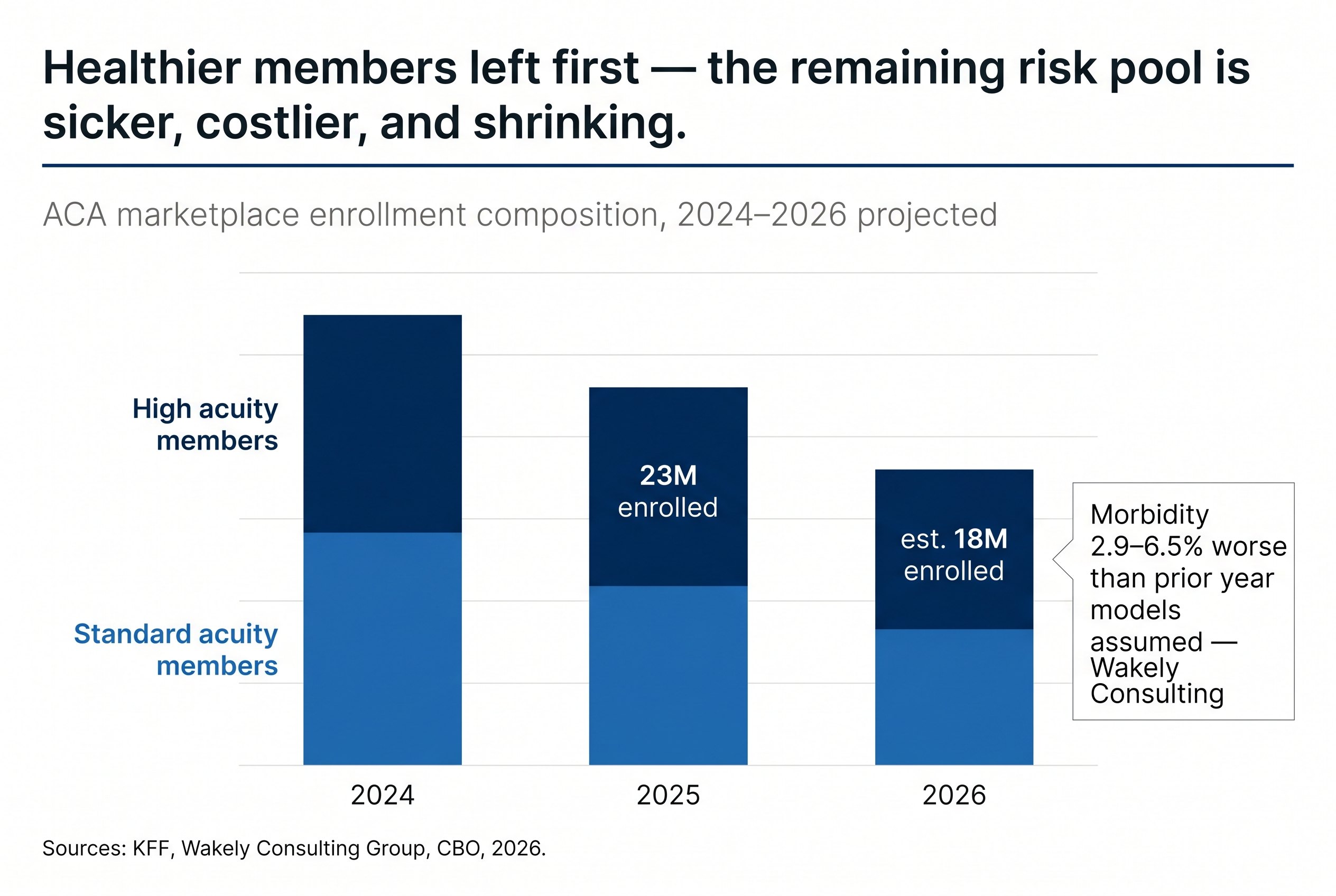

The headline numbers from the 2026 ACA marketplace tell a familiar story about affordability and political failure. Congress allowed enhanced subsidies to expire. Premiums surged, in some markets by more than 100 percent year over year. Enrollment dropped. The Congressional Budget Office estimated four million people would lose coverage. KFF now projects the final figure could approach five million, a decline exceeding 20 percent from 2025 levels.

That story is being told accurately. It is not, however, the story that should be occupying the attention of health insurance carrier leadership.

The enrollment number is a symptom. The operational consequences of who left, and who remained, are the problem that will define carrier performance through 2026 and into the planning cycles for 2027. Understanding those consequences requires looking past the headline and into the risk pool mechanics that every actuarial team has already modeled but that operational leadership has not yet fully absorbed.

The Risk Pool Problem Is Now an Operations Problem

When premium costs rise sharply, the insurance market does not lose members randomly. It loses them in a pattern that actuaries have documented across every previous market disruption.

Healthy enrollees, those with lower expected claims costs and less urgent dependence on continuous coverage, exit first. They make rational economic decisions: at $1,900 per month in premiums, a 28-year-old with no chronic conditions has genuine optionality. They can go uninsured, join a cost-sharing arrangement, or absorb the risk. The 55-year-old managing hypertension and a recent cardiac event does not have that optionality. They stay.

The 2026 data is confirming this pattern precisely. Silver plan enrollment fell 17 percent in 2026 compared to 2025, while bronze plan enrollment expanded by nearly 11 percent, as remaining enrollees bought down to higher-deductible plans rather than exit entirely. Wakely Consulting Group estimates that morbidity in the remaining risk pool could be between 2.9 and 6.5 percent worse than prior year models assumed. Independent research from the Commonwealth Fund found that remaining enrollees will be sicker on average, driving up average claims costs and, with them, rates for the following year.

The mechanism is self-reinforcing. A sicker pool generates higher claims. Higher claims require higher premiums. Higher premiums push out the next tranche of healthier members. Rates rise again for 2027. The carriers that understand this are already building operational responses. The carriers that have treated the enrollment decline as a volume problem, rather than a composition problem, will encounter the consequences in their loss ratios before they encounter them in their planning documents.

What a Sicker, Smaller Pool Demands Operationally

The operational implications of risk pool deterioration are specific and they are compounding.

Claims volume does not fall proportionally when enrollment falls. A 20 percent reduction in membership does not produce a 20 percent reduction in claims activity. It may produce a 5 to 10 percent reduction, at best, if the departing members were disproportionately healthy. Against a fixed or only modestly reduced cost base, the per-member cost of processing, adjudicating, and servicing claims rises. Administrative expenses, including customer service, claims processing, and premium billing, already represent a meaningful share of the operating cost structure that the Medical Loss Ratio requirement does not relieve. Those costs do not compress automatically when membership falls.

The complexity of individual claims rises alongside acuity. Higher-acuity members generate more claims per member, more prior authorization requests, more appeals, more coordination of benefits complexity, and more interactions with customer service. A claims operation calibrated for the enrollment mix of 2024 or 2025 is not calibrated for the enrollment mix of 2026. The ratio of complex cases to total cases has shifted, and it shifted quickly.

Premium non-payment has added a further operational layer that was not present at this scale in prior years. According to Wakely Consulting Group, approximately 14 percent of people who enrolled in ACA plans in 2026 did not pay their first monthly premium bill, with the figure reaching 25 percent or higher in some states. The normal early-year attrition rate is in the mid-single digits. Managing that volume of non-payment, including the outreach, grace period administration, and disenrollment processing that follows, has placed demands on member services and billing operations that were not planned for in 2025 budgets.

Elevance, one of the largest ACA market participants, entered 2026 with membership up approximately 10 percent from open enrollment but expects to end the year with a roughly 30 percent membership decline, according to JP Morgan analysis. The gap between enrolled and retained membership at that scale represents an operational management challenge that sits entirely within member services, billing, and disenrollment workflows. It does not resolve itself.

The Premium-Billing-Disenrollment Cycle Requires Operational Precision

The premium non-payment dynamic deserves more focused attention than it is receiving in carrier boardrooms, because the consequences of handling it poorly extend beyond the immediate revenue loss.

Federal and state grace period rules govern how long a carrier must maintain coverage for a member who stops paying premiums, what communications are required during that period, and how the disenrollment process must be documented. These rules differ by state and by the subsidy status of the member. Managing tens of thousands of members simultaneously through grace period timelines, with state-specific compliance requirements and the member communication obligations that accompany them, is not a background administrative task. It is a high-volume, deadline-driven, compliance-sensitive workflow.

Carriers that handle this process well protect themselves from two distinct exposures. The first is the regulatory exposure that comes from improper grace period administration, which in a market where regulators are already paying close attention to insurer practices, carries material risk. The second is the retention opportunity that a well-managed grace period process can create. Members who stopped paying due to sticker shock, rather than inability to pay, are not permanently lost. A structured outreach process, executed during the grace period, recovers a meaningful fraction of them. Most carriers do not have the operational capacity to execute that outreach at scale while simultaneously managing normal claims and service volumes.

In our experience working with carriers navigating member attrition events, the difference between a carrier that recovers 8 to 12 percent of lapsing members through grace period outreach and one that recovers 2 to 3 percent is almost entirely an operational capacity question. The strategy is not complex. The execution requires bandwidth that most organizations did not plan for.

The Forward Problem: 2027 Rate Development Under Uncertainty

The operational decisions carriers make in the second and third quarters of 2026 will directly shape the actuarial assumptions that underpin 2027 rate filings.

Wakely has already flagged that the morbidity deterioration in the 2026 risk pool introduces "considerable uncertainty for issuers as they develop 2027 premium rates." Carriers that have clean, operationally sound data on their 2026 claims experience, including accurate diagnosis coding, complete prior authorization records, and well-documented high-cost case management, will build 2027 rate assumptions from a stronger foundation than those whose operational data is fragmented or incomplete.

The upcoding risk compounds this. Research on high-acuity claims environments has documented a consistent pattern: as coding intensity increases across care settings, driven partly by AI-powered documentation tools and revenue cycle optimization strategies among providers, health plans face growing misalignment between clinical evidence, documentation, and billed complexity. For carriers whose utilization management and claims review operations are not calibrated for this environment, the 2026 claims data will systematically overstate expected future costs, producing premium proposals that either price carriers out of the market or create regulatory friction during the rate approval process.

Getting the operational data right in 2026 is not an internal administration matter. It is the input that determines whether 2027 rate filings are defensible, competitive, and accurate.

The Strategic Posture That Protects Margin in a Shrinking Market

The carriers that will emerge from this enrollment disruption with sustainable margins share a common operational orientation. They are not managing the 2026 situation as an exceptional year to be endured. They are treating the structural shift in their membership as a permanent recalibration that requires a permanent operational response.

In practical terms, this means building claims and member services capacity that is explicitly calibrated to a higher-acuity, lower-volume membership. It means having dedicated operational capacity for the grace period and disenrollment cycle, separate from the standard claims workflow, so that one does not deplete bandwidth from the other. It means investing in utilization management operations that can handle a higher ratio of complex, prior-authorization-intensive cases without the cycle time degradation that erodes both member experience and cost control. And it means building the documentation discipline into daily operations now, so that 2026 experience data arrives at the actuarial team in a form that can actually support sound rate development.

The enrollment decline created a set of operational demands that were not in any carrier's 2025 planning model. The carriers that treat those demands as temporary exceptions will build their 2027 rate structures on incomplete evidence and underpowered operations. The carriers that treat them as the new operating baseline will have both the margin performance and the actuarial foundation that the next enrollment cycle requires.

The five million who left changed the market. The operational question is whether the response is calibrated to the market that remains.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.