Social Inflation Is Not a Legal Problem. It Is a Claims Operations Problem.

The insurance industry's response to social inflation has been largely consistent across carriers: raise reserves, increase premiums, tighten reinsurance terms, and engage better defense counsel. These are rational responses to a threat that is primarily understood as a legal and financial one.

They are also insufficient responses, because social inflation is not primarily a legal problem. It is an operations problem that manifests in court.

The distinction is not semantic. If the root of the problem is legal, the solution lives in the defense strategy. If the root of the problem is operational, the solution must live in how claims are handled from the first moment of contact, long before any attorney is engaged and long before any jury is seated. The industry has invested heavily in the former. It has significantly underinvested in the latter.

Understanding why requires a clear-eyed look at what social inflation actually is, where it actually starts, and what operational decisions determine whether a given claim becomes a $200,000 settlement or a $50 million verdict.

The Scale of the Problem Is No Longer Marginal

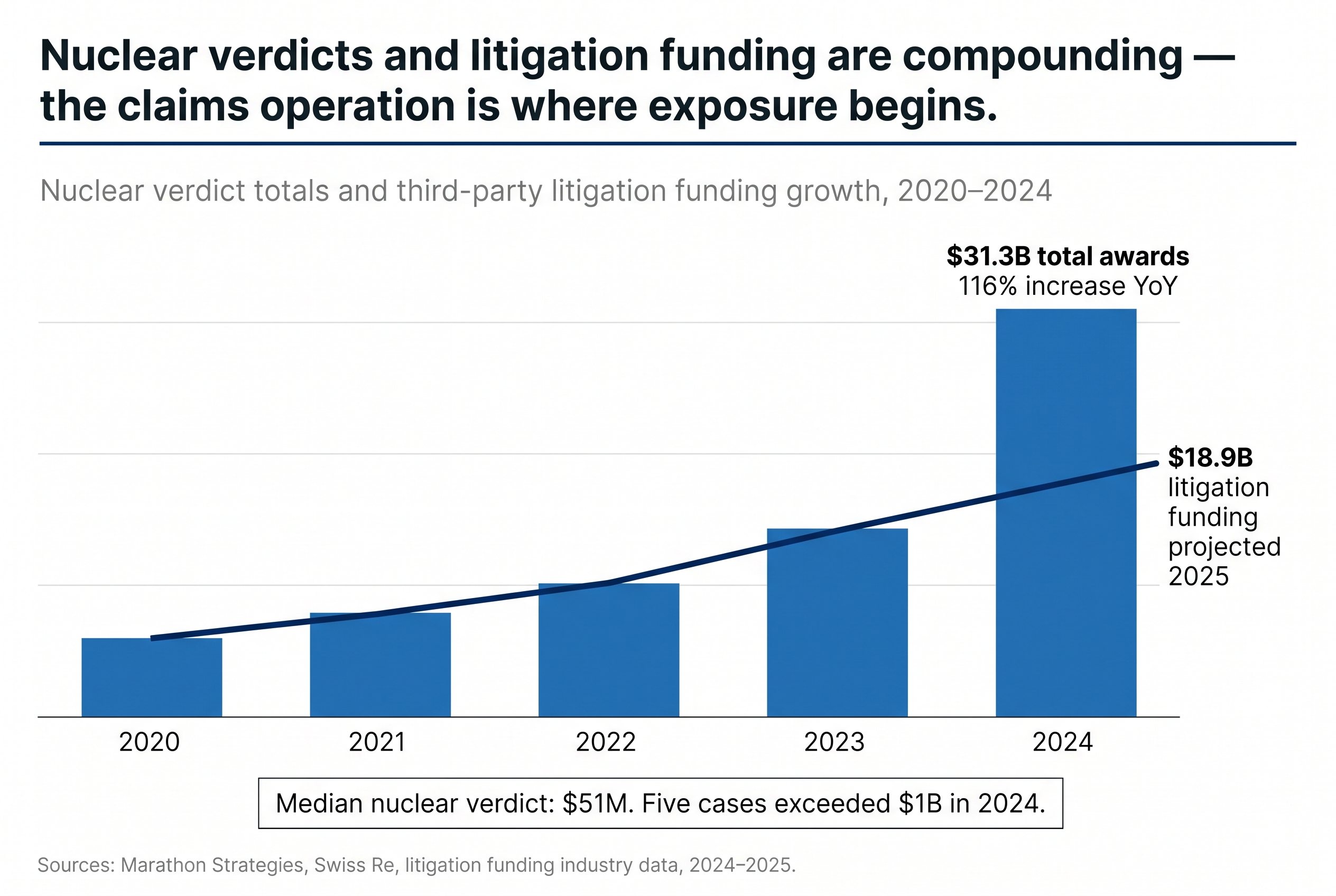

Social inflation has moved from an industry concern to a structural market force. In 2024, there were 135 lawsuits resulting in nuclear verdicts against corporate defendants, a 52 percent increase over 2023. The total sum of those verdicts was $31.3 billion, representing a 116 percent increase from the prior year. The median nuclear verdict climbed to $51 million, and verdicts exceeding $100 million surged by more than 80 percent, with five individual cases crossing the $1 billion threshold.

Third-party litigation funding is accelerating the problem in ways that change the fundamental economics of claim resolution. U.S. litigation funding investments are projected to reach $18.9 billion in 2025 and exceed $67 billion annually by 2037. When outside investors finance a plaintiff's lawsuit in exchange for a share of the recovery, the economic incentive structure shifts in a specific and important way. Plaintiffs no longer bear the financial pressure that historically pushed cases toward early, reasonable settlement. The funder's return is optimized by maximum award, not by efficient resolution. What was once a bilateral negotiation between insurer and claimant now involves a third-party investor whose financial interest is structurally opposed to early settlement.

The Litigation Transparency Act of 2025 and several state-level disclosure requirements signal that legislators are beginning to recognize this dynamic. But legislative remedies move slowly. The claims environment that carriers are operating in today, and will operate in through at least 2027, is one where the financial incentives on the plaintiff's side favor escalation over resolution.

Against that backdrop, the operational decisions that happen in the first 24 to 72 hours of a claim's life have outsized consequences.

Where the Verdict Is Actually Determined

The legal community understands something that insurance operations leadership often does not: by the time a case reaches a jury, the outcome has largely been shaped by decisions made months or years earlier in the claims handling process.

The conditions that produce a nuclear verdict are rarely manufactured in the courtroom. They are discovered there. Plaintiff attorneys do not create documentation gaps, inconsistent adjuster notes, missed escalation triggers, or evidence of delayed response. They find them. And when a skilled plaintiff attorney applies the reptile theory, a courtroom technique that frames a corporation's conduct as a systemic threat to public safety, to a claims file that contains those gaps, the jury is not being manipulated into an unreasonable verdict. The jury is being shown evidence of operational failure and asked to respond to it.

The implication is direct. A claim that is handled with precision at intake, documented with consistency through adjudication, and escalated appropriately when complexity emerges is a claim that is fundamentally harder to litigate against. Not because the legal exposure disappears, but because the evidentiary foundation for a reptile theory argument does not exist. There is no documentation gap to find. There is no delayed response to highlight. There is no inconsistency between what the adjuster noted and what the company's internal policies required.

This is not a theoretical observation. In our work supporting carrier claims operations across commercial liability, auto, and general liability lines, the pattern is consistent. The claims that escalate to significant litigation exposure are rarely the claims where liability was genuinely ambiguous. They are the claims where the handling quality gave plaintiff counsel something to work with.

The Four Operational Failure Points That Create Litigation Exposure

Understanding where operations create nuclear verdict conditions requires specificity about the failure modes. There are four that appear most consistently.

FNOL documentation discipline. The first notice of loss is the evidentiary foundation of the entire claim. When FNOL capture is incomplete, when adjuster notes are vague, when the initial incident description lacks specificity about parties, conditions, and timeline, every subsequent decision in the claims file is built on a weak foundation. A case that reaches litigation with strong, detailed FNOL documentation is a fundamentally different case to defend than one with fragmented initial intake. The carriers that treat FNOL as an administrative step rather than a strategic one are building litigation exposure from the first moment.

Escalation trigger failure. Every carrier has escalation protocols. The operational question is whether those protocols are executed consistently at transaction volume or whether they exist on paper while high-complexity cases continue through standard processing paths because the adjuster was managing 90 other files. When a claim with characteristics that historically correlate with elevated litigation risk, serious bodily injury, multiple parties, jurisdictions with high verdict history, commercial defendants with significant assets, moves through standard processing without triggering the review that its profile warrants, the case arrives at litigation without the early intervention strategy that would have changed its trajectory.

Inconsistency between internal policy and documented practice. Plaintiff attorneys will request the carrier's claims handling guidelines in discovery. When those guidelines specify response timeframes, documentation requirements, and escalation thresholds that are not reflected in the actual claims file, the gap becomes evidence in itself. The argument to the jury is not merely that the claimant was harmed. It is that the carrier's own standards required different conduct and the carrier chose not to follow them. That argument is significantly more persuasive when the claims file makes it easy to construct.

Reserve inadequacy as a settlement posture problem. When reserves are set too low at initial evaluation, the authorized settlement authority is anchored at a level that does not reflect the actual exposure. Adjusters operating within those constraints negotiate from a position that the other side, particularly when funded by a third-party litigation investor, has no incentive to accept. The case ages. Discovery deepens. The plaintiff's theory strengthens. When the reserve is finally corrected, it is often because the case has already moved into a posture where settlement costs more than it would have eighteen months earlier.

What Operationally Sophisticated Carriers Are Doing Differently

The carriers that are managing social inflation exposure effectively have recognized that the legal strategy and the operational strategy must be built in sequence, not in parallel, and that operations must come first.

This means treating FNOL as a strategic function rather than a call center function. The information captured at first intake, the specificity of incident description, the completeness of party and witness identification, the documentation of conditions, determines what the adjuster has to work with, what defense counsel has to work with, and what the evidentiary record looks like if the case reaches a jury. Organizations that staff and train for FNOL as a documentation-critical function produce claims files that are materially more defensible than those that staff for call handling volume.

It means building escalation triggers into workflow design, not just into policy documents. An escalation protocol that requires an adjuster to manually identify and flag a high-complexity case is dependent on adjuster judgment and bandwidth. An escalation protocol embedded in workflow design, where specific intake characteristics automatically route a claim to enhanced review, is consistent regardless of adjuster workload. Consistency is what produces defensible claims files at scale.

It means investing in reserve accuracy at first evaluation. The actuarial case for this is well established. The operational case is equally clear. A claim reserved accurately at the outset settles within an authorized range that reflects the real exposure. A claim reserved conservatively for ease of closure becomes a settlement problem when the true exposure becomes visible at the cost of months of additional litigation.

And it means treating the claims file as a legal document from the first entry, not from the date that litigation is threatened. Every note, every communication, every decision record is a potential exhibit. The carriers that build documentation discipline into daily adjuster practice, not into a pre-litigation response procedure, are building a fundamentally different evidentiary posture than those that treat documentation as a retroactive task.

The Forward Equation

Third-party litigation funding is not retreating. The legislative response is moving, but slowly, and disclosure requirements do not change the economic incentives of funders already committed to existing cases. The jury pool dynamics that produce nuclear verdicts, institutional distrust, anti-corporate sentiment, the influence of plaintiff attorney marketing, are not improving on any measurable trajectory. A 2025 Edelman survey found that seven out of ten Americans believe that government officials, business leaders, and journalists deliberately mislead them. That is the jury pool that carriers' cases are being tried in front of.

The legal environment will remain hostile for the foreseeable future. That is a fixed condition, not a variable. The variable is the quality of the operational foundation on which each claim is built.

Carriers that continue to treat social inflation as a problem to be managed at the defense table will keep encountering it at the defense table. The carriers that understand it as an operations problem will begin managing its trajectory at FNOL, in the escalation protocol, in the reserve methodology, and in the documentation practice of every adjuster handling every file.

The verdict is not written in the courtroom. It is written in the claims operation, over months of handling decisions that plaintiff counsel will reconstruct in front of a jury. The question for claims leadership is whether the operational foundation being built today would survive that reconstruction.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.