The Compliance Maintenance Burden Is Growing Faster Than Compliance Teams Can Scale. Most Carriers Are Managing the Gap With Exposure.

There is a version of the compliance problem in insurance that most carrier leadership teams understand well: the one-time implementation challenge. A new regulation takes effect. The legal team interprets the requirements. The operations team adjusts the relevant workflows. The compliance team documents the changes, trains the staff, and files what needs to be filed. The problem is solved.

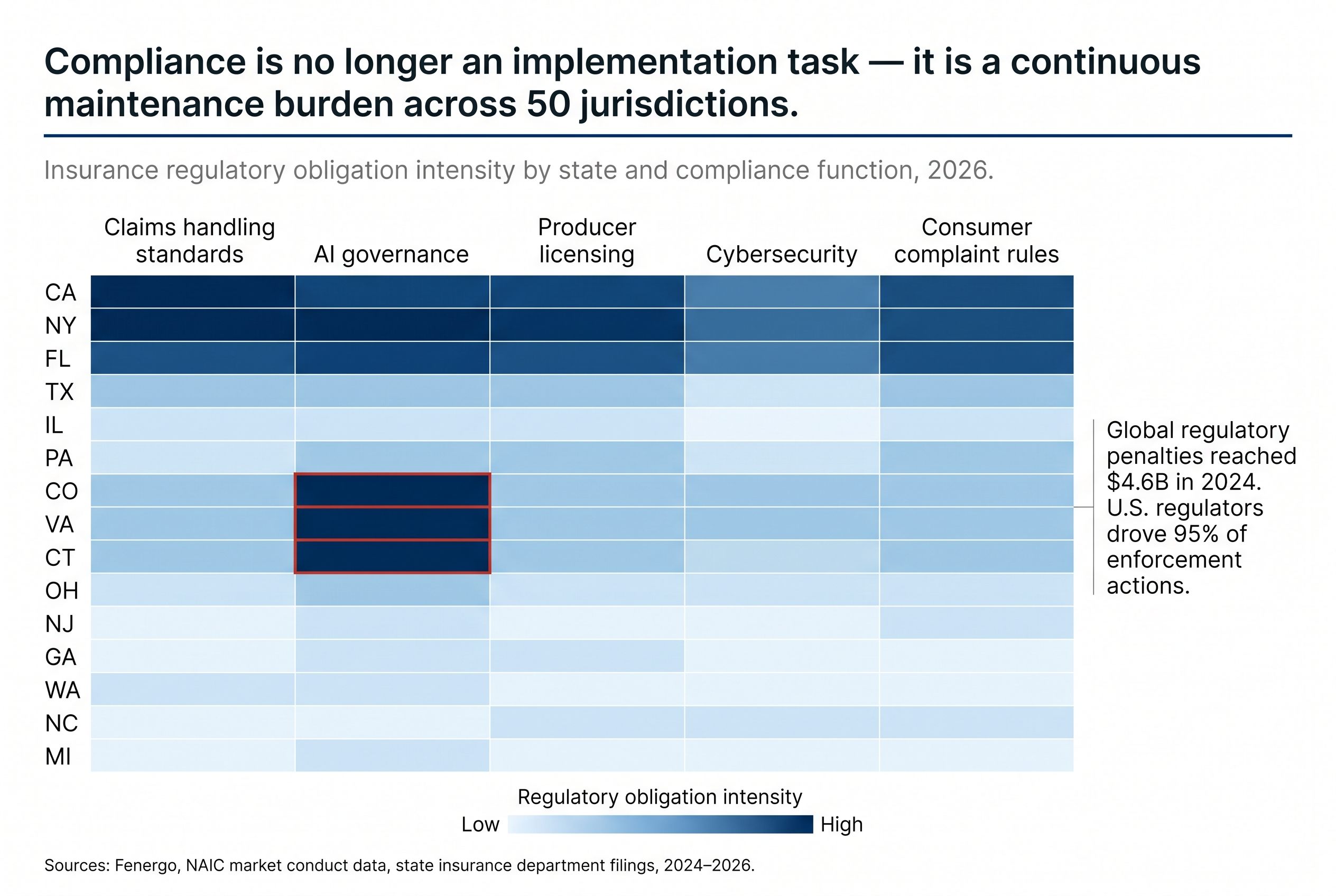

That model of compliance as a series of discrete implementation events is no longer adequate. It may not have been adequate for several years. The U.S. insurance regulatory environment in 2026 is not a stable landscape requiring periodic updates. It is a continuously changing body of requirements across 50 state jurisdictions, each with its own timing, interpretation, and enforcement posture, that demands ongoing operational maintenance rather than periodic project management.

The distinction matters because these two modes of compliance require fundamentally different organizational capabilities, and most carriers are still structured for the first while operating in the second.

The Architecture of the Compliance Maintenance Problem

Understanding why compliance has become a maintenance problem rather than an implementation problem requires a clear picture of what is actually changing and at what velocity.

State insurance regulation is not a fixed framework. States amend their insurance codes, issue bulletins and circulars, update market conduct examination priorities, revise producer licensing requirements, and introduce new consumer protection mandates on a continuous basis. The collective output of 50 state regulatory bodies, coordinating loosely through the NAIC while retaining full authority to deviate from model regulations in their implementation, produces a regulatory environment in which the compliance posture a carrier established last year is, in material respects, no longer the compliance posture the carrier needs today.

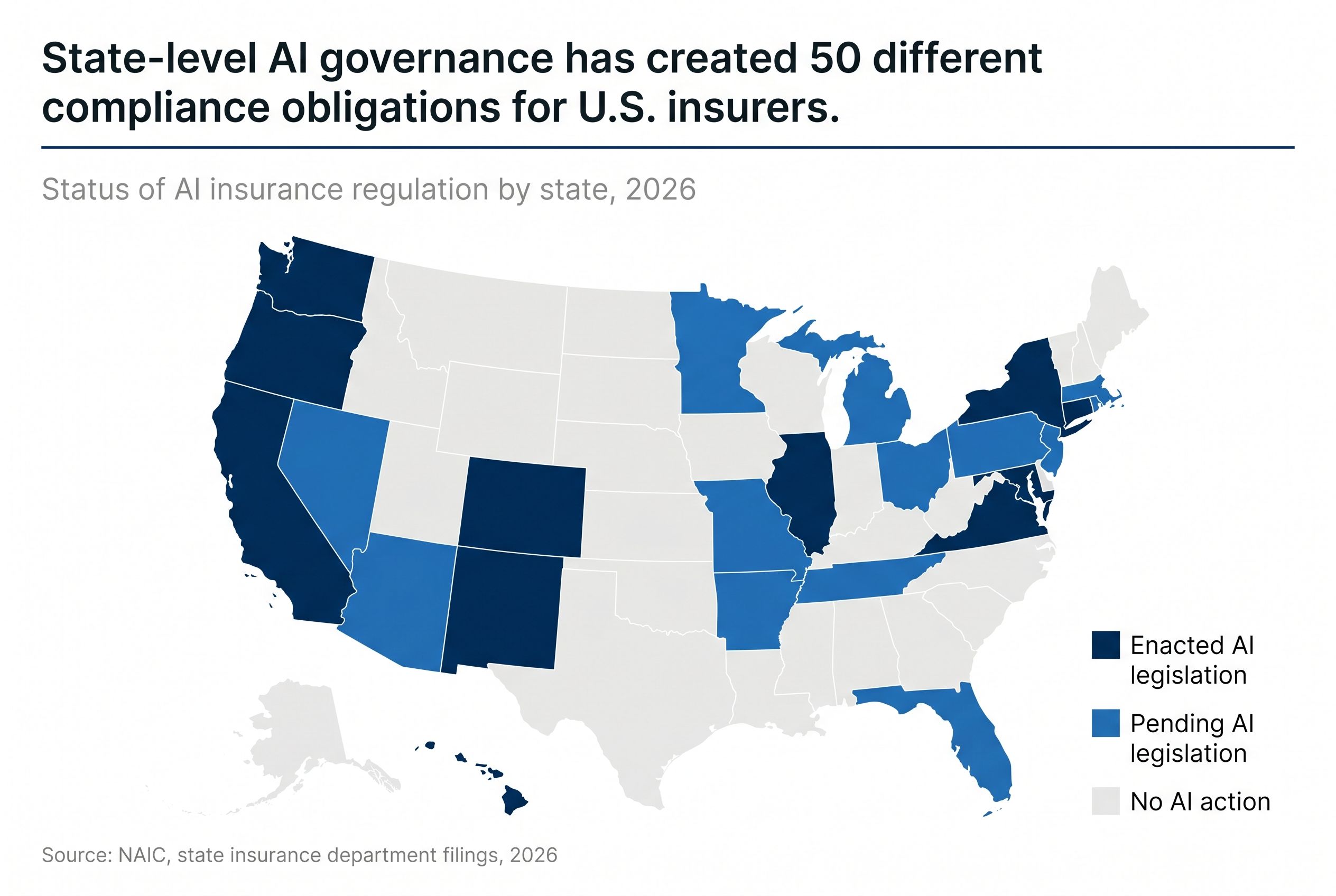

Several accelerants have intensified this dynamic in 2025 and 2026. The state-level AI governance legislation discussed in the first post in this series, Colorado's AI Act, Virginia's HB 2094, Connecticut's prior authorization restrictions, represents a new category of compliance requirement arriving faster than the operational systems to support it are being built. The NAIC's reinforced attention to market conduct in AI governance, cybersecurity, and consumer data management is reshaping examination priorities in ways that carriers who planned their compliance programs against prior examination patterns are discovering during actual examinations, not in advance of them.

Global regulatory penalties in the financial services sector reached $4.6 billion in 2024, with U.S. regulators accounting for 95 percent of enforcement actions. State insurance departments collectively took more than 2,500 formal actions against companies in a single recent reporting year, including suspensions and revocations of certificates of authority, based on NAIC data. These are not abstract risks. They are the operational consequence of compliance programs that were designed for a regulatory environment that has since changed.

The compliance maintenance burden is not evenly distributed across carrier operations. It concentrates in specific functions where regulatory requirements change most frequently and where the consequences of non-compliance are most material. Claims handling standards, documentation requirements, and response timeframe obligations vary by state and change as states update their market conduct guidance. Producer licensing, appointment, and continuing education requirements span all 50 states and generate continuous administrative obligations. Consumer complaint handling processes carry state-specific procedural requirements with penalty exposures for handling failures. And the emerging AI governance requirements are creating a new compliance maintenance layer on top of all of the above, requiring carriers to document, test, and demonstrate oversight of AI systems in ways that no prior compliance framework specified.

The Gap Between Compliance Knowledge and Compliance Execution

The central failure mode in insurance compliance is not, in most carriers, a knowledge failure. Legal and compliance teams generally know what is required. The failure is execution at scale: the consistent application of current requirements across every relevant transaction, interaction, and documentation decision made daily across the organization.

That gap between knowing the requirement and consistently executing it in operations is where regulatory exposure accumulates.

Consider what consistent compliance execution actually requires in a multi-state claims operation. Claims handling standards in California are not the same as in New York, which are not the same as in Florida. The timeframe within which an adjuster must acknowledge a claim, respond to a claimant inquiry, make a coverage determination, and issue payment or denial varies by state. The documentation that must accompany each step varies by state. The language required in specific communications to policyholders varies by state. When a claims operation processes thousands of claims per month across dozens of states, the organizational challenge is not knowing these requirements. It is ensuring that every adjuster handling every claim in every state applies the current requirement for that state to that transaction, consistently, without exception.

That challenge scales with geographic breadth. A carrier operating in 15 states has a compliance execution challenge that is not simply 15 times the challenge of a carrier operating in one state. It is dimensionally more complex, because the requirements interact, the update cycles are asynchronous, and the examination priorities of different states overlap in ways that require the compliance maintenance program to operate across all of them simultaneously.

The carriers that manage this well have made a structural decision about compliance that most have not: they treat compliance execution as an operational function requiring dedicated, continuously maintained capacity, not as a legal function requiring periodic project management. The compliance team defines the requirements. The operations function executes them. The division of responsibility sounds obvious. The operational implication, that execution quality at transaction volume requires dedicated compliance-aware operational capacity, not just well-trained general operations staff, is less commonly acted upon.

The Cost of Event-Based Compliance in a Continuous Environment

The dominant compliance posture in the industry remains what one 2026 compliance guide described precisely as event-based compliance: preparing intensively for an upcoming examination, then relaxing once it passes. That posture was manageable when examinations were the primary mechanism through which compliance gaps became visible. It is increasingly inadequate because examinations are no longer the primary mechanism.

Consumer complaint data is now a leading indicator that state departments of insurance use to direct examination attention and trigger targeted inquiries. A surge in complaints from a specific state about a specific carrier's claims handling practices will precede a formal examination notification. The carrier that operates in continuous-readiness mode, whose documentation is current, whose workflows reflect current state requirements, and whose complaint handling processes are functioning correctly, receives that examination inquiry from a fundamentally different posture than the one that treats examination preparation as a project activated only when a notification arrives.

The documentation dimension of this dynamic deserves specific attention. Regulators expect centralized, timestamped evidence during examinations. When evidence is scattered across spreadsheets, shared drives, and email chains, assembling a defensible audit trail becomes operationally difficult and gaps become visible to examiners precisely when visibility creates the most risk. The carrier whose daily operational workflow produces documentation that is examination-ready as a byproduct of how the work is done is not merely better prepared for examinations. It is managing its regulatory relationships from a position of transparency rather than from a position of reconstruction under scrutiny.

Market conduct examinations evaluate claims handling, underwriting practices, marketing and sales conduct, and consumer complaint processes. These are not distinct from the carrier's daily operations. They are a direct assessment of how the carrier's daily operations perform against regulatory standards. The examination outcome is determined by the quality of those operations on ordinary days, not by the quality of the examination response team's work in the weeks following notification.

Why Compliance Maintenance Cannot Be Solved by Compliance Teams Alone

The compliance function in most carrier organizations is appropriately sized for regulatory interpretation and program governance. It is not sized for the execution volume that compliance maintenance at a multi-state operation requires.

This is the structural problem that most compliance leaders encounter and that most carrier organizations have not fully resolved. The compliance team can define what the current requirements are in each state for each relevant function. It cannot also handle the claims documentation for 50,000 claims per month, execute producer appointment and licensing maintenance across 50 states, manage consumer complaint responses against state-specific procedural requirements, and maintain the AI governance documentation now required in multiple jurisdictions.

The functions that generate compliance exposure are operations functions. The compliance team's role is to define the standard to which those operations functions must perform. The critical organizational question is whether the operations functions have the capacity, the training, and the domain knowledge to perform to that standard consistently, and whether the compliance function has the visibility into operational performance to identify and correct gaps before they become examination findings.

The carriers that have closed this gap most effectively have made two structural decisions. The first is to staff compliance-sensitive operational functions, claims handling, complaint management, producer services, policy documentation, with associates who carry genuine insurance domain knowledge rather than generic process execution capability. The second is to build monitoring and feedback mechanisms that give the compliance function ongoing visibility into operational execution quality, rather than the periodic snapshot that an annual audit provides.

Seventy percent of insurers plan to increase compliance investment in 2026, according to industry research. The productive question for that investment is not simply how to add compliance team capacity. It is how to ensure that the operational functions where compliance exposure is generated have the execution quality and the domain knowledge that compliance investment is intended to support.

The Strategic Advantage in Continuous Readiness

The carriers that treat compliance as a continuous operational discipline rather than an event-driven project management function accumulate a competitive advantage that is not widely recognized as such.

Continuous compliance readiness means that examination outcomes are not disruptive events requiring recovery. They are confirmations of the operational posture the carrier has maintained throughout the year. It means that regulatory relationships are managed from a position of transparency, which produces materially different regulator engagement than the defensiveness that accompanies examination preparation under pressure. It means that the compliance investment the carrier makes produces durable operational quality rather than cyclical preparation-and-relaxation that leaves persistent gaps between preparation events.

The regulatory environment in 2026 is not simplifying. State-level AI governance requirements are being added to the existing body of market conduct, licensing, claims handling, and consumer protection obligations. The NAIC's examination tools are becoming more sophisticated. State departments are using complaint data more systematically to direct examination attention. The carriers that respond to this environment by adding compliance team headcount without addressing the operational execution quality that generates compliance performance are solving the wrong part of the problem.

The compliance maintenance burden is growing because the regulatory environment is growing in complexity at a pace that discrete implementation projects cannot track. The carriers that recognize this, and that build the operational infrastructure required for continuous compliance execution rather than periodic compliance preparation, are building a structural advantage that compounds in value precisely as the environment they are operating in becomes more demanding.

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.