The AI Regulation Collision Nobody Warned Insurers About

For the past several years, insurance executives have watched the AI regulation debate unfold largely as a federal question. Would Congress act? Would the administration set a national standard? The assumption, stated or not, was that clarity would eventually come from Washington and the industry would adapt accordingly.

That assumption is now operationally dangerous.

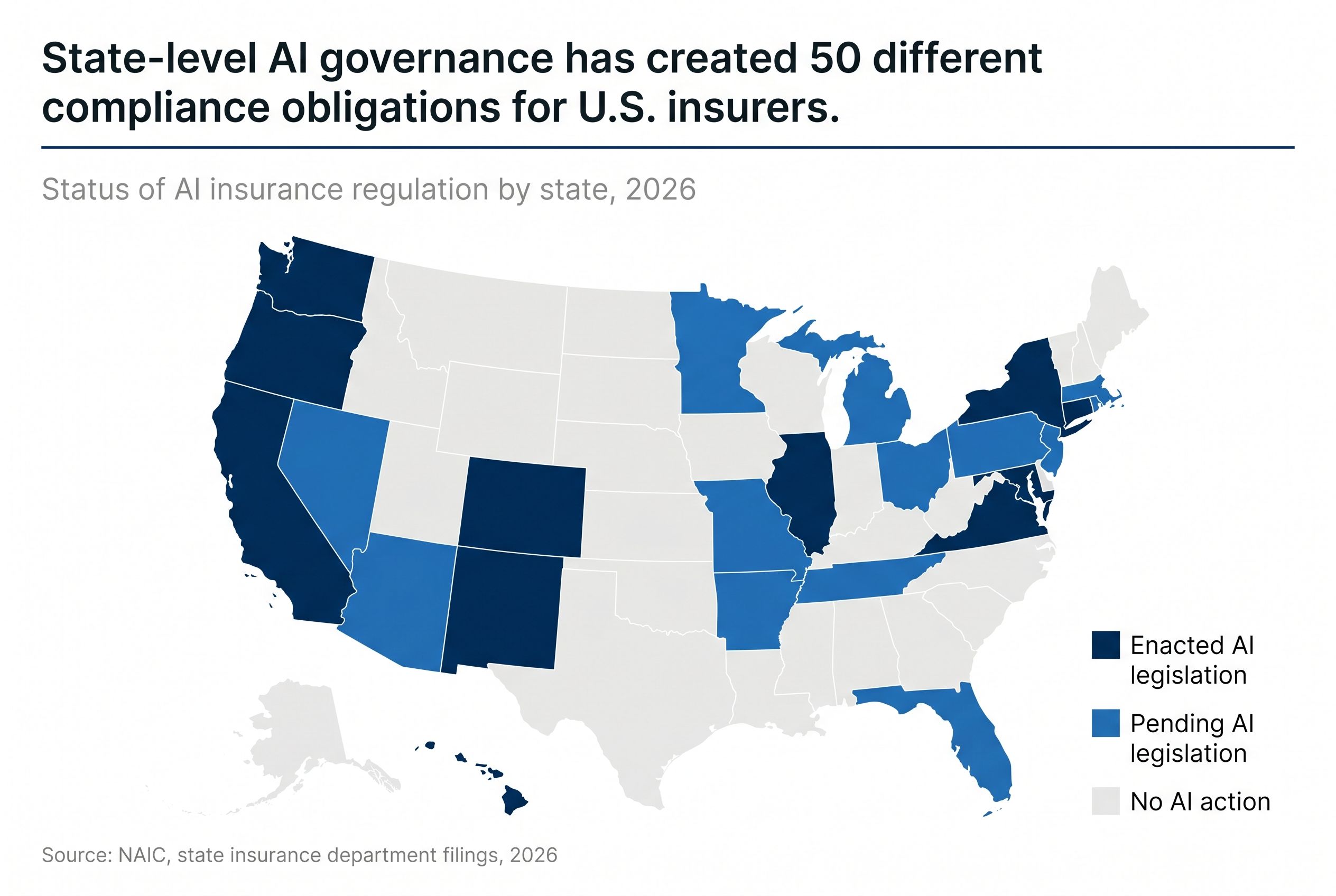

What has materialized instead is a fragmented, accelerating body of state-level law that imposes specific, binding obligations on carriers using AI in underwriting, claims adjudication, and customer interactions. The obligations differ by state. The enforcement mechanisms differ by state. And the timeline for compliance is not a future consideration. For many carriers, it is already past.

The C-suite conversation about AI governance needs to shift from strategic to operational, and it needs to shift now.

What the Regulatory Landscape Actually Looks Like in 2026

The clearest way to understand the current environment is to stop thinking about AI regulation as pending and start treating it as active.

Colorado's AI Act, the most comprehensive state-level AI governance law in the country, targets any organization deploying AI systems that make consequential decisions in insurance, healthcare, housing, or employment. It requires documented risk management programs, algorithmic bias mitigation, and consumer disclosures. Implementation, originally set for February 2026, was pushed to June 2026 following industry pushback. That extension is not an invitation to wait.

Virginia has enacted legislation closely mirroring Colorado's framework. Connecticut has moved to restrict insurers from using AI to automatically deny healthcare claims, a direct response to documented patterns of algorithmic denial without human review. New York's Department of Financial Services has issued AI underwriting and pricing guidance that applies to all licensed insurers in the state.

In March 2026, the National Association of Insurance Commissioners published a formal Issue Brief opposing federal preemption of state AI oversight. The NAIC's position is unambiguous: state regulators have built meaningful supervisory infrastructure, including AI-specific principles, interpretive guidance, and examination tools, and they intend to preserve it. Congressional proposals to restrict state-level AI oversight have not eliminated state authority. They have intensified the NAIC's determination to defend it.

The net effect is a regulatory environment in which carriers deploying AI face materially different compliance obligations depending on the states in which they operate, with no indication that a federal standard will resolve the inconsistency in the near term.

The Operational Gap Most Carriers Have Not Closed

Understanding the regulatory landscape is necessary. It is not sufficient. The more consequential question for insurance leadership is whether current operational structures are capable of meeting obligations that are state-specific, dynamic, and enforcement-backed.

Most carriers have invested in AI capability. Fewer have invested with equivalent seriousness in the operational infrastructure that makes AI deployable within a compliance framework. The distinction matters because regulators are not evaluating AI technology in isolation. They are evaluating governance. They are asking who owns the decision when the model produces an output, who reviews the exception cases, how bias testing is documented, and what the escalation path looks like when an automated determination is challenged.

These are not questions that technology answers. They are questions that operational design answers.

The carriers most exposed are not necessarily those with the most aggressive AI deployments. They are those whose AI capabilities have outpaced their control architecture. In practice, this means organizations where AI systems are producing decisions or recommendations at volume without a defined human-in-the-loop layer, without state-specific rule sets governing what the system can and cannot determine autonomously, and without documentation practices that would survive regulatory examination.

In our work alongside carriers across multiple lines of business, the pattern is consistent. The investment conversation focuses on what AI can automate. The governance conversation, when it happens at all, focuses on data privacy. The operational question of who owns the output in a contested or ambiguous case is frequently unanswered at the process level, even when it is answered on paper in a policy document.

That gap is where regulatory exposure lives.

Why This Is Harder Than It Looks from the Boardroom

The complexity of achieving genuine AI governance compliance in a multi-state insurance operation is not well understood outside of the operational layer.

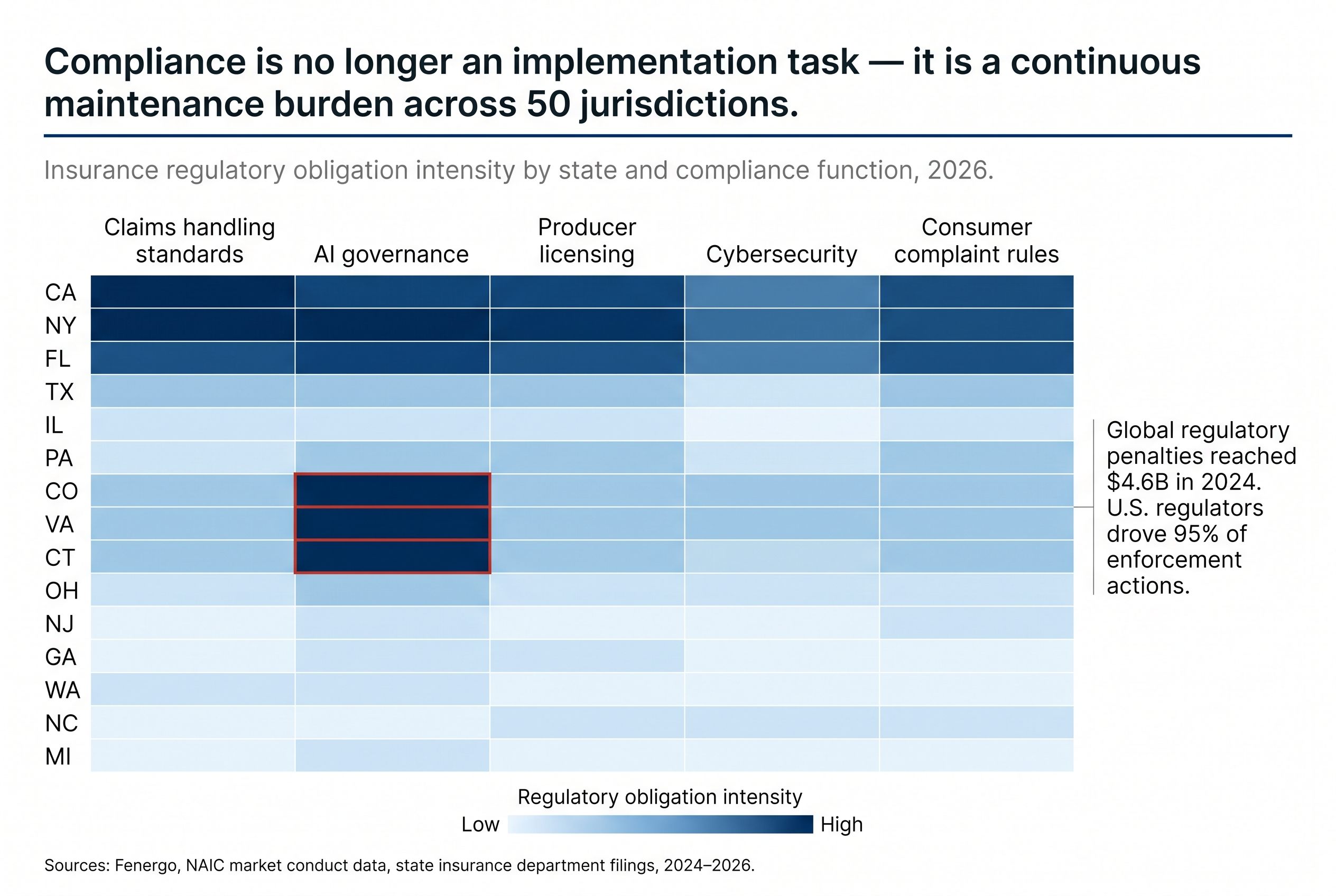

Consider what state-specific compliance actually requires in practice. A carrier operating across 20 states must maintain a compliance posture that accounts for different disclosure requirements, different standards for what constitutes an automated decision versus a supported decision, different definitions of which AI applications qualify as high-risk, and different audit and examination protocols. As new state laws take effect throughout 2026 and beyond, that matrix of requirements will expand.

Building static policies at the enterprise level does not solve this problem. What is required is an operational layer that can apply state-specific logic at the point of decision, flag the cases that require human review under a given state's standards, maintain the documentation trail that regulators will request, and adapt as requirements change.

This is, at its core, a workflow design and execution problem as much as it is a technology or legal problem. Legal teams can define the requirements. Technology teams can build the systems. Without an operational layer that executes the logic correctly at transaction volume, the compliance framework exists on paper but not in practice.

The distinction between paper compliance and operational compliance is precisely what regulators are increasingly equipped to detect. The NAIC's supervisory infrastructure now includes AI-specific examination tools. The question is not whether a carrier has a governance policy. The question is whether that policy is reflected in how decisions are actually made and documented at scale.

The Strategic Response

The carriers that will navigate this environment without material disruption share a common characteristic. They are treating AI governance as an operational discipline rather than a compliance checkbox.

In practical terms, this means several things.

First, it means establishing a defined human-in-the-loop architecture before deploying AI at decision-relevant volume. Not as a fallback for system failures, but as a designed component of how decisions flow. The human review layer is not inefficiency in the process. In a multi-state regulatory environment, it is the mechanism through which compliance is actually executed.

Second, it means building state-specific rule sets into operational workflows, not just into legal documentation. The adjudicator, the servicing associate, or the AI oversight function needs to know, at the point of processing a specific transaction, what that state's requirements are for that type of decision. Centralized policy documents do not achieve this. Workflow design achieves this.

Third, it means treating documentation as a real-time operational output rather than a retrospective task. Regulatory examinations in this environment will request documentation of AI-assisted decisions. The carriers with that documentation already structured will manage those examinations differently from those who must reconstruct it.

Finally, it means building operational capacity that can flex as requirements change. The regulatory environment for AI in insurance is not stabilizing. Colorado's implementation date moved once. New states are passing legislation. The NAIC is developing additional guidance. An operational model that treats current requirements as fixed will require repeated reactive remediation. An operational model designed for continuous adaptation will compound its advantage over time.

The Cost of Inaction Is Not Theoretical

Global regulatory penalties in the financial services sector reached $4.6 billion in 2024, with U.S. regulators accounting for 95 percent of enforcement actions. Insurance regulators have historically been among the most active in the country. The infrastructure to examine AI governance is now being built explicitly.

For insurance leaders evaluating the urgency of this issue, the relevant comparison is not what penalties carriers have received to date for AI governance failures. It is what enforcement infrastructure regulators are investing in right now, and what that implies for the enforcement environment 12 to 24 months from today.

The carriers that treat AI governance as an operational priority in 2026 will not merely be ahead of enforcement. They will have built an operational capability, a state-aware, documented, human-supervised decision architecture, that serves as a durable competitive asset as the market continues to evolve.

The carriers that treat it as a future consideration are accumulating exposure at the same pace they are deploying AI. In a regulatory environment this active, that is a risk the balance sheet will eventually reflect.

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.