Your Retention Problem Is Not at Renewal. It Was Created Six Touchpoints Earlier.

The way most insurance carriers manage retention is structurally misaligned with where retention is actually determined.

The industry has built sophisticated capabilities around the renewal event: pricing models, loyalty programs, outbound retention calls, competitive rate analysis. These are genuine investments in keeping policyholders, and they represent meaningful operational capacity. The problem is their timing. By the moment a policyholder receives a renewal notice and a carrier activates its retention infrastructure, the decision is frequently already made. Not consciously, not as a formal commitment, but as a disposition shaped by the cumulative quality of every service interaction that preceded the renewal.

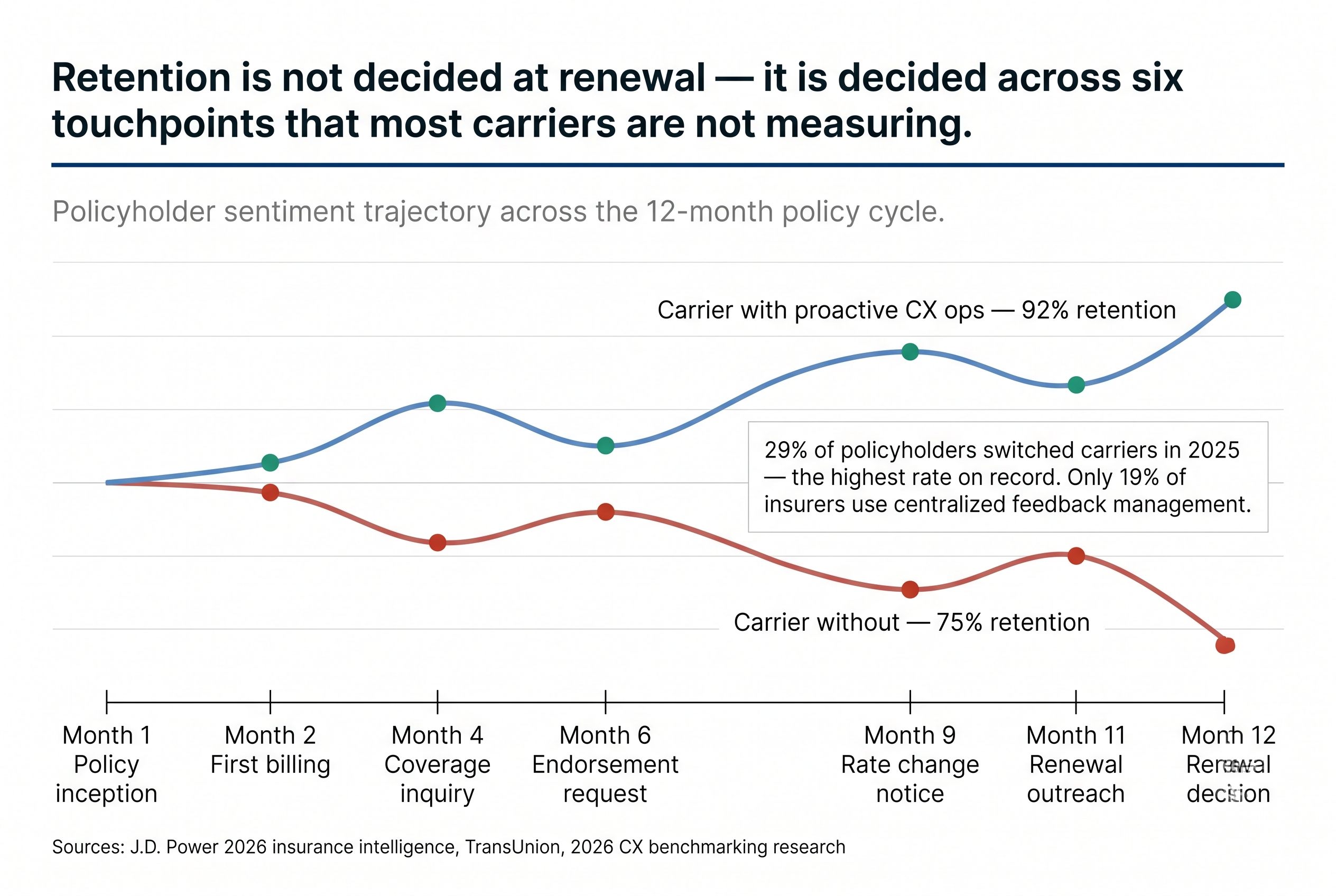

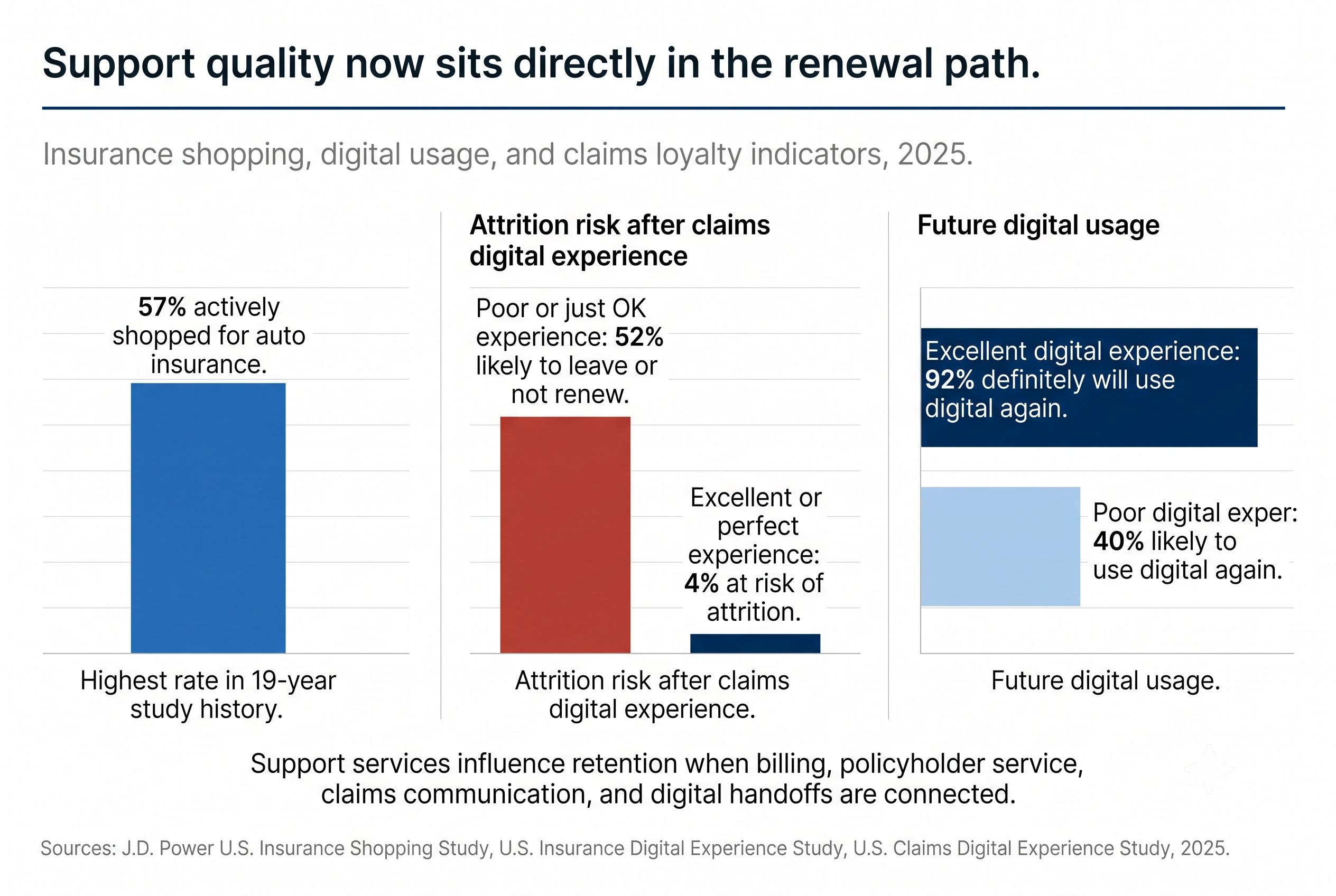

J.D. Power's 2026 insurance intelligence data showed that 29 percent of insurance customers switched carriers in 2025, a market-switching rate that has never been higher. Fifty-seven percent of auto insurance customers actively shopped for coverage, up from 49 percent in 2024. The carriers losing these customers are not, in most cases, losing them because a competitor offered a better product at renewal. They are losing them because the policyholder arrived at renewal already disengaged, and the price differential needed to retain a disengaged customer is different from the differential needed to retain one who had consistently positive service experiences over the prior twelve months.

The retention problem in insurance is operationally upstream from where most carriers are managing it. Understanding why requires a clear-eyed assessment of what the service experience between renewals actually produces.

The Hidden Cost Architecture of CX Fragmentation

The 2026 State of Customer Experience in Insurance research documented a finding that should be concerning to every carrier leadership team: only 19 percent of insurers use a centralized feedback management system. The majority of carriers are collecting customer experience data across channels, functions, and touchpoints without the operational infrastructure to synthesize it into a coherent view of the policyholder relationship.

That fragmentation has consequences that extend beyond satisfaction measurement. It produces a service experience in which a policyholder who called about a billing dispute last month, filed a minor claim two months before that, and asked a coverage question the month before that has interacted with three different operational functions, none of which had access to the context of the others. Each interaction was processed correctly within its functional silo. The cumulative experience was one of fragmentation, repetition, and the persistent sense that the carrier does not know who they are.

McKinsey analysis found that 60 percent of insurance customers switch channels before purchase, and one of the most consistently reported pain points across policyholder research is the requirement to repeat information when moving between channels or functions. That pain point sounds minor in isolation. Accumulated across a twelve-month policy period, it is the difference between a policyholder who arrives at renewal with a sense of relationship and one who arrives with a sense of transaction.

The financial consequence of that distinction is material. Forty percent of policyholders have considered canceling their insurance because they were unsure whether their coverage justified the cost, according to industry research. That perception of value is not primarily a pricing perception. It is an experience perception. The policyholder who has had three frictionless, well-handled service interactions over the course of a year arrives at a 10 percent premium increase with a different value calculation than the one who has spent cumulative hours repeating information, waiting for callbacks, and receiving inconsistent answers about their coverage.

Where Retention Is Actually Determined

The evidence on what drives retention decisions in insurance is consistent across multiple research streams, and it points to a different location than the renewal conversation.

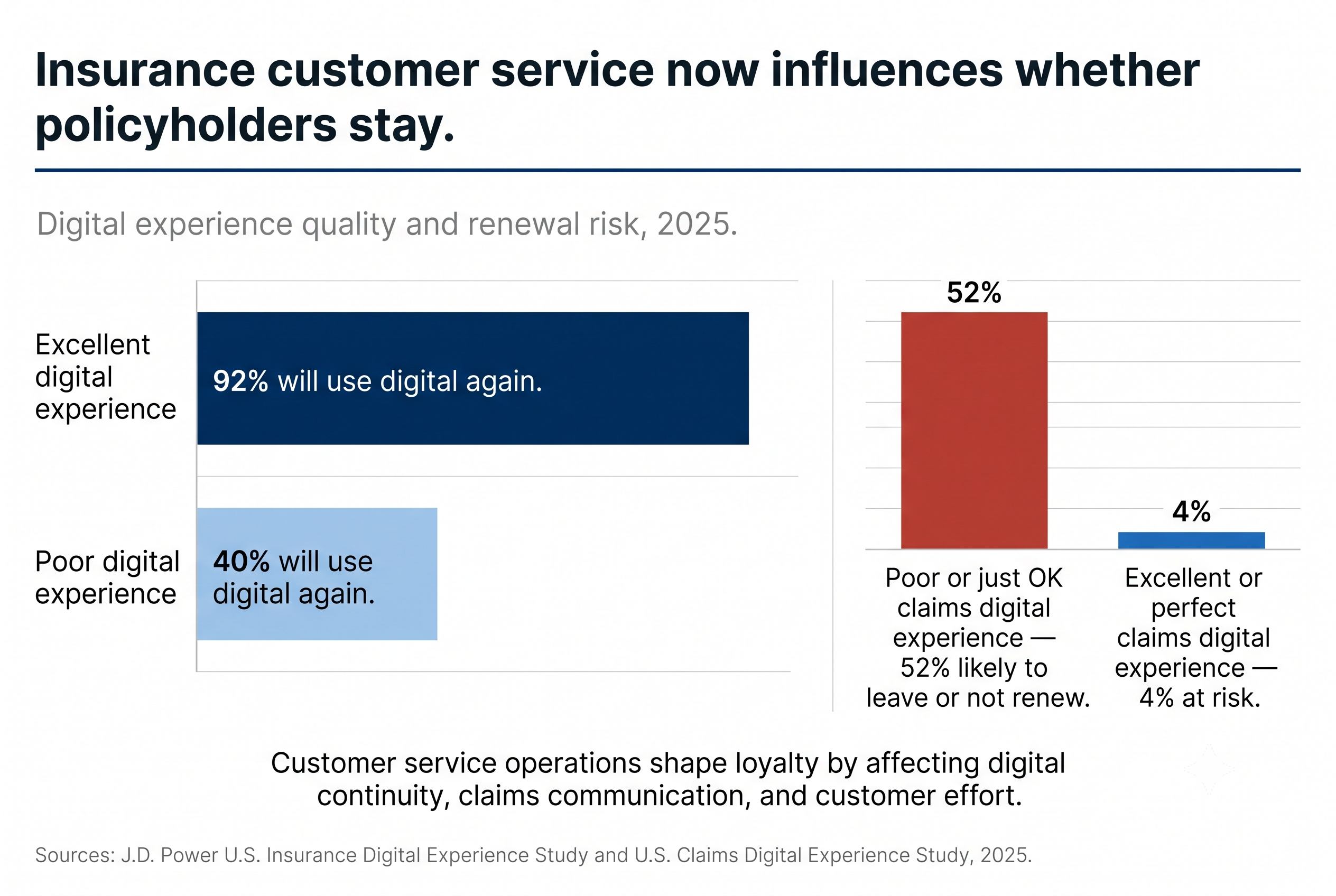

Claims handling is the highest-leverage retention event in the policyholder relationship. Research on P&C policyholder behavior is unambiguous on this point: the claims experience is the moment of truth that determines whether a policyholder renews or shops elsewhere. Fewer than half of customers in 2024 reported feeling that insurance was worth the price. The claims experience is the primary mechanism through which carriers either validate or destroy that perception. A policyholder who files a claim and receives fast, accurate, empathetic handling emerges from that experience with a disposition toward renewal that no competitor's rate advantage easily overcomes. A policyholder who files a claim and encounters delays, inconsistent communication, and the frustration of having to re-explain their situation multiple times arrives at renewal in a fundamentally different and far more price-sensitive state.

The interval between claims and renewal is the second highest-leverage window, and it is the one most consistently underinvested in operational terms. In our experience working with carriers managing high-switching environments, the carriers that retain the highest proportion of at-risk policyholders are not the carriers that execute the best outbound retention calls in the 60 days before renewal. They are the carriers that maintained consistent, proactive contact in the months between the last service interaction and the renewal notice. That contact does not need to be elaborate. A coverage check-in, a proactive communication about a policy change, an acknowledgment of a policyholder anniversary, all of these generate a different relationship dynamic than silence followed by a renewal notice and a rate increase.

Policy servicing quality, the handling of billing questions, endorsement requests, payment support, and routine coverage inquiries, is the third pillar of retention that most carriers undervalue precisely because these interactions do not feel strategic. They feel administrative. The policyholder who calls to add a vehicle to their policy and receives a fast, accurate, friendly service experience has had a positive deposit made in the relationship account that will affect their renewal calculus. The policyholder who navigates three transfers, waits on hold, and ultimately resolves a straightforward endorsement through effort they did not expect to expend has had a withdrawal made from the same account.

J.D. Power's intelligence framework identified the carriers most likely to succeed in 2026's retention environment as those that can unlock the most streamlined interactions and proactively communicate. That capability is entirely an operations output, not a product or pricing output.

The Operational Infrastructure That Retention Actually Requires

The gap between carriers achieving 92 percent retention in digital channels and those struggling to hold 75 percent is not primarily a technology gap or a pricing gap. It is an operational execution gap. Carriers with mature, integrated customer data implementations achieve 28 percent improvement in retention compared to those with fragmented customer data environments, according to 2026 benchmark research. That 28 percent differential is not delivered by technology alone. It is delivered by the operational infrastructure that uses that technology to produce consistent, contextually aware service at the moments that shape the policyholder relationship.

Building that operational infrastructure requires clarity about what it actually consists of.

The first component is interaction continuity. Every service interaction a policyholder has should be accessible to every function that subsequently handles that policyholder. This sounds obvious and is operationally difficult at scale in most carrier environments. The billing function should know about the recent claims experience. The renewal outreach team should know about the coverage inquiry that went unresolved six weeks ago. The claims handler should know that this policyholder recently escalated a billing dispute. Interaction continuity does not eliminate the need for good individual interactions. It prevents individually acceptable interactions from accumulating into a collectively frustrating experience.

The second component is proactive outreach architecture. The research on retention consistently identifies proactive communication as a primary driver of policyholder loyalty, specifically the communication that acknowledges the carrier knows who the policyholder is and is engaging with them before the policyholder needs to initiate contact. Building a proactive outreach capability that operates across the full policy period, not only in the renewal window, requires operational bandwidth that most carriers allocate to inbound volume management rather than to outbound relationship maintenance. The carriers that have built this capacity treat the 90-day pre-renewal proactive contact not as the start of the retention effort but as the closing of a relationship that has been actively maintained throughout the policy year.

The third component is first-contact resolution discipline applied consistently across all interaction types, not only claims. The billing inquiry resolved completely on first contact represents a different retention contribution than the billing inquiry that requires two callbacks. Applying first-contact resolution standards and measurement to the full range of policyholder interactions, not only to claims, produces a different pattern of experience accumulation across the policy year.

The fourth component is escalation recognition. Not every service interaction is a retention risk. But some are, and the operational function that handles them needs the capability to recognize which ones. A policyholder who calls about a rate increase after a significant premium jump is in a different retention risk posture than one calling to add a driver. A policyholder who has filed two claims in the prior year and is now asking questions about coverage adequacy is signaling something different than one making a routine payment inquiry. Building the recognition capability and the corresponding escalation path into service operations, so that interactions that carry retention risk are handled with the specific attention they warrant, requires operational design that most carriers have not implemented systematically.

The Measurement Problem That Perpetuates the Gap

The structural reason carriers continue to invest most of their retention effort at the renewal event is a measurement problem. Retention rates are measured at renewal, which creates the impression that the renewal event is where retention is determined. The causal chain runs in the opposite direction, but the measurement architecture makes it invisible.

The carriers that have closed the gap between where retention is measured and where retention is determined have built measurement frameworks that track the relationship dynamics across the full policy period, not only at renewal. They measure the quality and resolution rate of service interactions at 90 and 180 days post-policy inception, not only at renewal. They track policyholder sentiment signals, payment patterns, contact frequency, and channel behavior as leading indicators of renewal risk, not as outputs visible only after the renewal decision is made. They use those signals to direct proactive operational engagement toward the policyholders whose relationship trajectory suggests elevated churn risk months before the renewal notice generates the churn.

The industry's highest switching rate in recorded history is not primarily a product of rate increases. Rate increases create the occasion for the decision. The operational experience over the prior twelve months determines which policyholders are susceptible to that occasion and which are not.

The carrier whose operational model treats the twelve months between renewals as a period in which retention is actively built, rather than a waiting period before the retention effort begins, is building a competitive advantage that compounds with every renewal cycle. The gap between the carrier with a 92 percent retention rate and one at 75 percent represents, at scale, a fundamentally different business economics. That gap is not closed at the renewal table. It is closed in the service interaction quality of the preceding year.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.