Insurance Support Services Are Becoming a Retention Advantage

Introduction

Insurance support services now sit closer to the customer relationship than many traditional service models suggested. A billing question, coverage explanation, endorsement request, renewal update, document issue, or claim status inquiry can influence whether a policyholder feels confident staying with the carrier. J.D. Power’s 2025 U.S. Auto Insurance Study found that good rates and low cost are the top reasons customers choose an insurer, while good service and positive claims experience are the top drivers of renewal. That places support work directly inside the retention conversation, especially as carriers continue refining service models across digital, phone, email, chat, and broker-assisted channels.

Support Now Shapes the Renewal Conversation

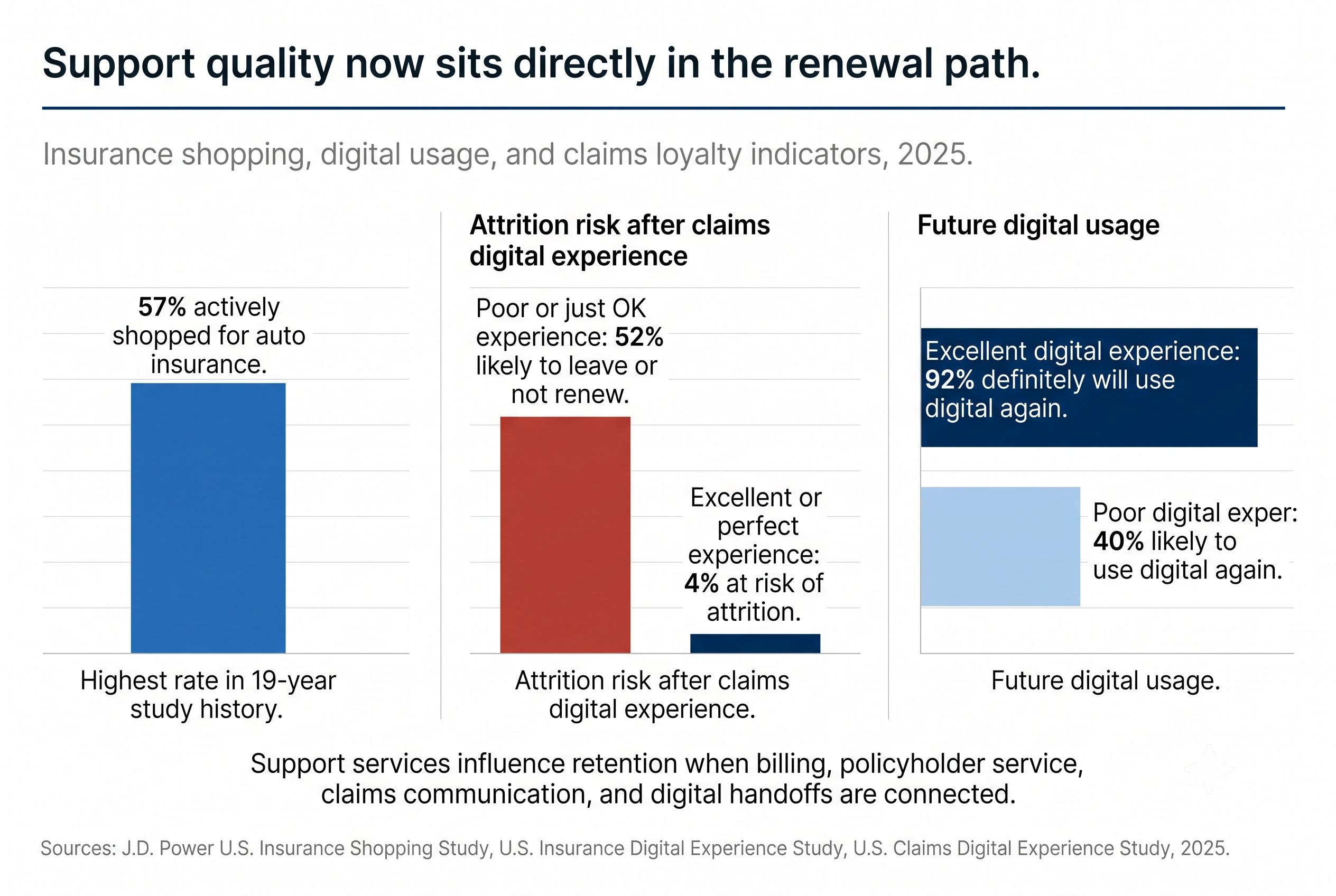

The 2025 market shows why support quality matters commercially. J.D. Power reported that 57% of auto insurance customers actively shopped for a new policy in the past year, the highest shopping rate recorded in the 19-year history of its U.S. Insurance Shopping Study. The same research found that one-third of active shoppers were seeking to bundle auto and homeowners coverage, a valuable segment because bundled customers have longer average tenure than non-bundled customers.

That does not make retention a pricing issue alone. Customers often compare price during shopping, but support experiences influence whether the relationship feels easy to maintain. A customer who receives clear answers on billing, coverage changes, renewal timing, documents, or claim status has fewer reasons to keep searching. For carriers, customer experience and support is becoming a practical retention function because the service team often handles the moments when customers decide whether the relationship still works for them.

Insurance Support Services Cover More Than Call Volume

The phrase insurance support services covers a broader operating layer than phone support. The Business Research Company’s 2026 Insurance Business Process Outsourcing Market Report lists customer care services as one of the main insurance BPO categories and breaks that category into call center operations, claims support, policyholder services, and helpdesk assistance. The same report includes policy administration, claims processing, customer support, data entry, and document management within the insurance BPO market definition.

That wider definition matters because most policyholder questions connect to another function. A service inquiry may require billing history, policy language, underwriting notes, claim status, renewal information, or documentation review. Support teams create more value when they can resolve the immediate request while protecting the accuracy of the workflow behind it. This is why ISSI’s insurance operations solutions connect support with claims, policy servicing, back-office operations, compliance, and AI workflow control.

Digital Service Still Depends on Human Context

Digital service has become a major part of how customers interact with insurers. J.D. Power’s 2025 U.S. Insurance Digital Experience Study found that 47% of auto insurance shoppers now purchase policies through digital channels, compared with 35% through agents and 17% through call centers. The study also found that when customers have an excellent digital experience, 92% say they definitely will use digital channels again, compared with 40% among customers with poor digital experiences.

Those numbers point to a practical operating reality: digital adoption increases the need for accurate support behind the channel. Customers use websites and apps for quotes, servicing, documents, payments, and updates, but they still need informed support when a question requires explanation or judgment. A strong support model gives associates the context to help customers move from digital self-service into assisted service without repeating information or restarting the request.

Claims Support Shows the Cost of Disconnected Information

Claims support is one of the clearest examples of how service quality affects loyalty. J.D. Power’s 2025 U.S. Claims Digital Experience Study found that insurers deliver adequate proactive digital updates only 22% of the time. The same study found that 22% of customers still rely on multiple channels to find answers to the same question, and 52% of auto and homeowners customers who rate their digital claims experience as poor or just OK are likely to leave or not renew, compared with 4% among those who rate the experience excellent or perfect.

This is an operations issue as much as a service issue. A customer asking for claim status may need information from intake, adjuster notes, vendor updates, payment status, document review, or coverage validation. When those details are connected, support teams can answer with confidence. ISSI has covered this pattern in Fragmentation Is Not a CX Problem. It Is a Cost Distortion Problem No One Owns, where fragmented information increases customer effort and creates extra work across the organization.

Policyholder Services Require Insurance Judgment

Policyholder service often looks simple from the outside. A customer asks for a document, changes an address, updates a vehicle, adjusts payment information, requests proof of coverage, or asks about renewal timing. Inside the operation, that request may affect billing, declarations, underwriting records, lienholder data, broker communication, regulatory notices, or claims eligibility. The quality of the answer depends on the associate’s ability to recognize which requests are routine and which require review.

Capgemini’s 2025 World Life Insurance Report found that only 5% of life insurers globally deliver quantifiably outstanding customer experience. Those carriers achieved 38% higher Net Promoter Scores, 11% lower expense ratios, and 6% higher growth over three years compared with mainstream insurers. The research specifically highlights onboarding, self-service, servicing, and claims as core areas where connected operations can produce measurable business results.

The Scorecard Should Measure Resolution Quality

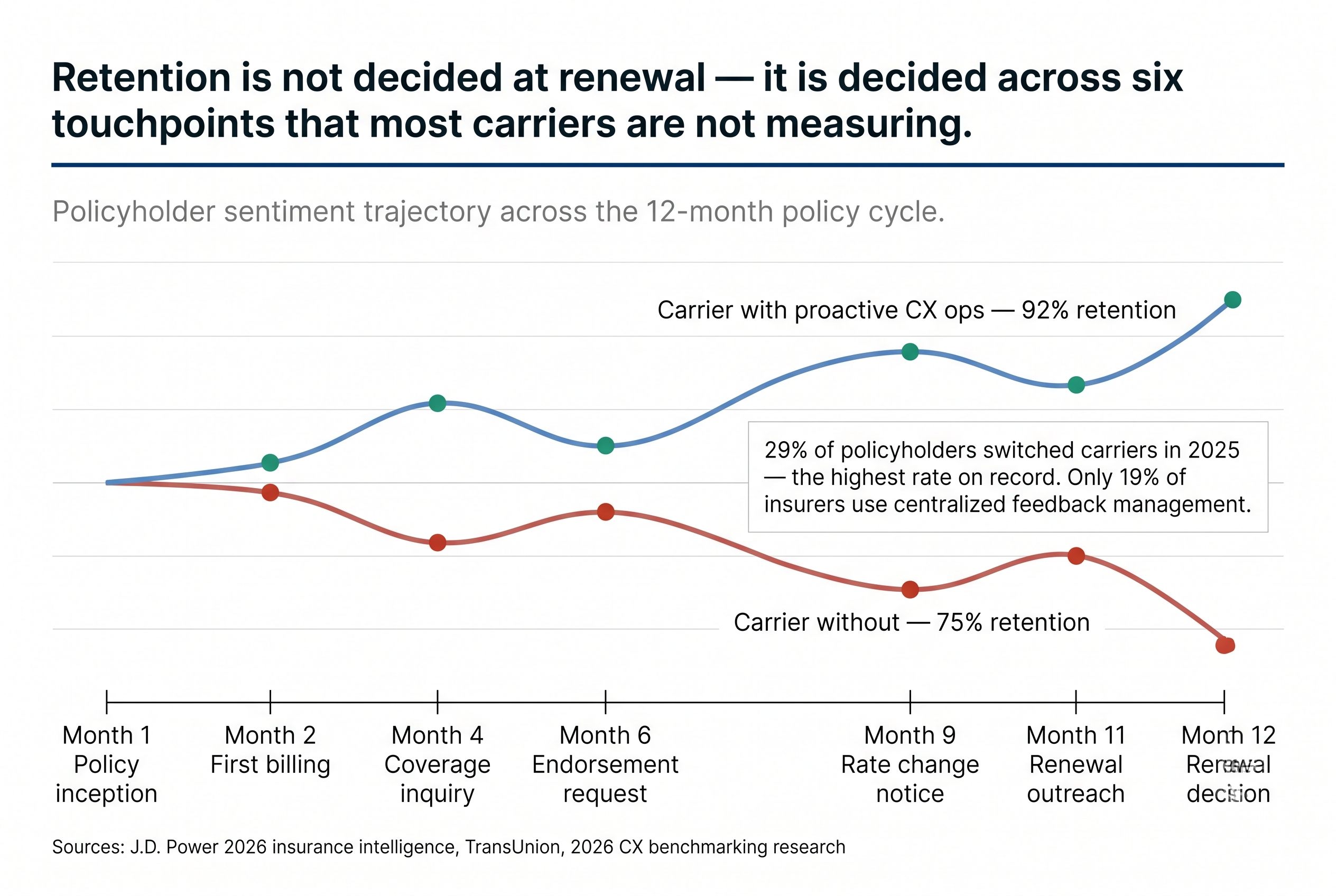

Support operations need activity metrics, but activity alone does not show whether customer requests are being resolved cleanly. Calls answered, average handling time, chats completed, and emails closed help leaders manage workload. Resolution quality requires a different set of measures: first-contact resolution, reopened cases, repeat contact rate, correction volume, escalation rate, customer effort, quality review findings, and downstream touches per request.

The expense context is clear. The NAIC’s 2025 mid-year property and casualty analysis reported $124 billion in underwriting expenses for the US P&C industry, a 25.2% expense ratio, and a 96.4 combined ratio for the first half of 2025. Support services influence that expense base because repeated contacts, corrections, unclear handoffs, and delayed answers create avoidable workload across service, claims, policy administration, billing, and compliance.

AI Raises the Value of Controlled Support Workflows

AI is becoming part of the support environment through call summaries, knowledge assistance, workflow routing, document review, chat support, and quality monitoring. The Business Research Company identifies AI-powered insurance BPO services as a major market trend and points to increasing adoption of automated claims and policy processing, AI-based workflow management, analytics-driven decision support, and secure outsourcing platforms as growth factors for the insurance BPO market.

AI-supported service still depends on clean workflow design. Support teams need accurate knowledge sources, clear escalation paths, documented decision rules, audit trails, and human review for sensitive issues. ISSI discussed this control layer in AI in Claims Is Working Exactly as Designed. That’s the Problem, and the same logic applies to policyholder service, billing inquiries, claims support, and compliance-related requests. Carriers evaluating AI operations and workflow control should examine how support interactions are reviewed, corrected, documented, and fed back into training.

Closing Perspective

Insurance support services are becoming a retention advantage because they sit at the point where customer experience, operational accuracy, and cost control meet. The support interaction is often where a customer learns whether the carrier has the information, coordination, and responsiveness needed to keep the relationship easy to manage.

The opportunity for carriers is practical. Support teams can reduce customer effort, protect renewal intent, improve claims communication, and surface the operational patterns that create repeat contacts. The strongest support models connect people, systems, quality controls, and insurance knowledge around the full policyholder journey. For carriers reviewing where support consistency, claims communication, policyholder service, or workflow control can improve, ISSI’s insurance operations solutions provide a way to evaluate support as part of the broader operating model.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.