Insurance Operations Are Becoming the Control Layer for AI

Introduction

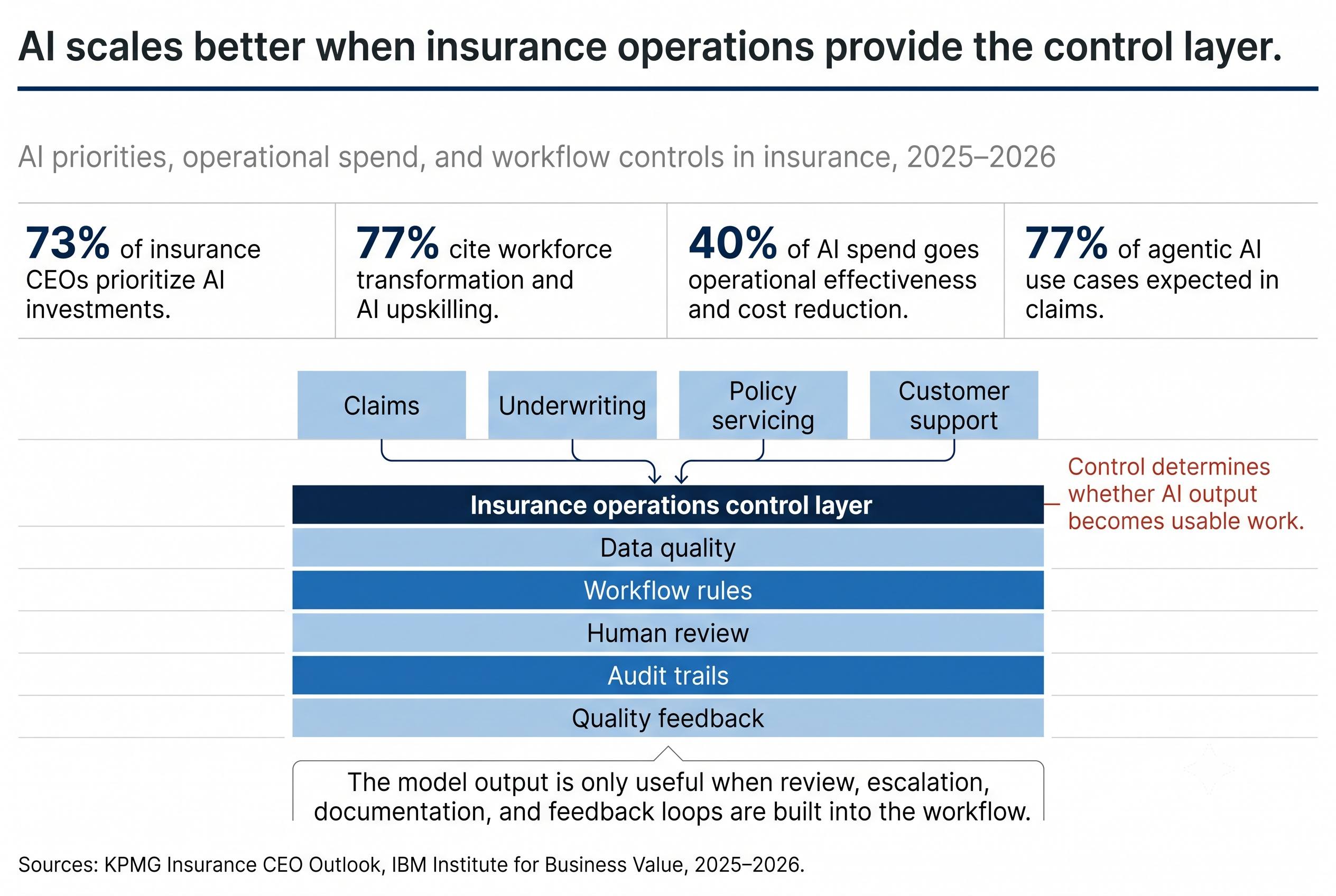

AI investment is moving deeper into insurance operations. Underwriting, claims, customer experience, fraud review, compliance documentation, policy servicing, and back-office workflows are all becoming part of the AI conversation. KPMG’s 2025 Insurance CEO Outlook found that 73% of insurance CEOs are prioritizing AI investments to streamline underwriting, claims, and customer experience, while 77% identify workforce transformation and AI upskilling as a top constraint and opportunity. That places insurance operations at the center of AI execution, because every model output still needs workflow rules, human review, documentation, quality feedback, and regulatory control.

AI Is Moving Into Daily Insurance Work

Insurance AI is expanding from recommendations and summaries into workflow execution. IBM’s 2025 Insurance in the AI Era report found that insurers allocate 40% of AI spend to operational effectiveness and cost reduction, and 77% expect to use agentic AI in claims over the next year. The same report describes agentic AI use cases such as claims orchestration, damage inspection, repair estimates, payment initiation, policy changes, complex customer queries, and edge-case support.

That shift changes the role of operations. A claim summary, customer response, policy change, or fraud flag becomes useful when it enters a process with defined ownership. Someone has to decide what the model can handle, what requires review, what needs documentation, and what should be escalated. AI can increase speed, but the operating model determines whether that speed improves claims, servicing, support, and compliance outcomes.

Workflow Design Determines the Quality of AI Output

The quality of an AI-supported workflow depends on the quality of the process around it. Deloitte’s 2025 insurance technology trends report notes that small language models may be better suited for insurance-specific tasks because they can be tuned to specific operational processes, policy details, claim statuses, and use cases across the insurance value chain. Deloitte also highlights human-in-the-loop models as a way to pair GenAI with claims processing, product personalization, and cyber risk work.

For carriers, this makes workflow design a practical AI requirement. Claims triage needs clear severity rules. Policy servicing needs accurate data fields and exception paths. Compliance workflows need documentation standards. Customer support needs approved knowledge sources and escalation rules. An AI operations and workflow control model gives the technology a structured operating environment, which helps associates review outputs, correct errors, and feed quality findings back into training.

Claims Show Why the Control Layer Matters

Claims is one of the clearest examples of why AI needs connected operations. A digital claim journey may involve FNOL, coverage verification, triage, adjuster assignment, vendor coordination, status updates, payment review, and customer communication. If those steps are connected, AI can help route work, summarize information, identify missing documentation, and support faster decisions. If the process is fragmented, the customer often has to move across channels to get the answer they need.

J.D. Power’s 2025 U.S. Claims Digital Experience Study found that insurers deliver adequate proactive digital updates 22% of the time, while 22% of customers still rely on multiple channels to find answers to the same question. The same study found that 52% of auto and homeowners customers who rate their digital claims experience as poor or just OK are likely to leave or not renew, compared with 4% among customers who rate the experience excellent or perfect.

This is the operating pattern ISSI discussed in AI in Claims Is Working Exactly as Designed. That’s the Problem. AI performs inside the system it is given. Claims operations create the structure that determines whether digital tools produce cleaner communication, faster routing, stronger documentation, and better customer visibility.

Human Review Is Becoming a Designed Function

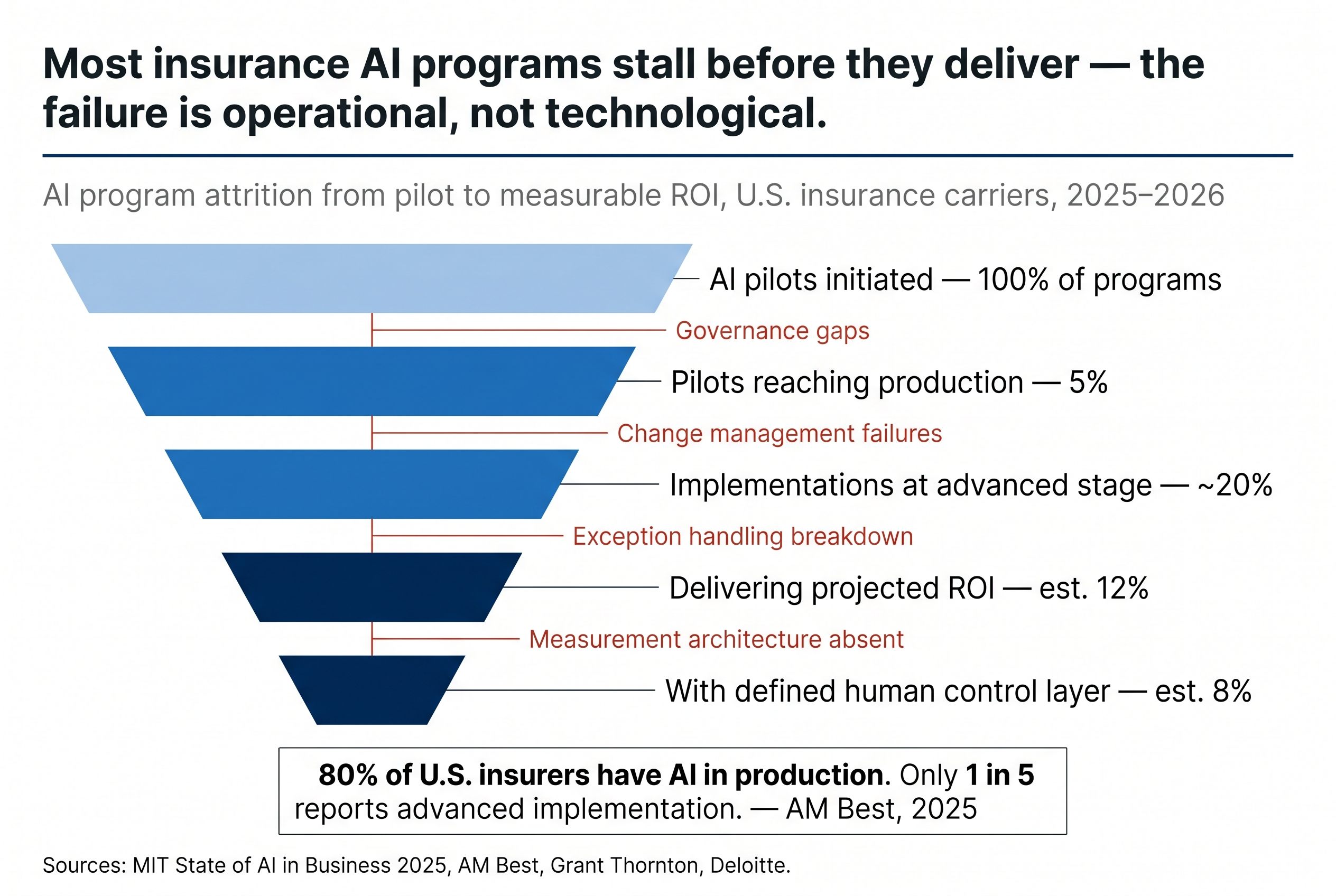

Human review is becoming part of the AI operating model. KPMG’s 2025 Insurance CEO Outlook found that 77% of insurance CEOs identify workforce transformation and AI upskilling as a top constraint and opportunity, and IBM found that more than 4 in 10 insurers see a need for additional internal skills and expertise to implement AI effectively. IBM also reported that 71% of insurance executives are using strategic partnerships with technology firms, vendors, and startups to accelerate AI-driven innovation.

This creates a practical role for experienced insurance operations teams. Reviewers need to understand when an exception is routine, when it signals customer sensitivity, when it affects compliance documentation, and when it may create downstream claims or policy issues. In underwriting support, servicing, claims, and customer care, human judgment helps decide whether the AI output is ready to move forward or needs more context.

Governance Is Moving Into the Operating Layer

AI governance is becoming part of daily insurance work. The NAIC’s June 4, 2026 implementation map for its Use of Artificial Intelligence Systems by Insurers model bulletin lists adopted jurisdictions including Alaska, Arkansas, Connecticut, Delaware, the District of Columbia, Hawaii, Illinois, Iowa, Kentucky, Maryland, Massachusetts, Michigan, Nebraska, Nevada, New Hampshire, New Jersey, North Carolina, Oklahoma, Pennsylvania, Rhode Island, Vermont, Virginia, Washington, West Virginia, and Wisconsin. The same NAIC map identifies separate insurance-specific regulation or guidance in California, Colorado, New York, and Texas.

For carriers, governance becomes operational when it is applied at transaction volume. A policy can define the standard, but the workflow has to execute it through audit trails, exception routing, reviewer notes, customer notices, model monitoring, quality review, and documentation retention. ISSI’s article on AI governance compliance addressed this same point: the control layer has to exist inside the work, where decisions are made and recorded.

Insurance BPO Services Are Expanding With AI

AI is also changing what carriers expect from insurance BPO services. The insurance business process outsourcing market is projected to grow from $8.4 billion in 2025 to $9.11 billion in 2026, and The Business Research Company identifies AI-powered innovation, automated claims and policy processing, AI-based workflow management, data security, and compliance as major trends in the category. The same report defines insurance BPO services across claims processing, policy administration, customer support, underwriting support, data entry, document management, customer care, helpdesk assistance, legal and compliance services, and analytics.

That makes the partner model more operationally connected. A carrier may need support reviewing AI-generated claim summaries, validating document extraction, monitoring customer service quality, managing exception queues, or preparing compliance documentation. Experienced insurance operations solutions can help carriers combine delivery capacity with process knowledge, quality control, and human review across the workflows where AI is being introduced.

What Carriers Should Evaluate Before Scaling AI Workflows

Before scaling AI across an insurance workflow, carriers need to define the operating rules around the technology. The process should clarify which inputs are required, which decisions the AI supports, which outputs require review, who owns corrections, how exceptions are routed, and how quality findings are fed back into the workflow. IBM’s 2025 action guide recommends integrating AI into key insurance processes, continuously monitoring AI-driven processes, refining them over time, and establishing governance frameworks covering ethics, regulatory compliance, and model performance standards.

The best evaluation starts with a specific workflow. In claims, that may mean FNOL, triage, document review, or status communication. In policy servicing, it may mean endorsements, renewal updates, proof-of-coverage requests, or billing changes. In customer support, it may mean knowledge assistance, call summaries, chat support, or quality monitoring. A complete insurance operations solution should make the AI-enabled workflow visible enough to manage, measure, and improve.

Closing Perspective

AI is raising the value of insurance operations because the output of a model becomes meaningful only when it is connected to a well-managed process. The work around the technology now matters as much as the technology itself: data quality, workflow design, escalation rules, human review, audit trails, and quality feedback determine how AI performs inside claims, policy servicing, compliance, customer support, and back-office operations.

For carriers, the opportunity is practical. Build the operating layer that allows AI to support faster work, clearer decisions, stronger documentation, and better customer communication. For organizations reviewing how AI fits into their insurance operations, ISSI’s AI operations and workflow control capabilities provide a way to evaluate where people, process, and technology should work together across the insurance lifecycle.

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.