Insurance BPO Services Have Changed. Here’s What Carriers Expect Today

Introduction

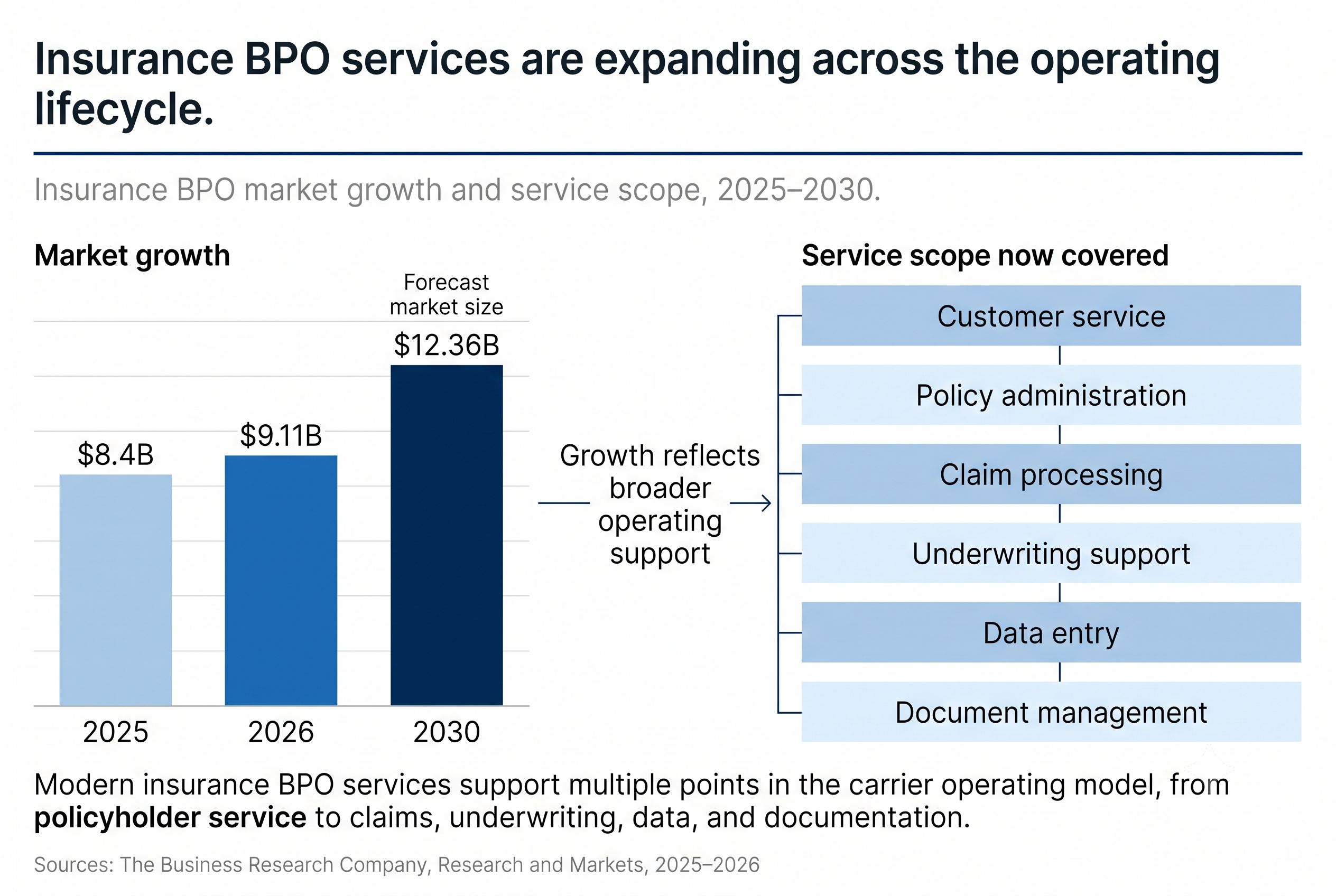

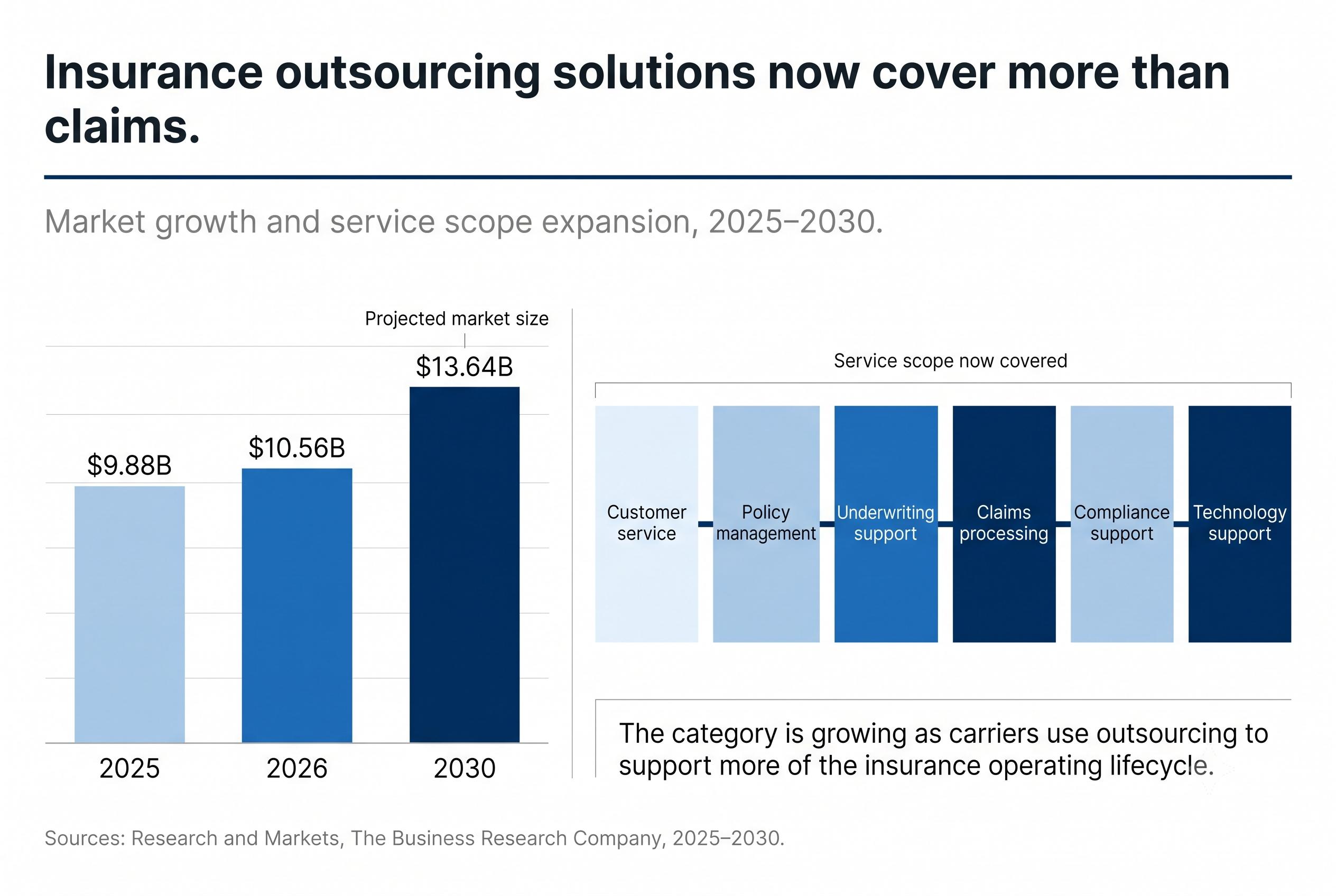

Insurance BPO services now sit closer to the core operating model of a carrier. The work includes customer care, policy administration, claims support, underwriting support, billing, compliance tasks, data management, document processing, and AI workflow review. The global insurance business process outsourcing market is projected to grow from $8.4 billion in 2025 to $9.11 billion in 2026, with forecast growth tied to process complexity, demand for scalable service delivery, automation, analytics, secure outsourcing platforms, and specialized insurance talent. That growth reflects how carriers are evaluating BPO today: capacity matters, but the larger value comes from process quality, insurance knowledge, and operating control.

Operational Capacity Still Matters

Capacity remains one of the practical reasons carriers use insurance BPO services. Claims volume can rise after catastrophe activity, customer support teams can see heavier demand during renewal periods, and policy servicing teams often need flexible support when books of business grow or products change. The NAIC’s 2025 mid-year property and casualty analysis reported $124 billion in underwriting expenses, a 25.2% expense ratio, and a 96.4 combined ratio for the US P&C industry. Those numbers show why operational discipline stays high on the executive agenda even when underwriting performance improves.

The value of capacity increases when it is tied to clear work design. A carrier may need more people answering customer questions, but it also needs consistent scripts, accurate policy data, escalation paths, quality review, and visibility into where repeat contacts begin. That is why modern insurance support services are increasingly evaluated through service consistency and workflow control, not staffing levels alone.

The Service Mix Has Expanded Across the Insurance Lifecycle

The insurance BPO market now covers a wider mix of functions than many executives associated with outsourcing a decade ago. Research and Markets’ 2026 report segments the market across asset management, finance and accounting services, customer care services, marketing, policy administration, and other services. It also identifies subsegments such as call center operations, claims support, policyholder services, helpdesk assistance, policy issuance and renewal, underwriting support, risk assessment, and claims management.

That broader service mix fits the way insurance work actually moves. A customer service question can become a billing correction. A policy change can affect underwriting records and future claims eligibility. A claims intake file can influence fraud review, severity assignment, documentation quality, and customer communication. ISSI’s insurance operations solutions are built around that connected operating reality, with support across claims, policy servicing, underwriting, CX, compliance, fraud, back-office work, and AI workflow control.

Quality Controls Are Becoming a Core Part of the Business Case

Activity metrics show workload. Quality metrics show whether the work is improving the operation. A team can answer more calls, process more transactions, or close more service tickets while still creating downstream rework for billing, underwriting, claims, or compliance. The stronger insurance BPO scorecard includes first-pass accuracy, reopened cases, correction volume, exception aging, escalation rate, customer effort, documentation quality, and downstream touches per transaction.

Capgemini’s 2025 World Life Insurance Report found that only 5% of life insurers deliver outstanding customer experience at a quantifiable level. Those insurers achieved 38% higher Net Promoter Scores, 11% lower expense ratios, and 6% higher growth than the industry over three years. The connection is operational: better onboarding, self-service, servicing, and claims capabilities can influence loyalty, expense, and growth at the same time.

Insurance Expertise Shows Up in Everyday Exceptions

Routine insurance work often carries judgment that a process map cannot fully capture. A policyholder request may involve state-specific notices, producer communication, premium changes, underwriting review, lienholder updates, renewal data, and documentation standards. A claims support task may require recognizing severity indicators, missing loss details, fraud signals, coverage questions, or customer sensitivity. The work becomes more reliable when associates understand both the transaction and the insurance context around it.

This is where insurance-specific BPO services create a practical advantage. The delivery team needs to know which items can be processed immediately, which require escalation, which need additional documentation, and which may affect another part of the policy or claim lifecycle. That knowledge protects the customer experience and reduces the correction work that often sits outside the original task queue.

Digital Experience Depends on the Operation Behind It

Digital channels improve access, but the customer experience still depends on the quality of the operating process behind the screen. J.D. Power’s 2025 U.S. Claims Digital Experience Study found that insurers deliver adequate proactive digital updates only 22% of the time, and 22% of customers still rely on multiple channels to find answers to the same question. The same study found that 52% of auto and homeowners customers who rate their digital claims experience as “poor” or “just OK” are likely to leave or not renew, compared with 4% among customers who rate the experience “excellent” or “perfect.”

Those findings matter for insurance operations because repeated channel switching is usually an operating signal. It can point to incomplete status data, unclear ownership, inconsistent communication, or missing workflow updates. ISSI has discussed this pattern in Fragmentation Is Not a CX Problem. It Is a Cost Distortion Problem No One Owns, where fragmented information increases cost and weakens decision quality across claims and policyholder interactions.

AI Adds a New Control Requirement

AI is becoming part of the operating environment carriers expect partners to support. KPMG’s 2025 Insurance CEO Outlook found that 73% of insurance CEOs are prioritizing AI investments to streamline underwriting, claims, and customer experience. The same report found that 77% identify workforce transformation and AI upskilling as a top constraint and opportunity for growth, while 83% are focused on strengthening risk management and cyber resilience.

AI-supported workflows need clear controls around data quality, exception handling, human review, audit trails, escalation, and quality feedback. In claims, underwriting support, servicing, and compliance, the model output is only one part of the operating process. The larger question is how the organization reviews exceptions, documents decisions, and learns from errors. ISSI covered this issue in AI in Claims Is Working Exactly as Designed. That’s the Problem, and the same principle applies across AI operations and workflow control.

What Carriers Expect From Insurance BPO Services Today

Carriers evaluating insurance process outsourcing services are looking for more than task completion. They want partners that can help maintain service quality across variable volume, train associates on insurance-specific workflows, document operating rules, manage exceptions, support compliance requirements, and create visibility into where rework begins. They also want delivery models that can adjust as products, customer expectations, regulatory requirements, and technology environments change.

The practical evaluation questions have become more specific. How does the partner capture institutional knowledge during transition? How are quality findings fed back into training? Which workflows require licensed or experienced insurance judgment? How are customer contacts, policy changes, claims details, and compliance documentation connected across teams? A strong partner can answer these questions with operating evidence, not broad promises.

Closing Perspective

Insurance BPO services have become more specialized because insurance operations have become more connected. Claims, policy servicing, customer support, underwriting support, compliance, fraud review, and AI workflow control all influence one another. A decision made in one queue can affect cost, quality, customer effort, and regulatory documentation somewhere else in the lifecycle.

That is the opportunity for carriers. Insurance BPO can add capacity, improve consistency, support technology adoption, and strengthen the operating layer that customers experience every day. The strongest results come when the partner understands the insurance workflow, measures quality across the full process, and helps the carrier see where work moves between functions. For organizations reviewing where support, scale, or workflow control can improve, ISSI’s insurance operations solutions provide a practical way to evaluate BPO as part of the broader operating model.

Related Blogs

Rethinking your

operations

doesn’t have to

happen alone.

If these challenges sound familiar,

let’s explore where your operations can improve.